- GBPNZD pullback can extend further short-term

- But the medium-term trend remains positive

- Watch Bank of England, UK inflation this week

- NZ dairy auction, GDP and current account in focus

Above: NZ dairy industry data is due this week. Image © Adobe Stock

The British Pound continues a corrective pullback against the New Zealand Dollar that can extend further over the coming days, although Thursday's Bank of England decision and some important data releases out of New Zealand will offer two-way volatility.

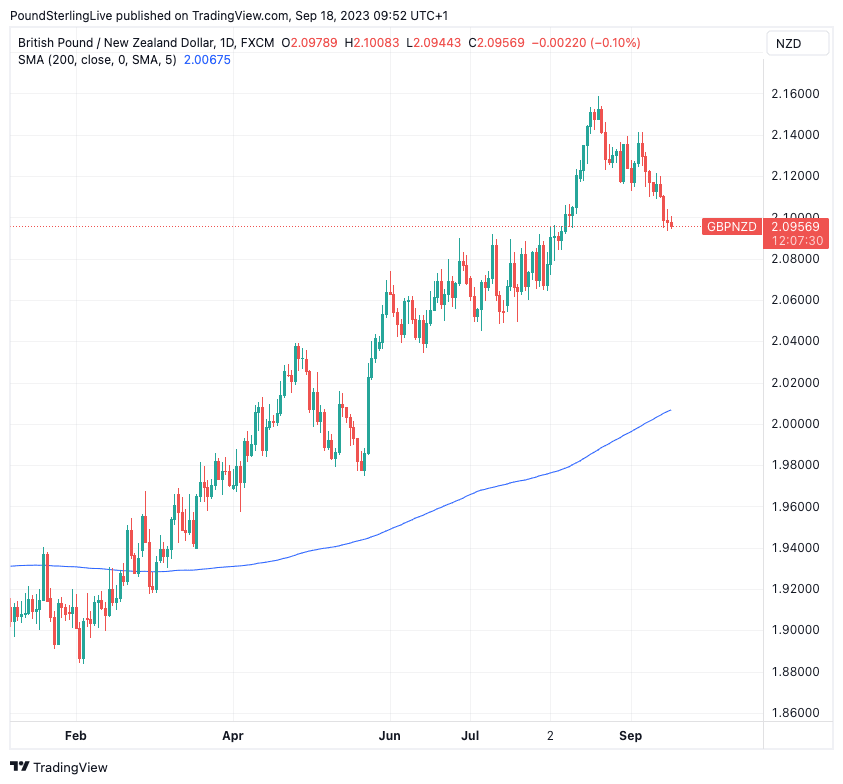

The Pound to New Zealand Dollar exchange rate (GBPNZD) has now retreated 3.0% from its August multi-year highs at 2.1590 as it quotes at 2.0950 at the time of writing, a move that still looks corrective at this juncture.

We are still inclined to call it corrective as the GBPNZD remains above its 200-day moving average (currently at 2.0067) and we would judge the medium-term (multi-week) trend to be in positive territory as long as it stays above this momentum indicator. (Note that GBPUSD has broken below its 200-day MA and we have therefore called an end to the 2023 uptrend as a result).

Above: GBPNZD at daily intervals, with 200-day MA annotated.

As such, the current weakness is still viewed as corrective and until a break below the 200-day MA occurs we would expect the positive trend to reboot at some point.

The current rebound in the New Zealand Dollar is linked to some better-than-expected data out of China which has improved sentiment towards the world's number two economy which has struggled to impress in the post-Covid period.

China's tepid recovery has weighed on the Kiwi Dollar owing to New Zealand's strong trade links, particularly in the agricultural sector. Therefore, a sense that the worst of the Chinese slowdown is in the past could aid sentiment towards the New Zealand Dollar.

"August economic data shows some signs of stability in China’s economy, particularly manufacturing and retail sales appear to have bottomed out. Our GDP expectations for China have been revised up for this year to 5.1% (from 4.9%) while 2024 is expected to deliver growth of 4.2%," says Susan Kilsby, Agricultural Economist at ANZ.

In the week ahead, most domestic interest will probably centre on Thursday’s June quarter GDP report.

Thursday sees the release of New Zealand GDP with the market looking for growth of 0.4% in the second quarter, which should mean the recession ended during this period. "Another piece of the economic puzzle (GDP) is due on Thursday. We will see how the Kiwi economy performed over Q2. And we’re expecting payback for the stunted growth over summer. We expect output rebounded 0.6%," says Jarrod Kerr, Chief Economist at Kiwi Bank.

"The underlying picture is that the economy is losing momentum, with annual growth expected to slow to 1.5% from 2.2% previously. Our forecast is above that of both the market and the RBNZ. But given the uncertainties surrounding this data, we think that the RBNZ will be insensitive to small deviations from its forecast," says Darren Gibbs, Senior Economist at Westpac.

Wednesday’s GDT dairy auction should garner some attention and Westpac looks for whole milk powder prices (WMP) to rise 3% at the upcoming auction. (Note WMP prices jumped by around 5% at the previous auction.)

