The New Zealand Dollar is currently has been one of the best-performing currency in G10 over the course of the past month, but analysts at JP Morgan warn they don’t see the good times lasting and adopt a negative stance regarding future expectations.

The move higher in NZD was rooted in a notable pickup in terms of trade and data surprise momentum.

A major mid-year review of the global foreign exchange market place conducted by JP Morgan suggests the remainder of 2017 could see weakness, in constrast to the more positive views held at their rivals.

As mentioned, for now momentum lies with NZD: the Pound to New Zealand Dollar is meanwhile also struggling having fallen for three months in a row now and is seen at 1.7550. The New Zealand Dollar is currently trading at 0.72 against the Dollar following a strong four-week rally.

JP Mogan forecasts point to NZD falling to 0.68 in Q3 before ending the year at 0.65.

We explore the reasons why they are so bearish the Kiwi.

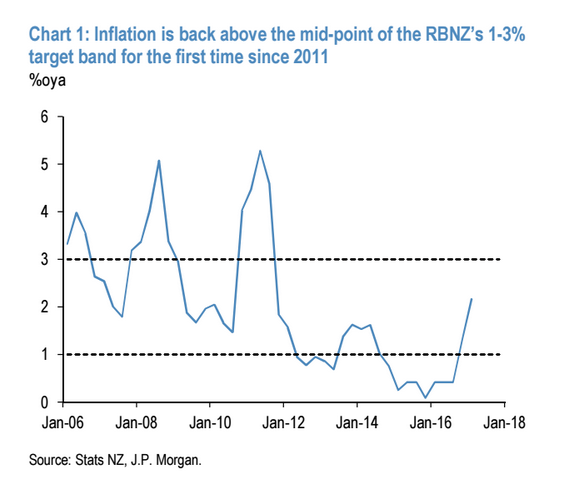

1. Inflation is not sustainable

Inflation has bounced to above 2.0% and this might warrant a rise in interest rates but J P Morgan say it is not sustainable.

Higher interest rates tend to increase the value of a currency by attracting more flows of capital, but in this case the inflation is primarily ‘tradables-driven’, and therefore unlikely to persist.

Tradables inflation means inflation from goods susceptible to international macroeconomic cycles such as commodities, raw materials and foods which are grown or resourced in other countries.

What J P Morgan are saying is that the rise in inflation is probably temporary as it reflects the rise in commodity prices over the last six months.

2. Tightening is not necessary

Even if there is an argument for raising interest rates due to higher inflation J P Morgan say there is no real need as financial conditions have already been adequately tightened through other means.

These include using macro-prudential policies which restrict mortgage lending and control bank credit.

The argument is that these have now dealt with the risks from cheap lending overheating the housing market or the economy in general.

3. The Reserve Bank of New Zealand (RBNZ) will remain on hold

“Our view is that that RBNZ will be on hold through 2018,” say J P Morgan in their note, meaning that they will neither raise or lower interest rates.

“RBNZ officials appear very cautious on the risks to financial stability from rising mortgage rates, given that household debt has increased so sharply in the last couple of years,” they add, which at least discounts the possibility of a rate cut.

4. GDP is peaking

GDP has been strong in New Zealand, due to strong net immigration but the market has become almost complacent to this trend, when actually it should be concerned that it might not last.

“The market has become accustomed to very strong GDP outcomes in New Zealand over the last few years. Even though the fundamental support for growth from the immigration boom – cosmetic as it is – is still in place, some of the luster is coming off the activity data recently,” said J P Morgan.

5. Weaker than Expected GDP

Following on from 4, growth was weaker-than-expected in the second half of 2016 and will probably be soft in the first half of 2017 thereby keeping a cap on the Kiwi.

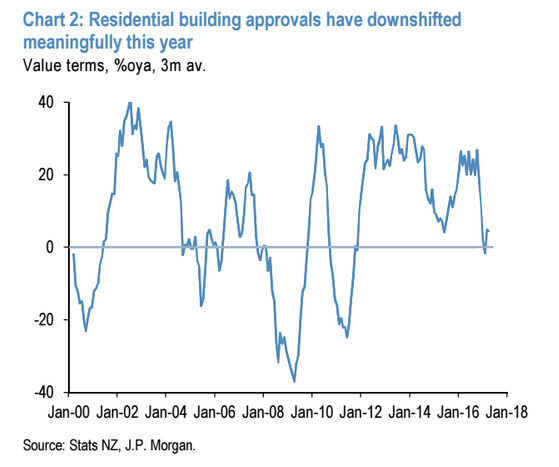

6. Housing is stuttering

Data appears to show the housing market peaking and rolling over after several extremely strong years.

