Image © Nazli Sart, Adobe Stock

- Pound-to-Dollar exchange rate in short-term downtrend

- Although oversold marginally likely to continue

- Pound eyes European elections for guidance

- Dollar eyes Federal Reserve communication

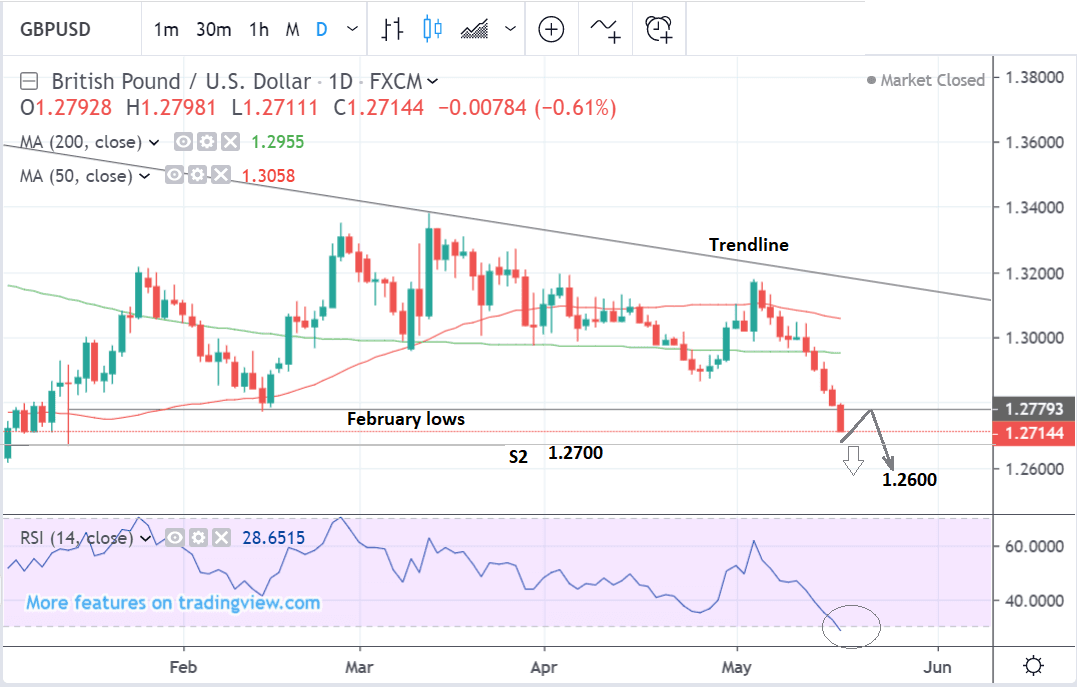

The Pound-to-Dollar exchange rate is trading at 1.2714 at the start of the new trading week after collapsing over 2.2% in the week before.

The decline came as a result of the collapse of cross-party Brexit talks which had promised to deliver a possible softer ‘customs-union’ Brexit but failed, while markets are preparing for the resignation of Prime Minister Theresa May and expressing caution that she will be replaced by someone more 'hawkish' on Brexit.

From a technical perspective, GBP/USD has established a short-term downtrend which is, on balance, more likely to extend than not given the assumption that the “trend is your friend” and therefore biased to continue.

There is a strong possibility, however, of a temporary short-term bounce or pull-back evolving due to the RSI momentum indicator reaching oversold levels classified as below 30 (RSI is at 29). This increases the possibility of a bounce occuring.

The pair is also close to reaching minor support from the R2 monthly pivot at 1.2704 (only 10 pips below), and the chances of a pullback at that level are enhanced.

Any pullbacks or corrections will probably return to the 1.2770 level of the key February lows before hitting a ceiling which may cap gains there. After that, they are likely to resume their descent.

A break below the 1.2704 monthly S2 pivot is eventually envisaged. This will probably lead to a continuation down to the next targets at 1.2600 and then 1.2500. A break below 1.2690 would probably provide confirmation of the second part of the descent.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement

The Dollar: Fed Dominates the Week's Calendar

Data is probably not going to be the key release for the U.S. Dollar as the releases scheduled for the coming week are not particularly significant.

Of interest though are likely to be the minutes of the most recent Federal Reserve (Fed) meeting in May, which will be released on Wednesday at 19.00 BST, as these are likely to give an insight into the debate by officials during the meeting before they voted to keep interest rates on hold.

Jerome Powell, the chairman of the Fed, said he did not see a strong case for moving interest rates in either direction at the press conference following the meeting suggesting a neutral official stance.

Some Fed policymakers, however, have indicated that they could lower interest rates if inflation does not pick up.

Fed presidents from Richmond, Boston and Minneapolis have gone further and expressed concern over whether a prolonged trade conflict might warrant a policy response because of the negative impact on the economy.

