Image © Adobe Stock

- GBP/USD in sideways consolidation

- Break below 200-day MA required for bears

- Sterling driven by wage data; USD by

The Pound is forecast to track sideways against the U.S. Dollar over the near-term suggest our technical studies, but much of this week's action will depend on UK wage data out on Tuesday and a Dollar that appears to be experiencing a short-term soft-patch.

The Pound-to-Dollar rate is trading at 1.3065 at the start of the new week, up 0.25% from the week before but the decline over the course of the past month stands at a notable 1.64%.

The pair rose more because of developments that weighed on the Greenback with the mid-week update from the U.S. Federal Reserve appearing to have prompted selling action. However, we note that the Dollar has displayed an inverse response to improving global investor risk sentiment, and therefore the mood of the global market place could be a deciding factor for where the world's most liquid currency trades over coming days.

The declines in GBP/USD actually have little Sterling-supportive factors to thank, indeed, the news the Brexit deadline had been delayed till October 31, appeared to have little effect on Sterling and if anything sucked the wind out of the sails of 2019's best-performing currency.

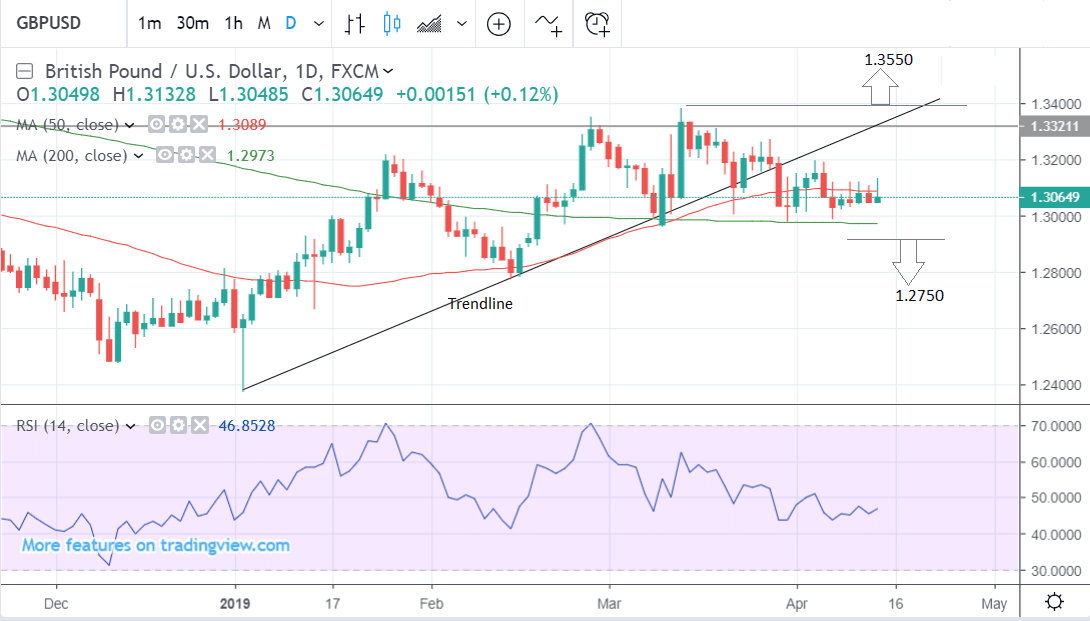

From a technical perspective little has changed since the previous week’s analysis when we wrote, “the pair has now broken below a key trendline and been rejected on a second retouch, which further confirms the break as decisive and suggests a broadly bearish wash to the technical picture.”

At the same time, the fact the market spent the whole previous week extending its sideways trend cautions against an overly bearish stance since this could merely be a lengthy consolidation before the next leg in the uptrend unfolds. Thus we are neutral overall, until a stronger move either way supplies confirmation.

The next development in the pair is probably dependent on whether the exchange rate breaks above or below the range highs or lows.

A break above the March 13 highs would probably provide the necessary confirmation for an extension up to a target at 1.3550, which is a strong resistance level made up of a combination of both the 200-week moving average (MA) and the R2 monthly pivot, a level used by traders to assess the strength of the trend, and a strong support and resistance level in itself.

Alternatively, a break below the range lows and the underpinning 200-day MA could signal a deeper bearish breakdown to a potential downside target at 1.2750-80 and the February lows, or even 1.2700 at the level of the S2 monthly pivot. Such a break would probably gain confirmation from a break below 1.2925.

The 200-day remains a tough obstacle to further losses. Large MAs often provide strong levels of support.

This is why we would ideally wish to see a break below 1.2925, for confirmation. A break below the MA on a closing basis would also provide bearish confirmation.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement

The U.S. Dollar: What to Watch this Week

Short-term momentum appears to have shifted to the downside for the U.S. Dollar, with the currency only being underperformed by the Japanese Yen and Swiss Franc last week.

