- USD steadies after heavy declines but faces further tests

- As payrolls & other data to determine Fed’s taper timeline

- Disappointment could see USD ‘long’ positions squeezed

Image © Adobe Images

- GBP/USD reference rates at publication:

- Spot: 1.3756

- Bank transfers (indicative guide): 1.3378-1.3475

- Money transfer specialist rates (indicative): 1.3636-1.3664

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The U.S. Dollar attempted to find its feet in the mid-week session but would risk fresh loss ahead of the weekend should Friday’s job report or other pending economic figures give the Federal Reserve cause to delay an anticipated September tapering of its quantitative easing programme.

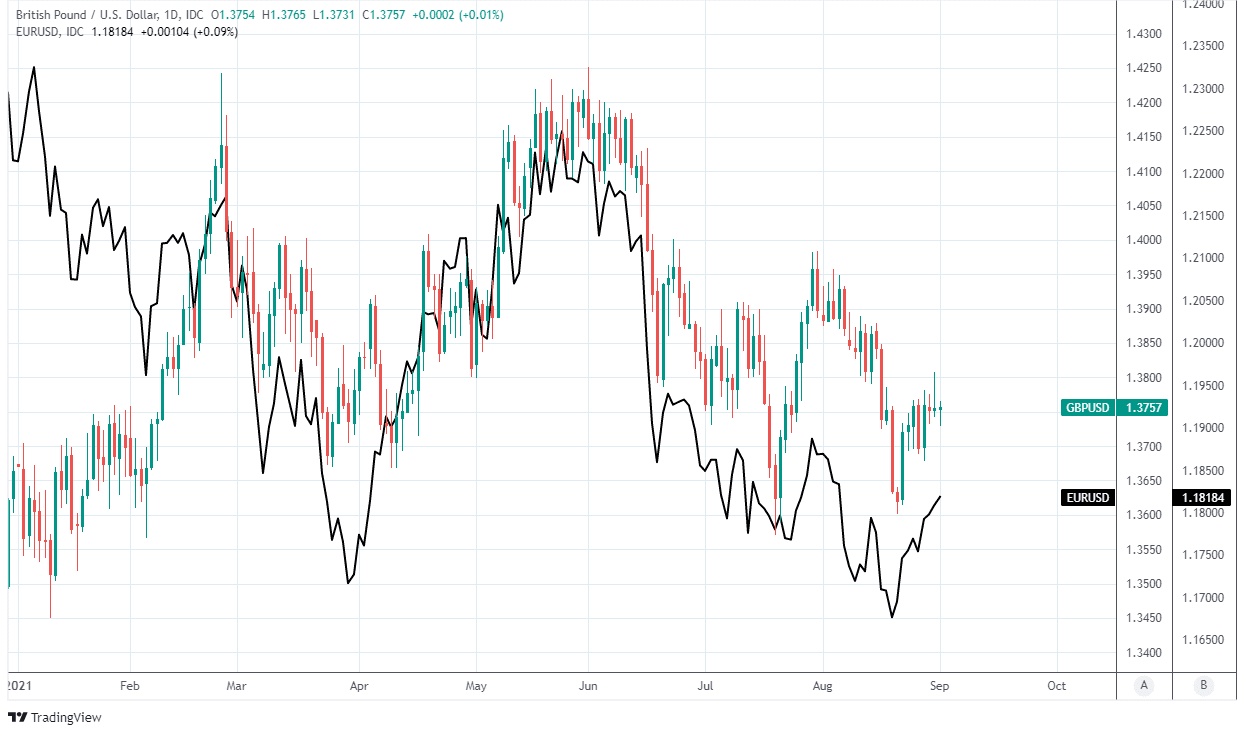

Some Dollar exchange rates found at least a short-term footing on Wednesday as selling appeared to abate following more than a week or almost uninterrupted declines for the U.S. currency, with the Pound-Dollar rate stalling around the week’s opening level just above 1.3750.

