Image © Adobe Images

- GBP/USD spot rate at time of writing: 1.3726

- Bank transfer rate (indicative guide): 1.3347-1.3444

- FX specialist providers (indicative guide): 1.3521-1.3631

- More information on FX specialist rates here

New foreign exchange forecasts from ABN Amro and Commerzbank show the U.S. Dollar might already have bottomed out for at least the duration of 2021, a view that goes against a consensus market expectation for Dollar weakness in the year ahead.

Rising federal government spending under the new administration of Joe Biden is expected to be the key issue in determining the Dollar's outlook, as will an expectation for an outperforming U.S. economy.

"The result will be a much more rapid closure of the output gap; we now expect this in Q1 2022," says Georgette Boele, a senior FX strategist at ABN AMRO.

"A strong US economy makes US assets more attractive, as well as the dollar," Boele adds. "In addition, we think that inflation expectations are toppish. As a result, US real yields will improve, i.e. become less negative. These developments are supportive of the dollar."

The view goes against the consensus adopted by analysts this year, which is that rising federal government spending will lead to a wider U.S. budget deficit and higher inflation. This, when combined with steady zero percent interest rates at the Federal Reserve, is expected to continue eating into the 'real yields' offered by U.S. government bonds.

Meanwhile, a quickening economic recovery overseas is widely expected to add to the downside pressure on the Dollar in the short as well as medium-term.

Aove: U.S. Dollar Index shown at daily intervals alongside 10-year U.S. government bond yield (blue).

Biden's bid to bolster last year's $900bn fiscal aid package for households with a further $1.9 trillion of monies including direct cheques to households worth more than $2,000 each in total is expected to lift economic growth and also U.S. government bond yields, which is a potential draw for foreign investors.

Yields are the returns earned by investors who hold U.S. government debt and are expected to rise with the supply of U.S. bonds on the market as well as the recovery of the economy, which risks stoking inflation.

However, those returns could be augmented further and in real terms during the months ahead if ABN Amro is right about investors' inflation expectations likely having reached their peak, as this would signal at least an intermittent end to the decline in 'real yields.'

"Investors are already positioned for dollar weakness and euro strength. Speculators are considerably net long euro and net short dollar. Consensus among analysts is for the dollar to weaken further and the euro to rally. We long had this view as well. But we now think the dollar has bottomed," Boele says.

Boele and the ABN Amro team told clients this week the Euro-to-Dollar rate is likely to fall back to 1.20 by March and decline to 1.15 before year-end.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

If history is any guide to future outcomes then investors' inflation expectations may indeed have topped out after recovering prematurely from crisis lows, which could in turn signal a potential Dollar turnaround if the currency market remains at all concerned with 'real yield' and Biden's fiscal policy remains geared toward increased spending.

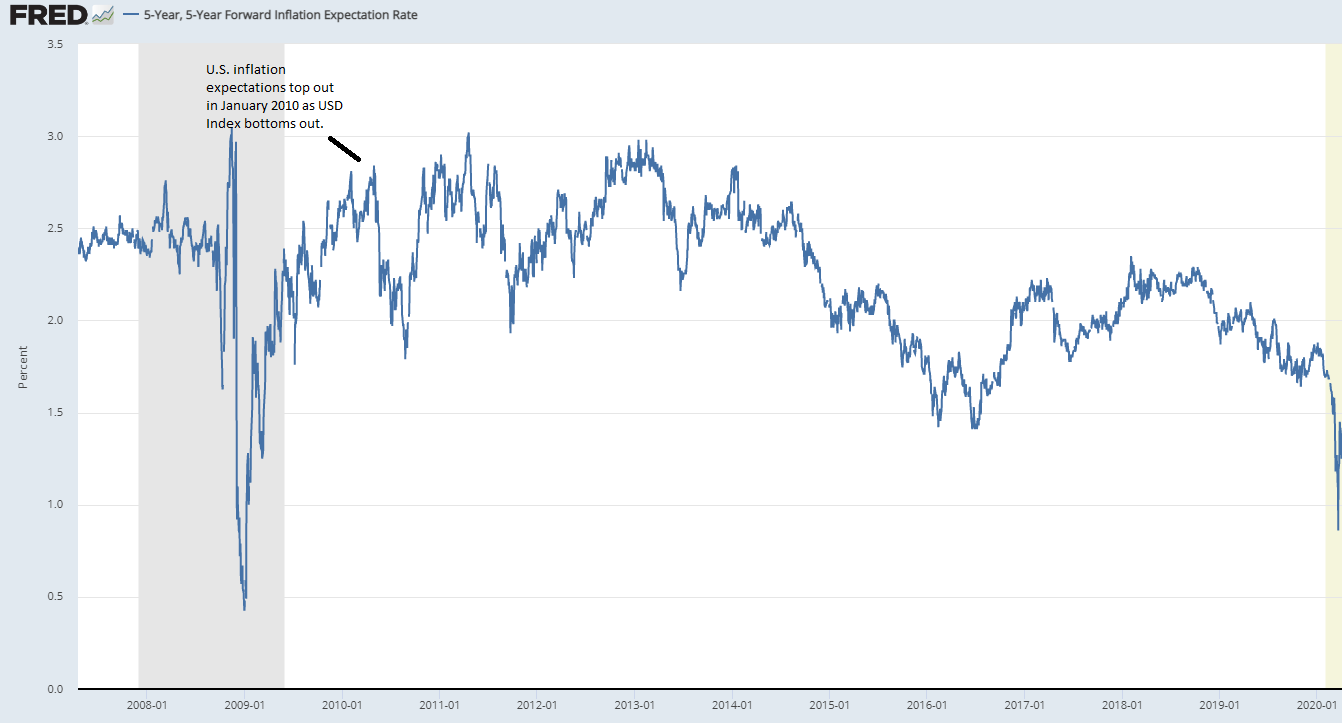

After all it was in January 2010 and at the same point the Dollar Index turned higher for a second time after the financial crisis that inflation expectations peaked, before subsequent declines threatened to lift real yields and provide a tailwind to the U.S. Dollar in the process.

