-USD spiral to extend in 2021 as politics collide with overvaluation.

-Regime change threatens U.S. energy independence, stokes deficits.

-As tax hikes constrain recovery, aiding a mean-reverting USD trend.

-Wild card win by Trump could offer short-term gains, correlation shift.

Image © Adobe Images

- GBP/USD spot rate at time of writing: 1.3098

- Bank transfer rate (indicative guide): 1.2740-1.2845

- FX specialist providers (indicative guide): 1.2900-1.2980

- More information on FX specialist rates here

The Dollar Index lifted off three-month lows on Thursday but the greenback’s downward spiral is a long way from over, according to BMO Capital Markets forecasts, with threats to U.S. energy independence, rising deficits and an onerous tax policy all seen encouraging further depreciation in 2021.

Dollars have been sold widely in recent months, leading to a -3.5% decline in the Dollar Index for 2020, with a range of factors seen behind the greenback’s mounting loss but none more pressing of late has been the prospect of a regime change in Washington.

“Our view on why the USD is falling is based primarily on the so-called reflation trade spurred by the Fed and other global central banks,” says Greg Anderson, CFA and global head of FX strategy at BMO. "Lurking in the background are darker USD fundamentals, which we don’t think are really in the price yet."

Source: BMO Capital Markets.

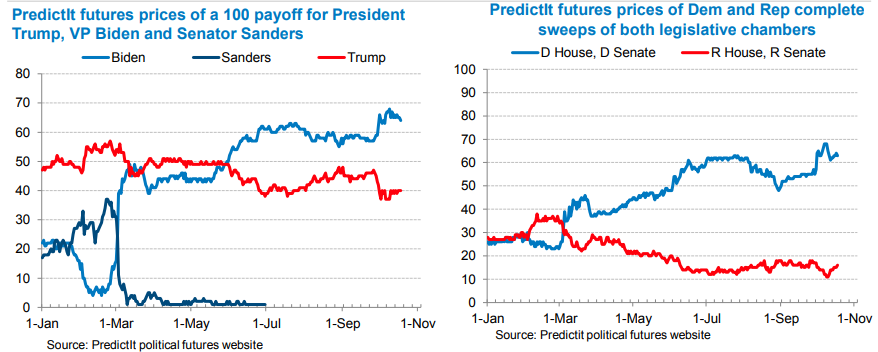

The incumbent President Donald Trump has, just like in 2016, been credited with little prospect of an election victory while opposition candidate Joe Biden of the Democractic Party remains the favourite for many pollsters with less than a fortnight to go before November 03 when Americans cast ballots in person.

A Democratic Party clean sweep is also BMO’s base case.