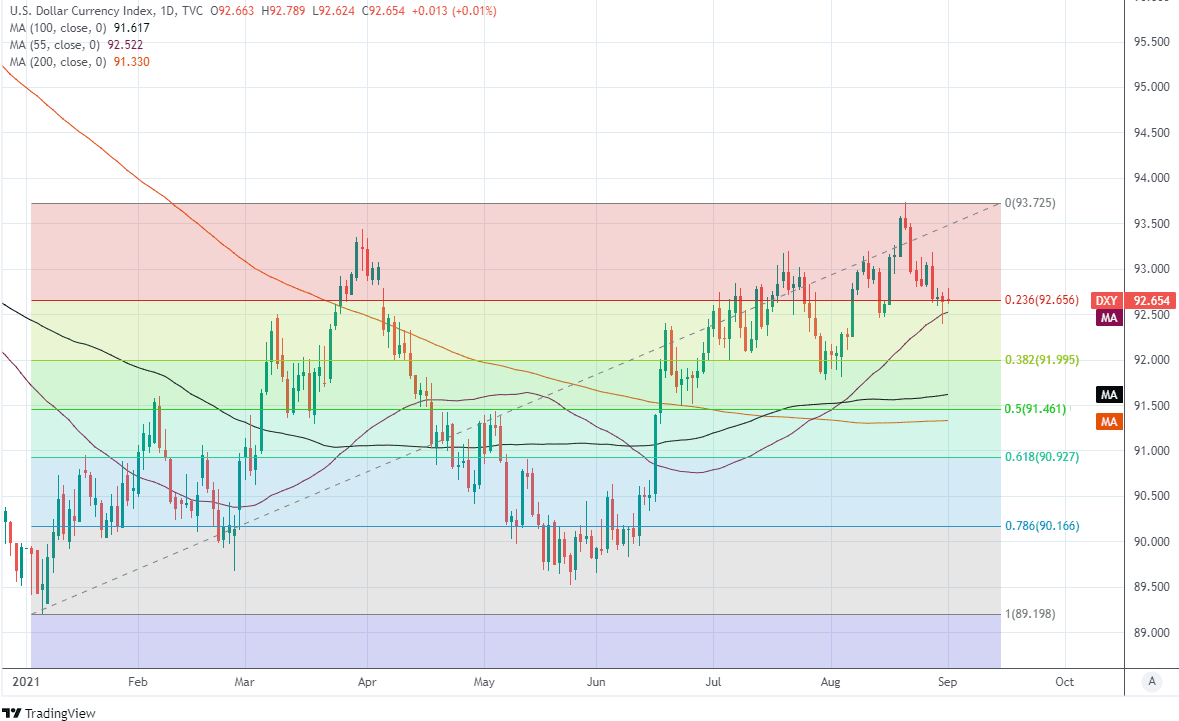

However, the Euro advanced against the greenback alongside the Australian and Canadian Dollars, leading the ICE U.S. Dollar Index to a fractional loss for the session that was in the process eroding an important level of technical support around 92.65 for the currency benchmark.

The Dollar has reached something of an inflection point from which it could either renew the losses seen over the recent fortnight or attempt a recovery, and this week’s non-farm payrolls report for August and Institute for Supply Management surveys will be decisive for which way the currency cuts in the wake of last Friday’s address from Federal Reserve Chairman Jerome Powell at the Jackson Hole Symposium.

“The USD is still nursing its wounds in the wake of the Jackson Hole central bank symposium,” says Valentin Marinov, head of FX strategy at Credit Agricole CIB. “Potential positive surprises from the releases, especially the labour market data, could be seen as bringing a QE taper closer and thus boosting the USD outlook. At the same time, any deterioration of global risk sentiment on the back of returning concerns about the growth-negative impact of the delta variant may now be less positive for the USD if they are seen as delaying the Fed’s policy normalisation.”

Above: U.S. Dollar Index shown at daily intervals with Fibonacci retracements of September 2020 fall indicating possible areas of resistance, with major moving-averages marking possible areas of support.

Chairman Powell confirmed last Friday the U.S. economy has been making light work of the “substantial further progress” toward full employment sought by the bank as a prerequisite for it to begin winding down its quantitative easing programme, but cautioned that “we will be carefully assessing incoming data and the evolving risks,” before making any decision on the scheme.

This has been flagged by analysts as something that could potentially delay the decision on tapering but it may also have mattered for the Dollar that Powell warned the economy will have to pass “a different and substantially more stringent test” before the Fed lifts its interest rates, one involving reemployment of the remaining six million workers idled by the coronavirus, which effectively rules out a rate rise any time soon.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

“A tapering announcement still seems likely this year, but we think hopes for September are overly optimistic. If confirmed, our expectation for a very disappointing US employment report should dash any remaining hopes of an early move. Against this backdrop, the USD is weaker against the spectrum of G10 and major EM currencies,” says Ned Rumpeltin, European head of FX strategy at TD Securities.

The Fed had already suggested in July that it would likely require more than one further policy meeting to make the call on shuttering the bond buying programme and to decide on the details of the process, meaning it already indicated that an announcement on tapering might be unlikely before November, although segments of the market had nonetheless assumed the bank would take the plunge in September.