That the Franc and Yen were the two underperformers immediately tells us something: markets took a decisive cue from global investor risk sentiment. The Yen and Franc are considered safe-haven currencies that benefit when global markets are being sold off, typically when investors take fright from any development or developments they believe bode poorly for global growth. The opposite performance by the Yen and Franc is true when markets are optimistic.

Often, the Dollar performs the same risk-haven function as its Swiss and Japanese colleagues, hence we believe the strong market response to improved Eurozone and Chinese data worked againt the Dollar.

"Risk appetite continued to recover last week, but this time G10 currencies performed better at the expense of the USD as confidence that a global recession could be avoided grew," says Timothy Fox, Head of Research & Chief Economist at Emirates NBD.

Therefore it could be that short-term developments in global investor sentiment are what matter for the Greenback over coming days.

Domestically, a welter of lower-tier data is scheduled in the week ahead and although none of the releases on their own are likely to be market moving, taken together, they may produce an effect on the Dollar.

The main consideration is whether they start to influence the outlook for Federal Reserve interest rate policy. The thinking is that although the Fed is not currently expected to raise interest rates in 2019 it may do if the data starts to improve.

“Economic releases out of the United States next week may not necessarily be very headline grabbing but could nevertheless steer the dollar in a more decisive pattern as investors ponder whether a Fed rate cut in 2019 is on the cards,” says Raffi Boyadjian, an economist at FX broker XM.com.

Last week saw slightly stronger-than-expected readings for both the key releases factory orders and inflation. If the trend spills over into the week ahead it could start to gently support the Dollar.

The Empire State manufacturing index is forecast to come out at a higher 8.1 in April from the 3.7 in the previous month when it is released at 13.30 BST on Monday.

“The New York Fed’s manufacturing activity gauge will be one of four indicators on US production, with investors hoping for the emergence of an uptrend. The various US manufacturing surveys have so far been mixed, so further convincing signs of a pick up in growth will be welcome by dollar bulls,” says Boyadjian.

The next manufacturing gauge to be released is the Philly Fed manufacturing index in April, which is forecast to show a slight decline to 11.2 from 13.7 previously. Again, a better-than-forecast result could support the Dollar if it forms part of a trend.

Official industrial production numbers for March are forecast to show a 0.2% rise from 0.1% previously when released on Tuesday,

April manufacturing PMI’s from data provider IHS Markit are forecast to show a recovery to 52.8 from 52.4 when released at 14.45 on Thursday. Services PMIs are forecast to decline slightly to 55.0 from 55.3.

March retail sales are forecast to show a strong 0.9% rise in April when released on Thursday at 13.30 BST. This may be partly due to the -0.2% fall in March.

Core retail sales, which omit autos and petrol, meanwhile, are forecast to rise by a slightly slower 0.5%.

“Along with the manufacturing data, the retail sales figures will be key in assessing the health of the US economy and hence, driving the greenback. Retail sales are forecast to have returned to growth in March after a surprise drop in February,” says Boyadjian.

The Pound: What to Watch this Week

With the deadline for exiting the EU now having been delayed Brexit will probably be less of a driving force for the Pound in the short-term. Bear in mind parliamentarians are also on their Easter break, therefore headlines should fade in frequency for this politically-charged currency.

Instead, hard data will become a more important driver again, and the highlight will likely be UK labour market data out on Tuesday, April 16, at 9.30 BST.

Of the various labour market stats which will be released average wages will be the most important.

Average earnings are expected to show a 3.4% rise in February compared to the 3.4% previously, and wages including bonuses, a 3.5% rise. Forecasts are quite high and if the actual figures are even higher it would almost certainly give a lift to the Pound.

The Bank of England is keeping a close eye on wages and have suggested they could raise interest rates in 2019 should wage rises continue to be robust. And, expectations for higher interest rates at the central bank tends to be a positive driver of Sterling.

"We are anticipating that average earnings will show a pick-up in the headline rate of income growth in the 3 months to February to 3.6%y/y while regular pay rises by 3.4%. This would reflect the tightness that we continue to see in the labour market amid ongoing delayed corporate investment spending," says Henry Occleston at Lloyds Bank Commercial Banking.

Jobs are forecast to have increased by 180k 3 months-on-3 months in January from 220k in the December, and expectations are the unemployment rate remained at 3.9%. The unemployment allowance claimant count is forecast to be 20k in March from 27k in February.

If wage data is strong it is expected to warn of better retail sales data when it is released on Thursday at 9.30 BST given the close relationship between the two.

Current forecasts are for retail sales to show a -0.3% fall in March from 0.4% in February and a 4.6% rise year-on-year.

The other main release for the Pound is inflation data for March out mid-week, which is forecast to show a 0.3% rise compared to the 0.5% increase previously, and a 2.0% rise compared to a year ago.

Higher inflation tends to drive up Sterling since it usually results in the Bank of England (BOE) having to raise interest rates, and higher interest rates tend to attract higher foreign capital inflows.

* Advertisement