Image © Ash T Productions, Adobe Stock

- GBP/INR still in downtrend despite Brexit bounce

- Technical downtrend to extend

- Brexit the key to Sterling

- U.S. Dollar and U.S. mid-terms could impact Rupee

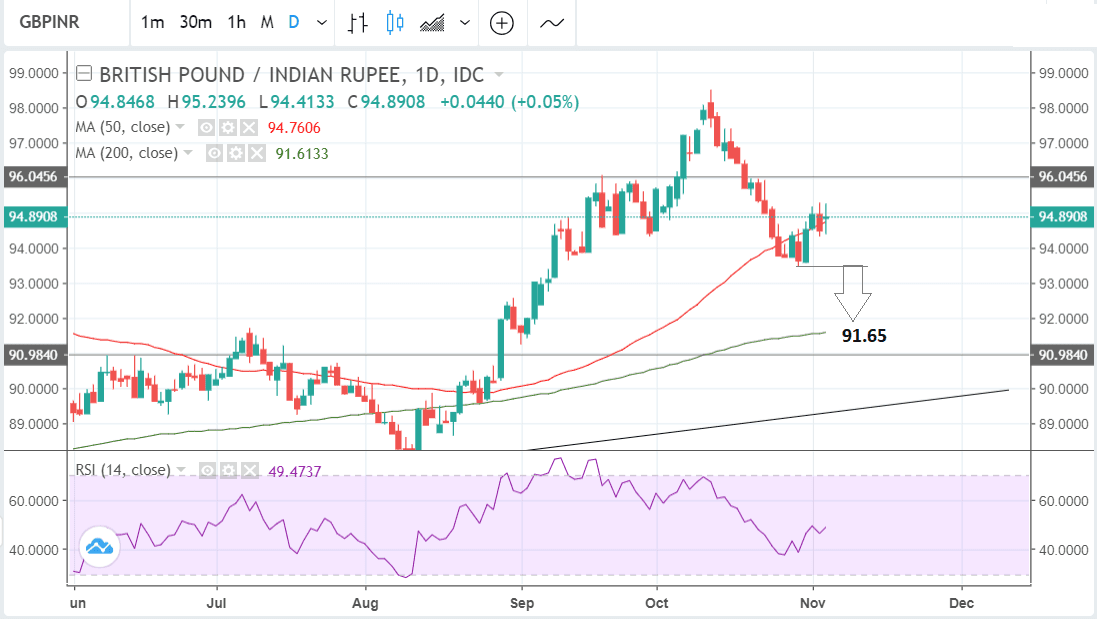

The Pound's trend against India's Rupee remains bearish and we see the short-term downtrend as, on balance, marginally more likely to continue.

The break below 94.00 lows was a critical turning point for GBP/INR, as was the break below the 50-day moving average (MA).

These now suggest the trend in GBP/INR has gone from positive to negative and the exchange rate is therefore pointing lower.

We see more downside as probable, on the condition that the exchange rate can break below the 93.39 lows.

Such a break would probably see an extension down to 91.65 and the 200-day moving average.