Above: U.S. 5-year inflation expectations between 2008 and 2020. Source: Federal Reserve.

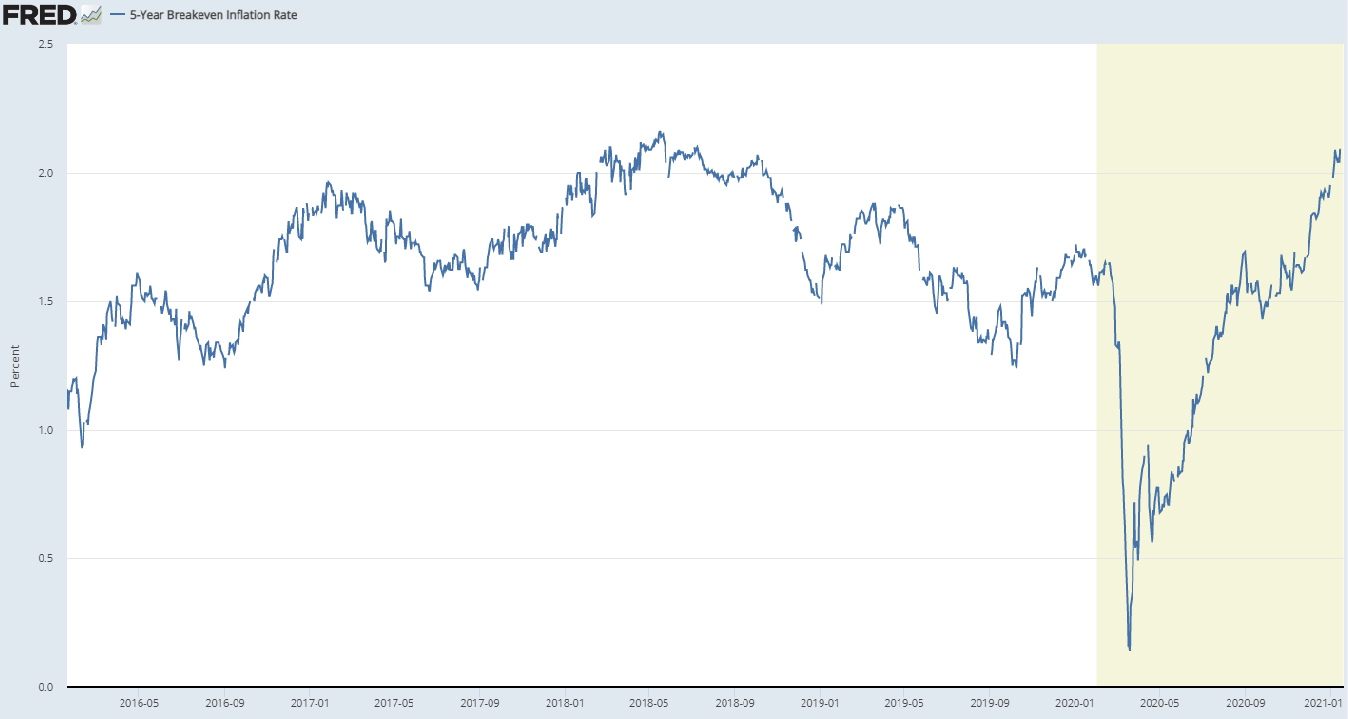

Above: U.S. 5-year inflation expectations in January 2021, returning to 2019 highs but remaining below 2010 levels.

"Higher inflation expectations are not primarily a signal for higher U.S. interest rates (which would make the dollar more attractive) but merely the prospect of a faster erosion of the greenback's domestic purchasing power, which would also make it appear less attractive on the currency market," says Ulrich Leuchtmann, head of FX strategy at Commerzbank. "However, the US fiscal package also has real economic consequences."

Investors' expectations for inflation over the a five year period have risen sharply in the last year, due in substantial part to a more-than 20% increase in some measures of the money supply that has roots in a record expansion of the Federal Reserve balance sheet associated with quantitative easing.

But both investors and policymakers have long overestimated inflation in the U.S. as well as almost everywhere else in the world, leading to persistent downside surprises between the financial and coronavirus crises.

"The high US growth rates we are expecting should improve the yield outlook for US securities and direct investments," Leuchtmann says. "This should also boost the U.S. dollar. After all, it is effectively the necessary entry ticket for U.S. investments. We therefore expect the dollar to strengthen across the board."

Leuchtmann forecasts that a temporary boost to U.S. growth will lead the Dollar to outperform this year, which is expected to push the Euro-to-Dollar rate back to 1.20 by March and to 1.19 before the end of June. However and thereafter the bank tips a recovery and return to this January's 1.23 before year-end.

The Commerzbank team cites an overvaluation of the Dollar which is expected to be corrected by permanent coronavirus-related damage to the U.S. economy and a deepening federal government budget deficit, the broad contours of which the U.S. currency has often appeared to follow over the years.

"We trust the currency market to start looking through the fiscal boom as early as the second half of this year. Like the bond market, it should then price out the special fiscal effects again bit by bit. What then remains are, on the one hand, the old arguments against the greenback," Leuchtmann says. "On the other hand, the expansionary fiscal policy generates new USD-negative effects."

Above: U.S. Dollar Index shown at monthly intervals with U.S. federal budget deficit (orange).