![]()

Image © Adobe Stock

One of New Zealand's largest lenders says the New Zealand Dollar is likely to struggle over the remainder of 2022 amidst ongoing headwinds to global markets and as the Reserve Bank of New Zealand fails to live up to lofty expectations.

Researchers at BNZ maintain a cautious tone on the New Zealand Dollar's prospects as part of their mid-year assessment of global and domestic markets.

"We remain sceptical that the bad macroeconomic environment we see developing further over coming months is 'fully' in the price and we continue to see the NZD as vulnerable to further downside pressure in Q3," says Jason Wong, Senior Market Strategist at BNZ.

Global economic and financial developments are to remain "difficult" says Wong, which should ensure headwinds remain for the pro-cyclical New Zealand Dollar.

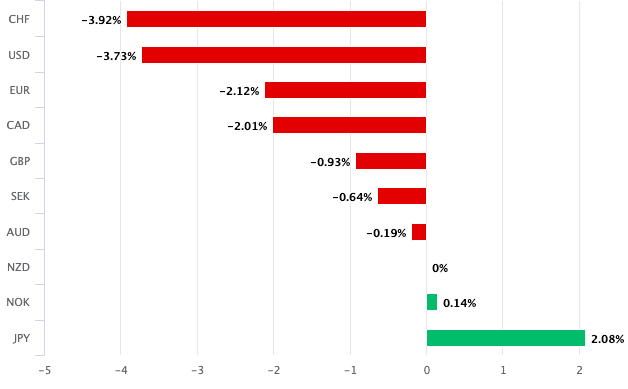

Above: The NZD is one of the laggards of the past month.

The New Zealand Dollar's pro-cyclical nature means it tends to rise alongside global stock markets and struggle when markets are in decline.

Indeed, the NZ Dollar has been supported over the course of the past week helped largely by a recovery in global stock markets.

Should this improvement in investor sentiment continue then the New Zealand Dollar can benefit further, but is the bottom in or is this a bear market rally that will ultimately fail.?

"The message from all these market movements seemed to be less concern about global economic recession risks, and less concern about the inflation outlook, seeing a significant paring back of monetary policy rate hike expectations. A more sceptical take would be that this is just a temporary reversal of recent market movements and not too much should be read into them," says Wong.

The improvement in global risk sentiment seen over recent days comes as investors pare back expectations for the number of hikes still to come out of global central banks.

This comes as investors price in falling commodity prices and greater risks of an U.S. recession.

Less hikes at the major central banks inevitably means less restrictive financial conditions going forward than had been previously assumed for consumers and businesses and is therefore supportive for investor sentiment.

This reappraisal is also relevant to the Reserve Bank of New Zealand (RBNZ).

"The global moves have seen a paring back of NZ rate hike expectations, with July OIS closing the week at 2.55%, now suggesting only a small chance of a 75bps hike, a big drop from mid-month where the implied OCR change priced in had reached 70bps," says Wong.

BNZ maintains a view that 75bps hike increments are unlikely.

RBNZ policy direction matters as a higher Official Cash Rate means higher returns for New Zealand sovereign bonds, which in turn creates a supportive flow dynamic for the New Zealand Dollar.

Therefore if the RBNZ indicates less hikes than the market is expecting the NZ Dollar could come under pressure.

"The RBNZ will find last week’s poor NZ consumer confidence data, with the Westpac measure falling to a record low, was a reminder of the vulnerability of the NZ consumer and the Bank has no need to rock the boat with super-sized rate hikes," says Wong.

BNZ forecasts the New Zealand Dollar to Pound exchange rate at 0.52 by the end of September and 0.54 by year end. This gives a Pound to New Zealand Dollar exchange rate of 1.9230 and 1.85. (Set your FX rate alert here).

Their NZD/USD forecast is for 0.63 by the end of September and 0.64 by the end of the year.

BNZ's NZD/EUR exchange rate forecast rests at 0.61 for the end of September and 0.63 for year end.

BNZ's calls echo those of BMO Capital Markets whose latest assessment of the New Zealand Dollar suggests it will remain in the slow lane, hampered by New Zealand's ongoing reliance on energy imports.

"With very little travel exports and the surging price of energy imports, NZ’s trade deficit has ballooned," Greg Anderson, Global Head of FX Strategy at BMO Capital Markets.

In a monthly foreign exchange forecast update analysts at BMO also say the New Zealand Dollar would also struggle as the RBNZ could be amongst the first major central banks to call an end to its interest rate hiking cycle.

New Zealand "had its moment as a nation when its economy seemed the most COVID resistant in the G10, which allowed the RBNZ to lead out in tightening monetary policy," says Anderson.

"Despite NZ having the G10’s highest overnight rate (with the RBNZ at 2.00%), NZD hasn’t fared well during the global tightening phase," says Anderson.

"We're getting close to where markets will start to speculate about which central banks will stop tightening first," adds Anderson. "The RBNZ is probably the lead candidate."

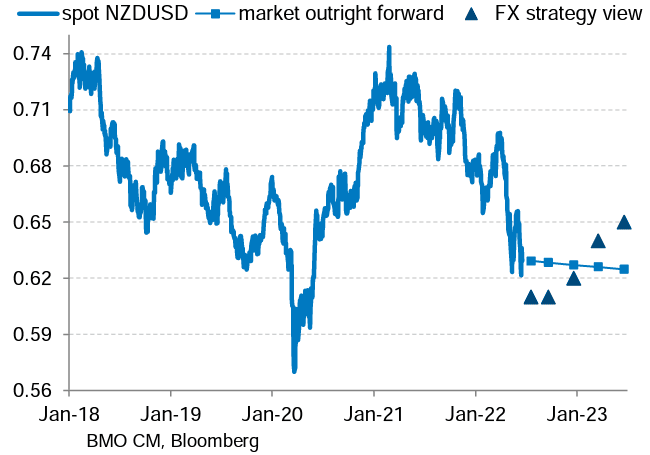

Above: BMO's NZD/USD outlook.

BMO Capital forecasts the New Zealand Dollar / U.S. dollar exchange rate to trade at 0.61 over a one month horizon, 0.61 over a three month horizon, 0.62 over a six month horizon and 0.65 over a one year horizon.

Given spot is currently at 0.6315 this implies further underperformance over the near- to medium-term which has implications for other NZD crosses.

Such a profile could keep the Pound propped up against the NZ currency and implies the potential for some further, albeit modest, upside.