- GBP/USD looks for support at 1.38, 1.3675

- USD puts up resistance at 1.3960 & 1.4018

- Fed chair, speakers eyed before BoE decision

Image © Adobe Images

- GBP/USD reference rates at publication:

- Spot: 1.3807

- Bank transfers (indicative guide): 1.3424-1.3520

- Money transfer specialist rates (indicative): 1.3683-1.3710

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Pound-to-Dollar exchange rate enters the new week licking wounds near to early May lows around which it could stabilise ahead of an important address from Federal Reserve (Fed) Chairman Jerome Powell on Tuesday, and June’s monetary policy decision from the Bank of England (BoE) on Thursday.

Pound Sterling ended last week in the red against many currencies but wracked up its most significant loss by far against the Dollar, with GBP/USD falling more than one percent on Friday alone in an intraday decline that took its total loss for the week to in excess of -2%.

This left the Pound-Dollar rate clutching for support around six-week lows at 1.38 by the weekend although, and despite that, Sterling was still one of the better performing major currencies of the period.

That is in turn testament of the extent to which the U.S. Dollar came surging back after after June’s policy decision and quarterly forecasts emerged from the Federal Reserve (Fed), which included a dot-plot of projections for the Fed Funds interest rate range showing that a majority of eighteen Federal Open Market Committee (FOMC) members now see as many as two interest rate rises coming before the end of 2023; with the first potentially some time next year.

“With the Fed dots having done so much damage to positioning, the focus for the week ahead will be on a host of Fed speakers - and whether they're as hawkish as the dots suggest,” says Chris Turner, global head of markets and regional head of research at ING.

“Potential hints at QE tapering in September would add further support to the dollar. Best protected will be those currencies where central banks are hawkish – such as in Canada and Norway,” Turner adds.

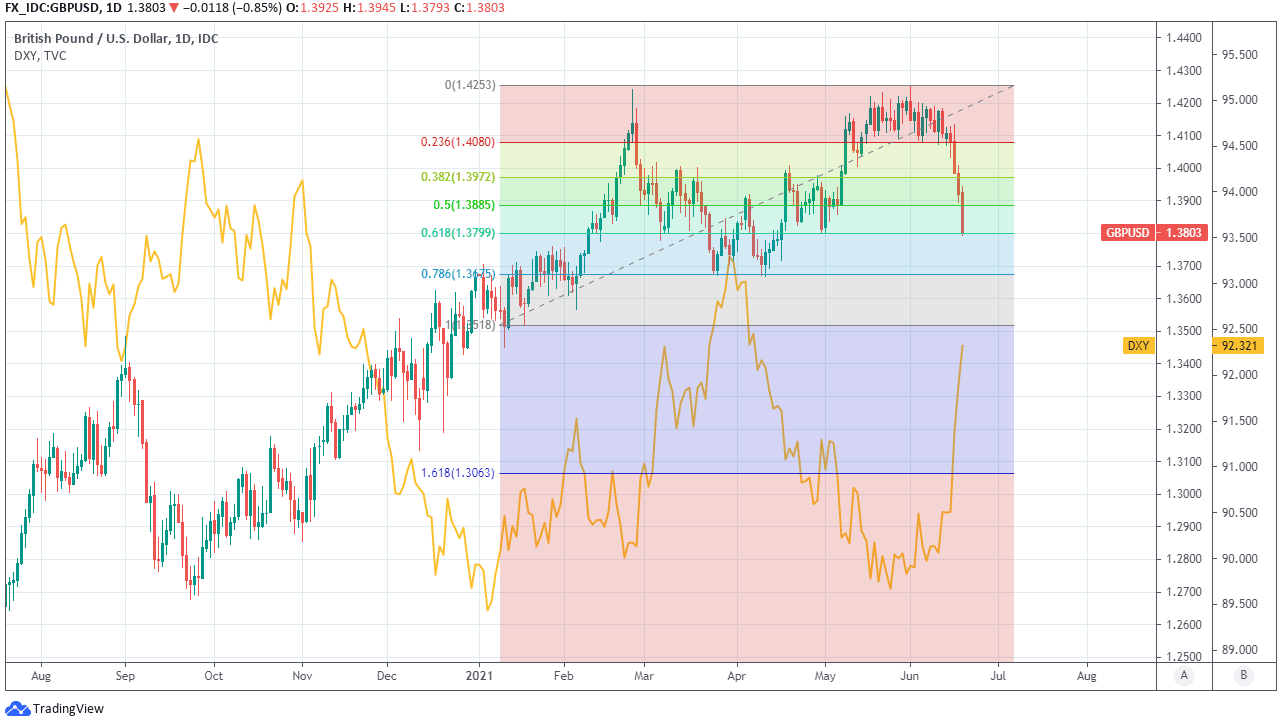

Above: Pound-to-Dollar exchange rate with Fibonacci retracements of April’s extension higher and U.S. Dollar Index (yellow).

If nothing else the Fed’s update and the market’s response to it render as questionable what were increasingly widespread suggestions that the bank’s policymakers were in danger of ‘falling asleep at the wheel’ as far as inflation is concerned, while also dissuading any notion that the Fed is anywhere close to giving up its spot as the world’s preeminent central bank.

