Image © RCP, Adobe Stock

- Rising budget deficit warns of problems on the horizon

- U.S. Fed's rate hikes price in

- One analyst says call the top in the Dollar at your own peril

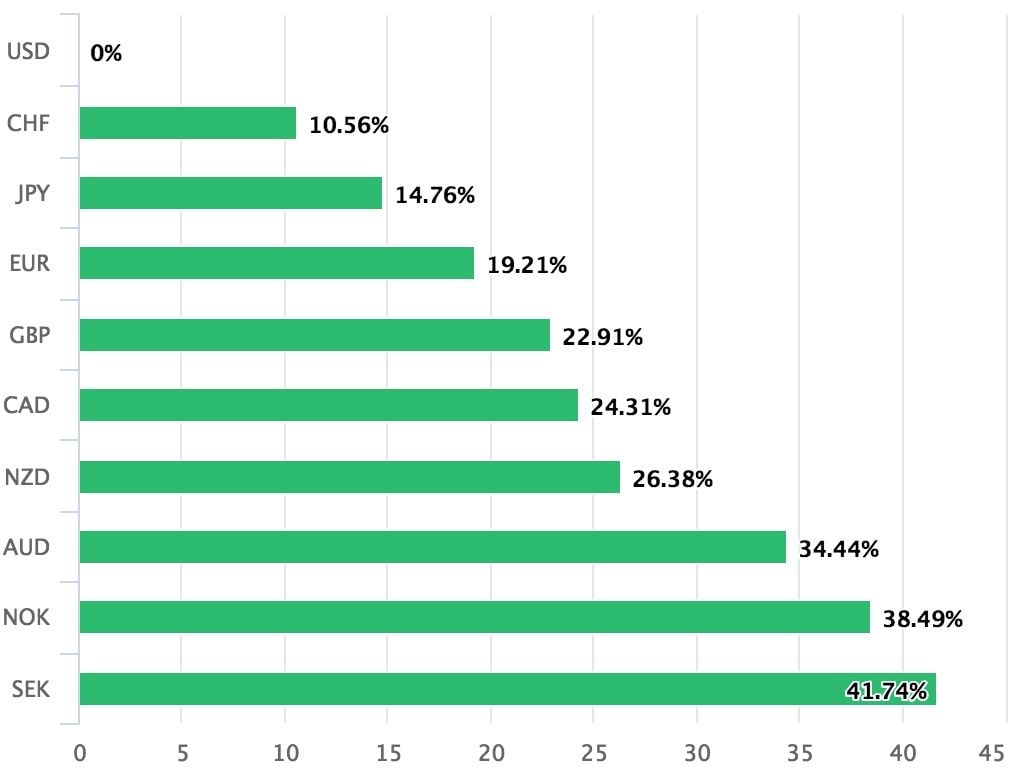

The U.S Dollar is still one of the better performing major currencies of 2018, with only the Yen and Norwegian Krone outperforming the Greenback in the G10 complex thus far.

But if we consider performances of the past five years we can see the Dollar is actually the best performer by some margin:

Image (C) Pound Sterling Live.

One question that is being increasingly fielded by readers and those in currency circles is whether or not the Dollar's long-term bull run is due to turn; questions that coincide with talk of stock markets now being "late cycle"; reference to a stock market that is in the final legs of a long running rally and about to turn lower.

The fortunes of the Dollar and the U.S. stock markets are of course ultimately tied to the fate of the U.S. economy, and the economy has enjoyed a strong expansion which is now in its 9th year - one of the longest expansions on record.

It is understandable that investors are wary of the good run ending, right across a number of asset classes.

But, currencies, stocks and economies don't always run together, and we see signs that the Dollar is a candidate for a turn lower.

Here we consider the validity of the arguments suggesting the Dollar is likely to trend lower over coming weeks and months and question whether or not the currency has indeed peaked.

Fed Rate Hikes Already Priced In

The Dollar's recent run of strength has been mainly due to heightened expectations that the U.S. Federal Reserve (Fed) will continue raising interest rates at a similar pace in 2019.

Higher interest rates usually boost a currency by attracting more foreign deposits drawn by the promise of higher interest returns, however, some analysts are arguing that the strong-Dollar has now fully priced-in these interest rate expectations and so may not rise any higher.

"Even in the short run, we believe that relatively strong growth and tighter Fed policy are largely factored into the exchange rate. Market positioning is also biased strongly towards long USDs by a number of metrics," says Shaun Osborne, chief FX strategist at Scotiabank.

Deficit Issues

The Dollar is at risk of being dragged down by a deteriorating fiscal position in the long-term which could weigh on US economic growth.

The U.S. administrations recent tax reforms have widened the budget deficit and although they have probably stimulated growth too, they could be storing up problems for later. The 'hangover' from the 'fiscal party' could be painfully felt, especially by the Dollar.