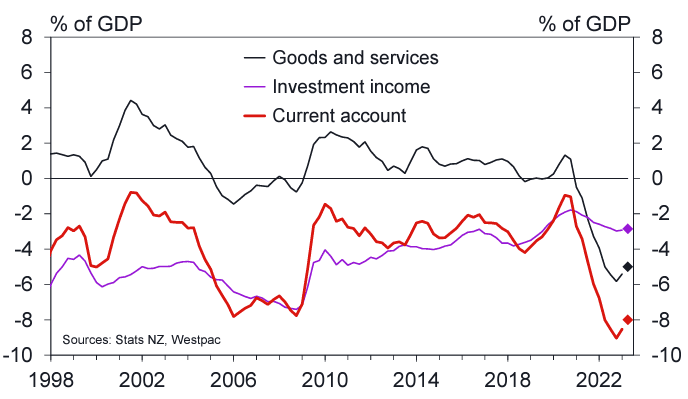

Above: NZ current account deficit has deteriorated sharply, image courtesy of Westpac.

"Prices appear to be finding a bottom after a sustained run of price falls. However, the spring peak in local production is around the corner and its strength or otherwise will provide fresh direction to prices. Heading into 2024, we anticipate that rebounding Chinese demand will lift prices, although there are downside risks as to the timing and magnitude of any price recovery," says Gibb.

Current account data is also due Tuesday with economists expecting the country to be firmly stuck in deficit, a negative situation for the New Zealand Dollar on a long-term fundamental basis.

"The blow-out in New Zealand’s current account deficit over recent years has been a symptom of an overheated economy. In other words, we have been spending beyond our current means," says Gibb.

That said, the current account deficit has turned the corner this year and is starting to narrow.

Image © Adobe Stock

The Bank of England and UK inflation data are two events that could offer some meaningful support - or otherwise - to GBP this week, thus determining whether GBPNZD can stabilise its current pullback.

The Bank looks keen to signal the end of the rate hiking cycle is close, even as it delivers another 25 basis point hike in response to elevated inflationary levels.

The risk for Pound Sterling is that it makes a hash of navigating a tricky juncture that triggers a sell-off, as was the case throughout the duration of 2022.

"Will BOE indicate a pause after hiking 25bp next week? If so, GBP should have room to drop," says Anders Eklöf, an analyst at Swedbank.

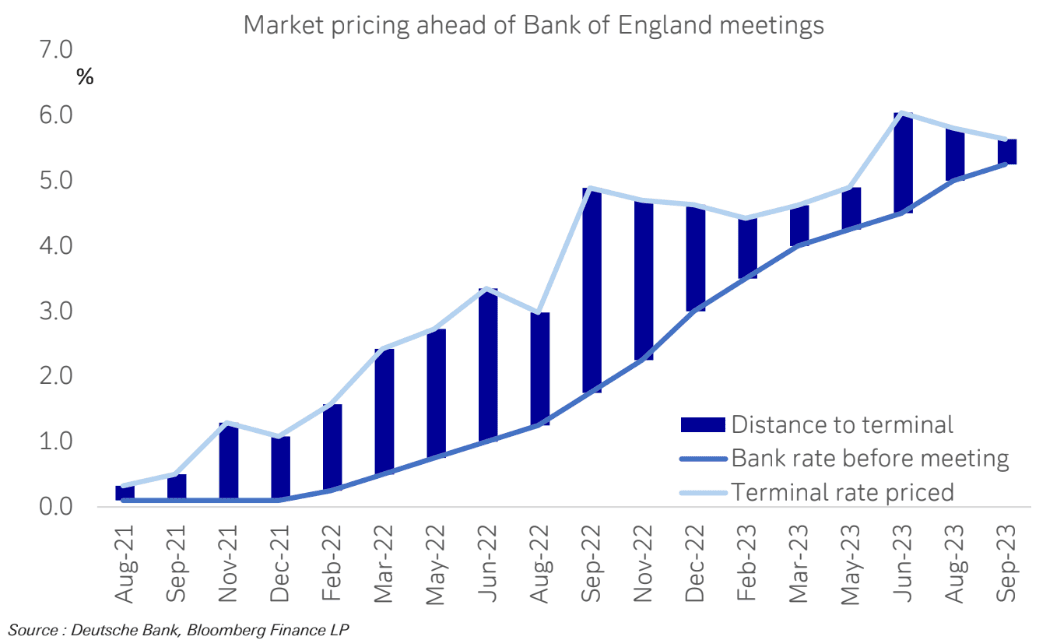

Above: "Market pricing suggesting the BoE are finally within striking distance of the terminal rate" - Deutsche Bank.

Bank of England Governor Andrew Bailey contributed to Sterling weakness when he appeared before members of Parliament's Treasury Select Committee and explicitly stated the Bank was close to reaching a peak in interest rates.

The subsequent adjustment lower in UK rates and the Pound therefore suggests much of the downside that comes from a 'dovish' turn might already be accounted for, limiting potential GBP weakness at the event itself.

Wednesday's inflation release comes ahead of the Bank's decision and it is hard to see any upside for the Pound coming from this data set.

A stronger-than-expected inflation figure (expectations: 7.1% y/y, core expected at 6.8% y/y) would normally be associated with strength in the Pound, but markets might not reward such a print if it suggests the UK's stagflation problem is more acute than previously expected.

A downside miss will also simply suggest the Bank of England can afford to relax in November, egging on the recent trend of GBP weakness.

On balance, however, the non-staglationary signal of a below-consensus print is likely more supportive of the Pound on a longer-term basis.

"The MPC's hope will be that Wednesday's CPI print doesn't now raise pricing - and thus raise the stakes for sterling - right before their decision," says Shreyas Gopal, Strategist at Deutsche Bank.