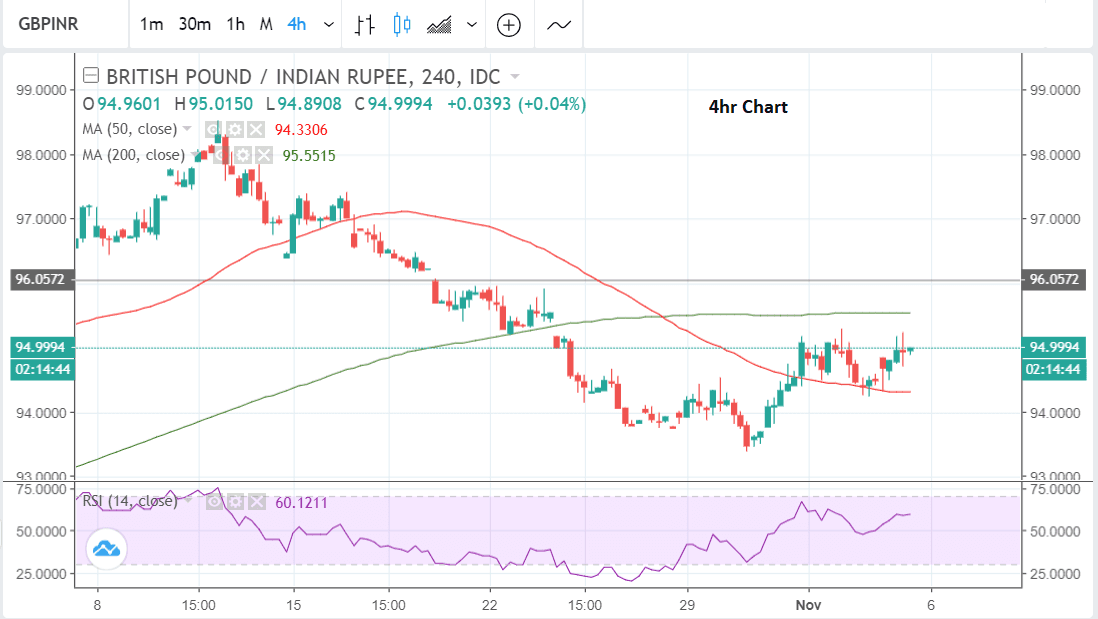

The move below the 94.00 September-October trough lows, as well as the establishment of a sequence of lower highs and lower lows on the four-hour chart are bearish trend-change signals.

The RSI momentum indicator is in the middle of the range, at 49, and providing a neutral reading.

Any upside is likely to be capped at the 96.05 September highs, and we are overall marginally bearish.

There are no key fundamental events on the calendar for the Rupee in the week ahead, and probably the most important data event of the week has already passed on Monday, November 5, when the Nikkei PMI Services survey results for October were released and showed an uptick in sentiment to 52.2 from 50.9.

An acceleration in new orders was one of the main factors behind the rise, according to Markit IHS, the providers of the survey data.

They also noted a continued rise in business cost inflation which is likely to trickle through into broader inflation, a factor which remains relatively high in India.

"Reflective of higher staff costs as well as greater food and fuel prices, service providers’ expenses rose in October," report Markit. "The rate of cost inflation moderated from September’s ten-month high, however, and was below its long-run average."

The rise in costs suggests continued pressure on the Reserve Bank of India (RBI) to raise interest rates after it has already raised them twice in 2018 due to rising inflation.

Higher interest rates tend to strengthen currencies by attracting greater inflows of foreign capital drawn by the promise of higher returns.

Analysts such as Shilan Shah of advisory service Capital Economics expects one more rate hike in the current cycle.

Still, annualised inflation has actually come down to 3.77% in September from a previous high of 5.07% in January 2018 and this could keep the RBI on hold.

The Rupee may be at risk from another source, however, which is political meddling in central bank monetary policy setting, after it emerged the RBI governor Urjit Patel had threatened to resign following a spat with the Modi government over the extent of pressure the RBI is placing on state-owned banks to clean up their balance sheets.

The country has one of the worst rates of bad loans in the world at an average 10.0% and the RBI has tried to increase pressure on banks to clear up their backlog of non-performing loans, however, the government has criticised their policies as growth-threatening.

If the RBI is viewed as compromised there are fears it may lead to a Turkish Lira-style sell-off for the Rupee.

As far as macro factors go, the U.S. midterm elections on Tuesday, November 6 could impact on the Rupee if Republicans lose their control of the house of representatives.

This could lead the Dollar to weaken according to some analysts as it may prevent the government from introducing further tax cuts and stimulus measures.

"Opinion polls show a strong chance that the Democratic Party could win control of the House of Representatives; this could halt President Trump’s plans to push through with implementing tax cuts. If so, the stock market might take a knock, and the Dollar too," says Zaakirah Ismail, FIC Strategist at Standard Bank.

A weaker Dollar would ease pressures on emerging market economies which have struggled in 2018 in the face of the rising Dollar which pushes up the cost of servicing Dollar-denominated debt.

A stronger Dollar meanwhile also pushes up the cost of imports, and for countries such as India which import significant amounts of fuel, this bodes negative for growth.

Therefore, a weaker Dollar could lift the broader Rupee complex, pushing GBP/INR lower in the process.

Advertisement

Bank-beating GBP-INR exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here