Nonetheless, there’s scope for at least temporary confusion over the outlook for Dollar exchange rates with early doors implications for GBP/USD this week, given the pending reappearance of Fed Chairman Jerome Powell, this time before the House of Representatives’ select subcommittee on the coronavirus crisis at 19:00 London time on Tuesday: This is an ideal platform from which Powell could correct any market misperceptions, or hammer home a message that was evidently perceived by many as an almost-‘hawkish’ about-turn by the Fed on its monetary policy heels.

“The Fed delivered a hawkish surprise, signalling earlier tapering and rate hikes,” says Christian Keller, head of economic research at Barclays.

“The Fed’s message could accelerate the broader policy adjustment, with other major central banks having already started to taper and several EM banks hiking,” Keller adds, in an observation that could be all the more pertinent ahead of Thursday’s policy decision from the Bank of England.

{wbamp-hide start}

GBP/USD Forecasts Q2 2023Period: Q2 2023 Onwards |

Chair Powell’s Tuesday address comes before excursions by various other FOMC members onto the speaking circuit later in the week, and is almost certain to see him pressed about the outlook for monetary policy given that some members of congress and the government including Treasury Secretary Janet Yellen have expressed views on whether the bank has been too relaxed about risks posed by inflation.

U.S. inflation rose to more than five percent and twice the level of the Fed’s target of 2% on average, further fomenting what were becoming increasingly commonplace suggestions that the bank is somehow providing too much stimulus to the U.S. economy: Those rates of inflation however, are said by the bank to have as much to do with one-off “transitory” factors as they are the result of its policy support for the economy.

But investors, analysts and other observers were seemingly drawn to the Dollar last week, perhaps yet like moth to flame, by the Fed’s dot-plot back of rate projections although it matters that the bank has been seeking to generate more inflation than it has done in the past with an overachievement of its 2% target such that consumer price growth now averages that target for a period.

“The Fed certainly followed through on its delivery of a hawkish meeting, even beyond what we saw as the baseline risk. This is true not only in signaling two hikes in 2023 via its dot plot, but in Powell’s messaging on inflation,” says Kevin Cummins, chief U.S. economist at Natwest Markets.

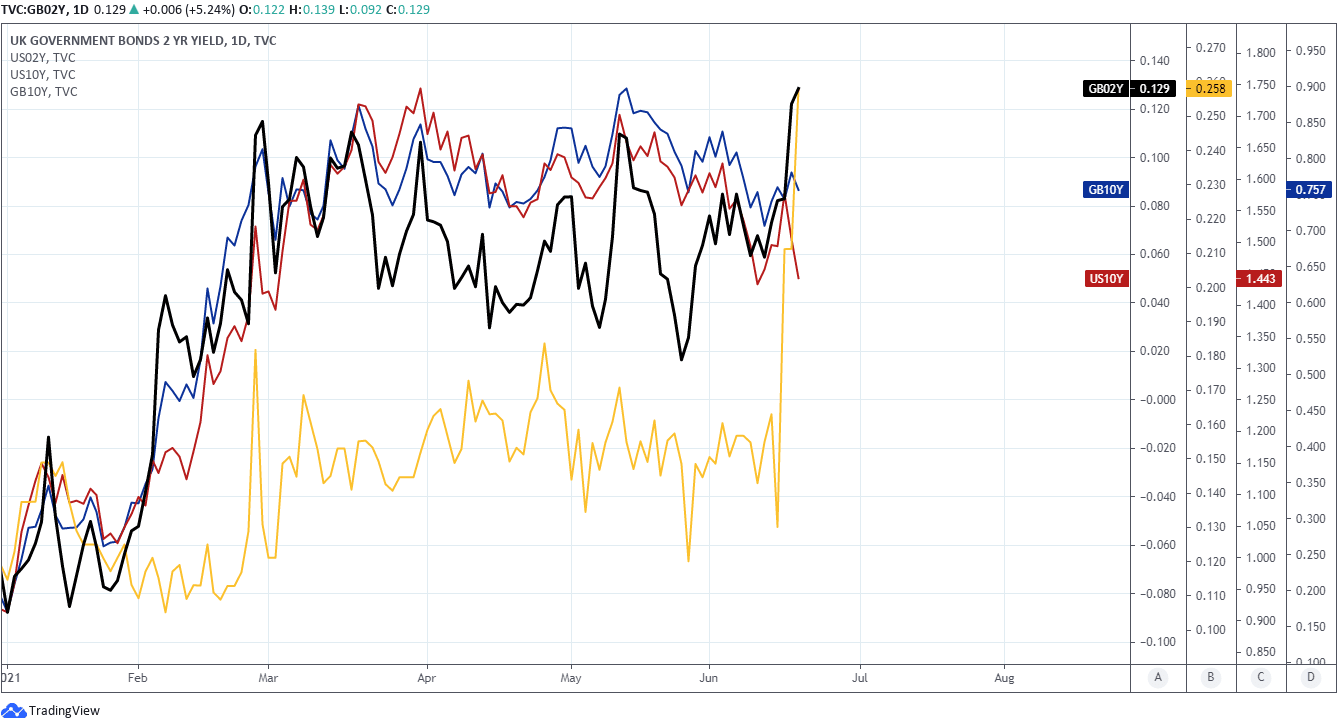

Above: UK and U.S. bond yields; with 2-year yields rising sharply as 10-year yields decline, creating a flattening yield curve.