Above: Pound-Dollar rate shown at daily intervals alongside EUR/USD.

The above assumption means the Dollar could be vulnerable to any poorer-than-expected outcome from this Friday’s non-farm payrolls report and potentially also to any other adverse economic data to emerge in the coming weeks. Consensus favours a 750k increase in the number of jobs created or recovered from the coronavirus in August, which would follow back-to-back blockbusters of 943k and 850k in July and June respectively.

“Clear guidance was provided that the Fed is on course for tapering the size of its asset purchases programme by the end of this year. However, the news was given a dovish tilt. Powell was cautious about the improvement in the labour market particularly for the black and Hispanic populations. He was also keen to separate policy on tapering from that on the Fed funds rate,” says Jane Foley, head of FX strategy at Rabobank. “The result was that there was no fresh fodder for the long USD positions that had been built up ahead of the meeting and a pull-back swiftly ensued.”

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

August’s non-farm payrolls report is out at 13:30 on Friday and forms the highlight of the week but before then the Institute for Supply Management (ISM) Manufacturing PMI is out at 15:00 on Wednesday and is followed at the same time on Friday by the ISM Services PMI, with both potentially providing an important signal about the pace of the U.S. recovery in mid-way through the third quarter.

“The bottom line, in my opinion, is that it might be a tough week for the US dollar due to the upcoming data releases. After all, the data is unlikely to be so good that it suggests the Fed will decide to taper sooner rather than later. On the contrary, if the market is disappointed, the USD could see an even sharper decline,” says Antje Praefcke, an analyst at Commerzbank.

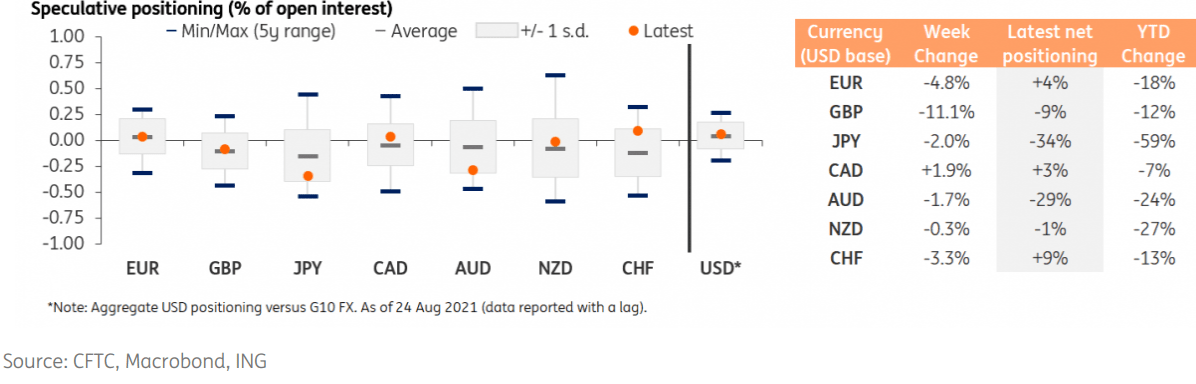

Above: ING graph shows changes in futures market’s speculative exposure to G10 currencies.

July’s ISM surveys had hinted of a fresh acceleration in the U.S. economy early this quarter, underwritten by the services sector and even as the manufacturing sector was being further stifled by temporary supply chain disruptions, although consensus among economists is for both survey indices to decline for August and the danger for the Dollar is that this simply encourages the market to further reconsider earlier wagers on the greenback.

“All currencies except for Canada's dollar saw a contraction in net positioning in the week ending 24 August. EUR/USD saw the largest drop in net positioning in two years, with the gauge dropping to 4% of open interest,” says Francesco Pesole, a strategist at ING. “An even larger drop in positioning (worth 11% of open interest) was recorded in sterling, although wide weekly fluctuations in positioning are more common in GBP than EUR.”

The Dollar could be especially vulnerable in the context of recent changes in investors holdings of it and other major currencies after Chicago Futures Trading Commission data showed investors filling their boots with further exposure to the currency for the week to Tuesday 24 August, presumably due to the popular conception that the Fed was becoming more likely to adjust its monetary policy settings sooner rather than later.

While some of that rebuilt exposure to the greenback may already have been jettisoned following Chairman Powell’s Jackson Hole address, those are exactly the kinds of wagers that could be squeezed in the event of disappointing economic data this week’s U.S. data, with potentially positive implications for currencies like Sterling and the Euro.