Investors should be mindful of the sage old advice that “housing leads the economy” - it has rarely been proven wrong.

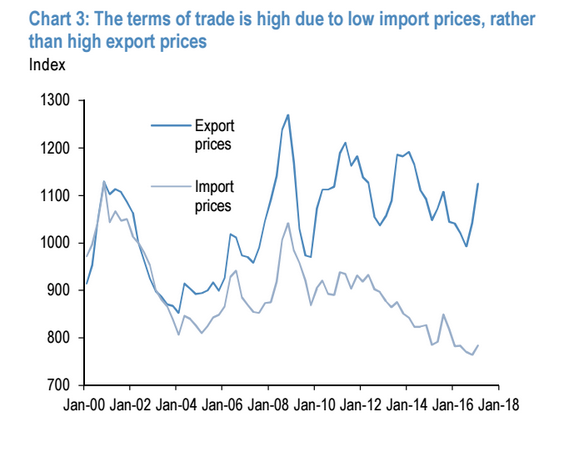

7. Improvement in ‘Terms of Trade’

The improvement in the ‘Terms of Trade’, which is the ratio of import prices to export prices normally increases the value of the currency, however, J P Morgan don’t see this as likely in the case of New Zealand, where the improvement was mainly due to a fall in import prices not appreciation of exports, and so had no real impacted on the current account.

8. Current account surplus has waned

Regardless of the Terms of Trade ratio, the Trade Balance or any other trade components of the Current Account, surpluses are rarely held onto in New Zealand, and it is surpluses which help a currency evaluate.

This is due to the country’s low savings rate.

9. NZD economy is ‘fully priced’

J P Morgan argue that the NZ economy is actually ‘fully priced’ into the Kiwi Dollar so it is harder to achieve further upside and the risks are therefore more to the downside.

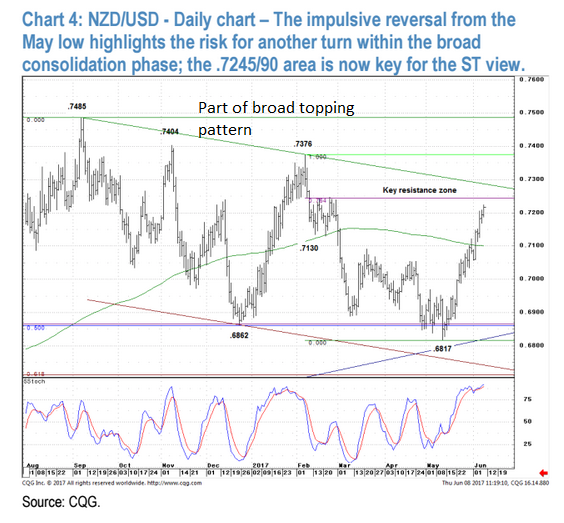

10. Major top on charts

There is a major long-term topping pattern forming on NZD/USD which is likely to eventually assert itself and lead to a tehcncial breakdown.

Although the recent rally is still intact and a deeper correction would be required for them to adopt a stronger bearish bias in line with the fundamental analysis.

“While we can still make a case that NZD/USD is forming a broad topping pattern below the September ’16 peak, the impulsive nature of the reversal from the low has put this bearish view on the backburner for now,” remarked J P Morgan’s analysts.

JP Morgan are not alone in their stance on NZD.

Analysts at TD Securities have today briefed that they think the near-term picture is likely to turn less supportive for the currency.

"For one thing, NZD remains one of the most yield-sensitive currencies in the G10 so our call for a hawkish hike this week increases the risks the of a squeeze," says Richard Kelly, Head of Global Strategy at TD Securities.

It has also overshot the levels implied from our HFFV and it is now one of the most expensive currencies in the G10, tracking over 2- sigmas from Kelly's estimates.

TD Securities think this excessive valuation leaves it vulnerable to a shift in either internal or external drivers.