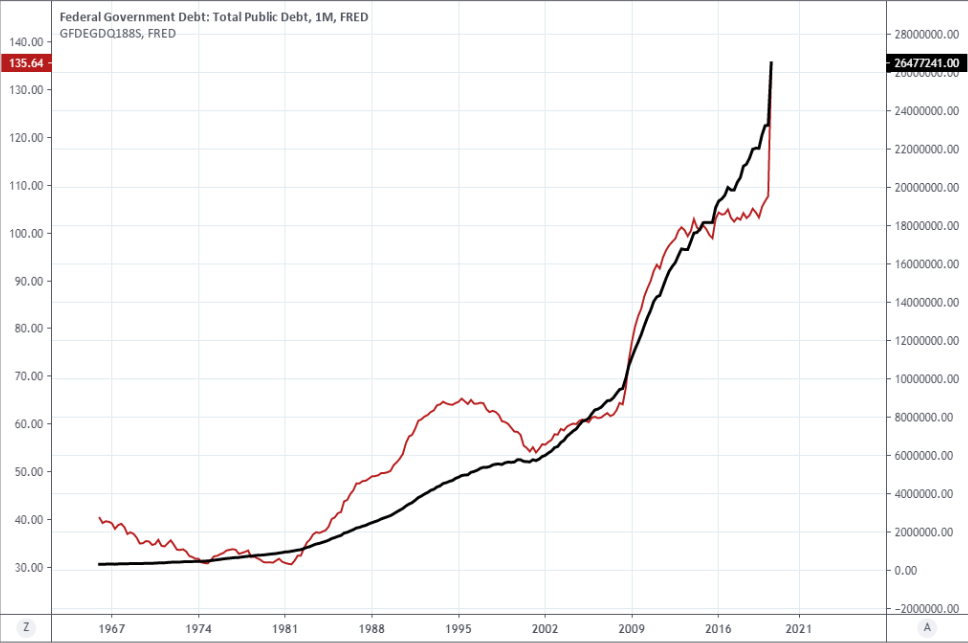

“Assuming our political base case, we look for US oil production to fade rapidly and for the US’s current account deficit to deteriorate sharply in 2021. With the fiscal deficit running at roughly 15% of GDP, the USD will again be an out-of-control twin deficit currency (like 2004-2007),” Anderson writes.

Source: Dollar Index shown at monthly intervals.

The Democrats’ White House hopeful is pointedly the polar opposite to the incumbent, particularly on economic policy and most notably in relation to the energy sector, which has been something of a golden goose for the U.S. in recent years but could be undone by a planned crusade against fossil fuels.

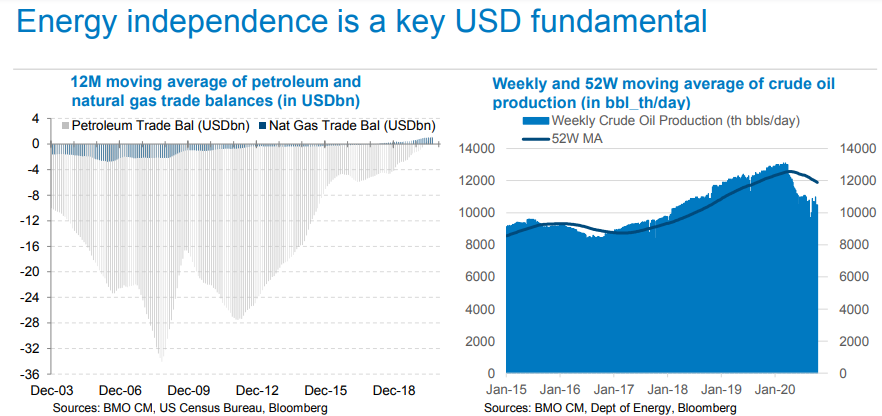

The advent of ‘fracking’ and horizontal drilling have enabled widespread production of shale oil and gas, contributing to huge gains in U.S. crude oil output that have cultivated an energy trade surplus that now sees America selling more oil to the rest of the world than is imported from it.

U.S. oil production rose from around 9 million barrels per day in 2016 to more than 13 million early in 2020, creating many jobs and an energy trade surplus in the process, while adding to GDP and sometimes lifting the Dollar.

“Biden will make a $2 trillion accelerated investment, with a plan to deploy those resources over his first term, setting us on an irreversible course to meet the ambitious climate progress that science demands,” Biden’s campaign website says, before also claiming his agenda will “ensure the U.S. achieves a 100% clean energy economy and reaches net-zero emissions no later than 2050.”

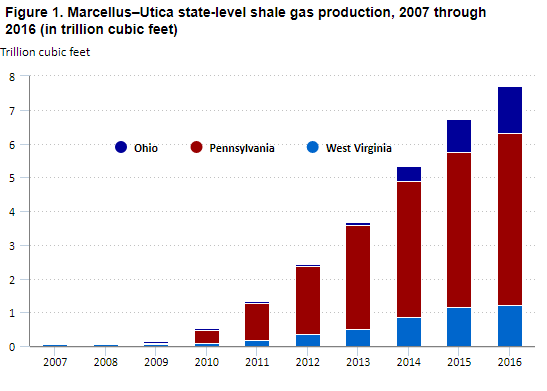

Above: Bureau of Labor Statistics graph showing growth of shale gas production in some key swing states.