If the minutes appear to pitch the Fed in even a marginally more dovish (meaning in favour of lower rates) direction it will probably impact negatively on the Dollar.

The market is seeing a higher probability of a rate cut than rise, according to Fed fund futures, which calculate a 73.4% probability of a cut by the end of the year.

Trade tensions could also cause volatility, however, the impact on the U.S. Dollar isn't always clearly correlated.

When tensions worsen the Dollar sometimes rises because its emerging market counterparts weaken and it gains on safe-haven flows. There may also be a case for seeing the Dollar weaken, however, due to negative impact on the U.S. economy from tariffs.

The main risk is that the U.S. raises tariffs on a wider variety of Chinese imports, further inflaming the dispute.

The two main hard data releases for the U.S. Dollar are durable goods orders in April, out at 13.30 on Friday, and data on both existing and new home sales out at 15.00 on Thursday and Tuesday respectively.

Durables are likely to decline due to the grounding of the 737 Max because of a technical fault.

“The grounding of the Boeing 737 MAX and subsequent negative headlines have led to net cancellations, which will weigh heavily on April’s outcome as aircraft orders account for roughly 10% of the total. As a result, we expect total orders fell 3.8% during April,” say Wells Fargo in a client note on the matter.

Their estimate is more than the -2.0% consensus forecast.

U.S. housing data went through a bad patch, which is concerning since housing often leads the economy, however, Wells Fargo note the sector has seen improvement, so data this week may surprise to the upside.

“At least the recent pickup in the housing market remains on track. Housing starts rose 5.7% in April. Building permits also improved, and do not look to have been quite as low as previously thought. The pullback in mortgage rates, lower material costs, and improved builder sentiment should help to keep the rebound in residential construction intact,” say Wells Fargo.

Official estimates, meanwhile, are for existing home sales to rise 2.6% in April but new home sales to fall -2.8%. Data will clarify next week.

The Pound this Week: Euro Elections, Inflation Data

Overshadowing most data for Sterling will probably be Brexit risks and political uncertainty from the EU elections.

The Pound has nosedived since news cross-party talks fell apart. One catalyst for the disintegration has been the strong support polled by the new Brexit Party in the run up to the EU elections, on Thursday May 23, and correspondingly weak support polled by the Conservatives.

The inference is that Tory voters have changed allegiances and joined the Brexit party. This seems to be hardening the Conservative Party's stance on Brexit, widening the gulf between them and the other major parties.

Pressure is now also growing for the Prime Minister to resign, especially if her deal fails its fourth and final meaningful vote at the start of June, and Boris Johnson, who is a Brexit 'hawk', is the frontrunner to take over.

If he does it will increase the risks of ‘no-deal’ as we believe the next Prime Minister will pursue a policy of 'Brexit at all costs' come October 31.

“A poor showing by the UK Conservatives in the European Parliament elections could make it even more likely that Theresa May is replaced with someone that wants to deliver Brexit ‘no matter what’, keeping the Pound on the back foot,” says Raffi Boyadijian, an economist at FX broker XM.com.

Other events, however important during ‘normal’ times, are likely to be overshadowed by political risks, even inflation data out at 9.30 BST on Wednesday, May 22, and the testimony of the governor of the Bank of England (BOE), Mark Carney at 9.30 on Tuesday, May 21.

Inflation is expected to show a big rise in April, increasing by 0.7% on a monthly basis and 2.2% compared to a year ago. This would reflect a considerable acceleration from March when inflation only rose by 0.2% and 1.9% respectively.

Core inflation, which strips out volatile food and fuel components, is forecast to rise by 0.4% month-on-month and 1.8% compared to a year ago. This compares to 0.2% and 1.8% respectively in March. The core figure is not expected to show the same acceleration as broad CPI, as inflation recently has been driven primarily by rising oil prices, which impact on petrol prices.

Commentary from the governor of the BOE, Mark Carney, and other members of the BOE rate-setting committee, also potentially moving markets.

Although Governor Carney’s comments to the Parliamentary treasury committee may move the Pound, heightened Brexit uncertainty may make him ambivalent, and there is a risk of a U-turn from his May meeting confidence when he said investors should guard against complacency over inflation. The BOE’s stance at its May policy meeting was that it planned to raise interest rates over coming months at a "gradual and limited" pace.

Retail sales data is the final major release on the calendar, and is forecast to show a -0.4% slowdown from March, partly because of the outlying stellar performance in April when it rose 1.4%. It is forecast to rise by 4.6% compared to a year ago, after it grew 6.7% in March compared to the previous year. If sales are strong it could boost the Pound as it will show consumers continue to spend generously, which is a key indicator of overall economic growth for a nation.

* Advertisement