“We suspect now that Powell started the process of preparing the public and financial markets for tapering, we expect chatter to increase over the summer (assuming job growth continues to make progress). Presumably, officials discuss tapering in July and September FOMC meeting, and formally announce the details of the plan in December before implementing it in early 2022,” Cummins adds.

It may be most pertinent in the week ahead however that Chair Powell already said in last Wednesday’s press conference that “we did not actually have a discussion of whether lift-off is appropriate at any particular year,” and that “dots are to be taken with a big grain of salt” because “the dots are not a great forecaster of future rate moves.”

It remains to be seen if these remarks are repeated before congress this week and if they are, whether the market receives the message, although any scenario which leaves investors with less motive to anticipate a change of policy any time soon would be supportive of the Pound-to-Dollar rate ahead of June’s monetary policy update from the Bank of England on Thursday.

This is the highlight of the week for Sterling and could provide the Pound-to-Dollar exchange rate with a late-in-the-week lift if the BoE also comes across as more concerned about upside risks to its own 2% inflation target than downside risks to the upbeat growth outlook set out in May, which may be more likely after last week when inflation figures for the month of May showed both the main consumer price index and the adjusted measure which overlooks energy prices each rising to or above the 2% level.

Nonetheless, the Pound-Dollar rate would still retain a downside corrective trajectory even if it’s able to retrace a full 50% of the June month’s decline from 1.4240 following the BoE’s pending decision, after having fallen from around 1.41 last Monday to 1.38 by Friday’s close: A 50% retracement of that move would leave GBP/USD trading around 1.4020 although with the Fed’s policy position potentially in flux it’s open question as to whether Sterling would be able to sustain even those levels.

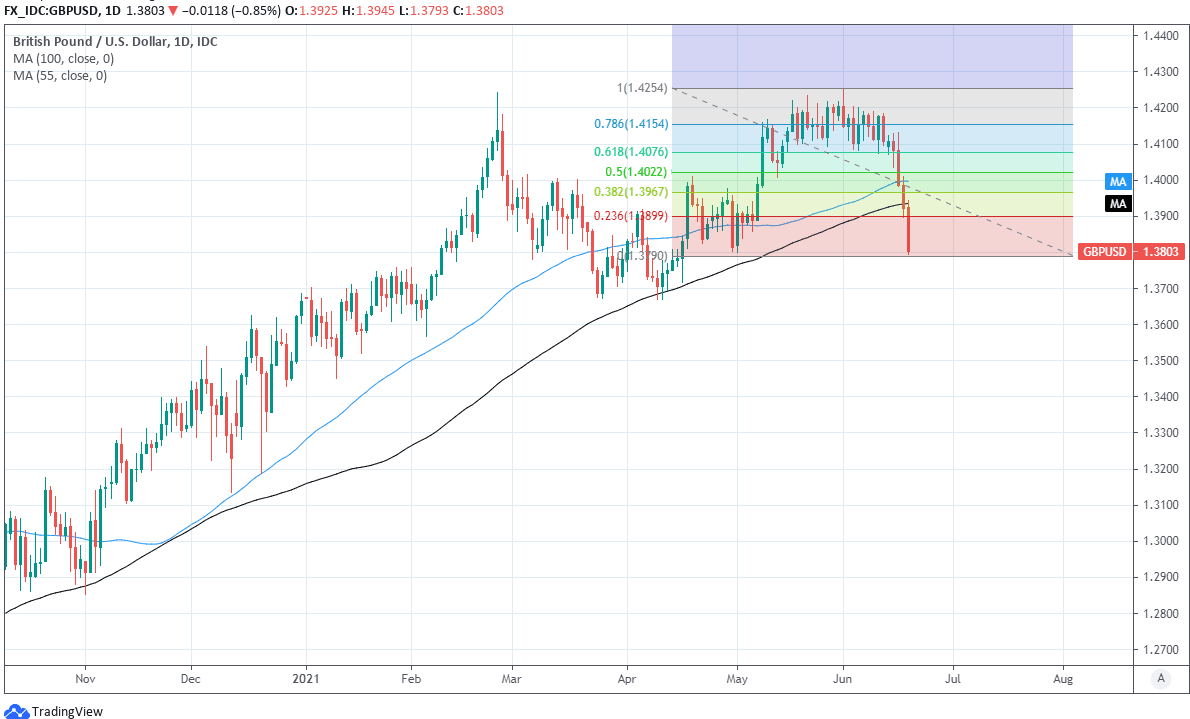

Above: Pound-to-Dollar exchange rate with Fibonacci retracements of June's correction lower and key moving-averages.