President Trump has been criticised by the opposition and campaigners for lacking any climate plan, but Biden's plan is light on detail and his rhetoric in relation to it, sometimes self-contradictory.

Biden was reported to have claimed this last week that he wouldn't seek to cut natural gas from the U.S. energy mix, while still touting a plan that "achieves a 100% clean energy economy and reaches net-zero emissions."

The issue is almost certain to feature as a faultline for voters in at least some so-called swing states, where this election could be won or lost. Bureau of Labor Statistics figures show that much of the increased production of shale gas has been in places like Ohio, Pennsylvania, and West Virginia - all ‘swing states’ in which gainful employment could be threatened in an industry that's already struggling due to the coronavirus-related actions of governments.

“Shuttered production may not come back easily given low prices, industry consolidation and regulatory risk,” Anderson says, after noting pandemic-inspired declines in oil output. “The US energy industry likely needs help from DC to avoid further production deterioration as wells age out. That’s tough to imagine in a blue sweep scenario. The USD could quickly evolve back to being an oil importer currency.”

Source: BMO Capital Markets.

There aren’t many countries or policymakers who would be likely to want a stronger currency in the middle of an economic recovery much less while still mired in crisis, BMO says, but following any November clean sweep by the Democratic Party Washington will have multiple advantages in this regard.

The Dollar remains 8% above its long-term average even after its 2020 decline, according to Federal Reserve research cited by BMO, and is currently in the midst of a reversion that would be further encouraged by trade and current account deficits - otherwise known as ‘twin deficits’ - that are bolstered by energy woes, increased government spending and “tax hikes on corporations and the wealthy,” under the opposition's plans.

Tax increases could constrain the economic recovery and in the relative world of exchange rates, this risks handing other currencies a free lunch. However, and on the other hand, a wild card election win by President Trump would be likely to see 2018’s tax cuts remain in place while implying lesser increases in government spending and risking a return of international trade tensions that are typically supportive of the safe-haven Dollar.

“Is this the event that breaks the equities up = USD down correlation that has held all year? We suspect that it would be in the short run, with equities and the USD both rallying,” Anderson says of any Trump win, which BMO assigns only a 25% probability. “With the election out of the way, negotiations with the EU and others are back on the calendar for whenever COVID-19 is out of the way. This would be EUR-negative and USD-positive.”

Above: U.S. government debt in Dollars (black line, right axis) and U.S. debt-to-GDP ratio (red line, left axis.)

BMO forecasts a further -2.5% loss for the Bloomberg Dollar Index over the next 12-months, which is set to be aided by a Euro-to-Dollar rate rally from 1.18 to 1.21 late in 2020 and early next year. Europe’s single currency is however, expected to dip back toward 1.17 by the end of 2021.

Euro gains could be supplanted by an even larger increase in Pound Sterling, which is expected to rise from 1.30 to around 1.35 over the next three months in the event of a Brexit deal, a level it could remain close to for the next year.

Gains by the Japanese Yen, Canadian and Australian Dollars, Swiss Franc and Swedish Krona all also contribute to the envisaged U.S. Dollar fall next year, with USD/CAD seen ending 2021 at 1.28 while AUD/USD rises to 0.76.

“Regardless of when a deal or a series of deals is agreed, we expect Brexit to be on the ‘harder’ end of the spectrum and limited appreciation of the GBP out to 6M,” Anderson writes, in a quarterly review of BMO's forecasts. “CAD’s monetary and fiscal fundamentals mirror the US’s closely, so this is simply a USD call that has been projected onto USDCAD based on its ‘beta’. However, we do think other fundamentals like oil will prove CAD supportive.”