"We also feel that medium-to-longer run risks for the USD are tilted bearishly due to rising US deficits," says Scotiabank's Osborne.

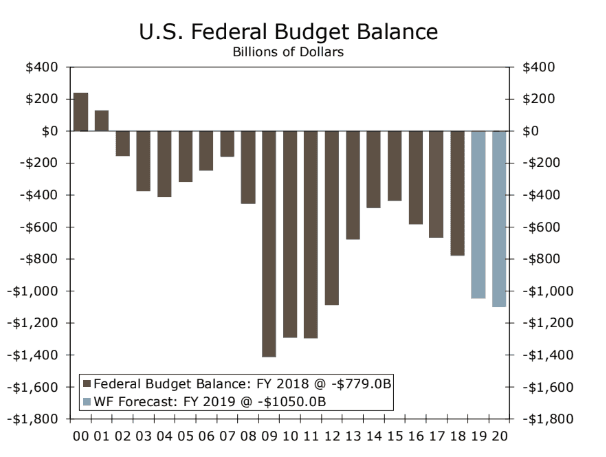

On Monday, the U.S. Treasury announced the federal budget deficit had widened to -$779bn for the fiscal year 2018. This was deeper than the -$666bn it forecast in 2017 and was the widest deficit for 6-years.

The accompanying statement, however, was optimistic that the deficit would eventually be reduced by increased tax revenues from rising growth.

"America’s booming economy will create increased government revenues – an important step toward long-term fiscal sustainability,” said Mick Mulvaney of the Office of Management and Budget Director.

In reality, total revenue growth in the US has risen only 0.4% in FY 2018, despite GDP rising 5.0%. The main reason for the lack of revenue growth is the massive 31% drop in corporate tax revenues, due to the generous tax cuts given to companies. Revenue from increased tariffs failed to make up the shortfall left by tax cuts and although they rose 20%, only contributed a paltry 1.2% to total taxes.

One concerning statistic for followers of the deficit is that repayments of existing debt contributed the fastest rising costs for the Treasury, increasing 24% for the year.

These may well rise further as the growing budget deficit along with the trade deficit will mean the US is forced to borrow money to pay for its new spending promises.

Rising borrowing costs in the US could also increase the cost of servicing the debt pile, putting even more pressure on growth.

The US budget deficit is set to widen to over $1 trillion in 2019 as spending continues to rise faster than tax receipts.

The widening deficit will probably result in federal spending cuts which will hit growth and this is seen as a major factor capping the Dollar's rise.

However, calling the turn in the Dollar could be a tricky prospect.

Chris Turner, head of FX at ING Bank, thinks the Dollar could still rise as long as U.S. interest rates are rising, and is only likely to end its uptrend when interest rates finally hit their ceiling, or the 'Fed Cycle' as Turner calls it, 'ends'.

"In terms of the overall outlook, until we see: (i) clear signs that the market has confidence where the top is for the Fed cycle and (ii) Washington softening its stance on China and trade, we would expect the Dollar to stay supported against emerging market and pro-growth currencies," says Turner.

A Move Lower is Likely, Even if it is Short-Lived

While calling the end of the long multi-year trend is could be premature, a shorter-dated turned lower might just be on the cards. Here the evidence is largely technical.

A Crowded Market

One increasingly negative sign for the U.S. Dollar is that bullish bets in the futures markets have become excessively overcrowded and this extreme level of 'optimism' amongst speculators is normally a contrarian sign that the currency is actually going to fall.

"Risk is growing that the dollar will fall further, especially as the speculative long Dollar trade remains crowded," says Martin Miller, an analyst at Thomson Reuters.

IMM data for the week ending October 09 showed the futures market net long was an equivalent cash position of $27.79 billion, up from $26.69 billion the previous week.

The long position has now been maintained for 17 straight weeks.

However, positioning is typically a technical consideration and could be more useful to explain shorter-term moves rather than a fundamental shift in fortunes and this argument might therefore not be suggestive of a turn in trend.

Technical Studies

The Dollar index - a broad measure of overall Dollar strength based on its performance against a basket of other currencies - is presently trading at 94.66. This is well off the highs of the upper 95s enjoyed in April.

And, technical studies suggest further downside is possible.

"The 94.986 Fibonacci level on the Dollar Index is seen as a 'make or break' level below which the Dollar would experience even deeper declines "to the 30-day lower bollinger band, currently at 93.965," says Miller.

Of course short-term downturns can morph into longer-term downtrends, but we would want soime technical confirmation for this first. The break below 94.99 is arguably a sign the short-term trend may already be bearish due to a reversal in sequence of lows and highs, or peaks and troughs.

A stronger indicator of a bearish trend would come from a break below the Sep 93.83 low.

That would be very bearish.

So while we might not be able to precisely call the turn in the Dollar, at least we will know what the turn looks like when it happens.

Advertisement

Lock in Sterling's current levels ahead of potential declines: Get up to 5% more foreign exchange for international payments by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here