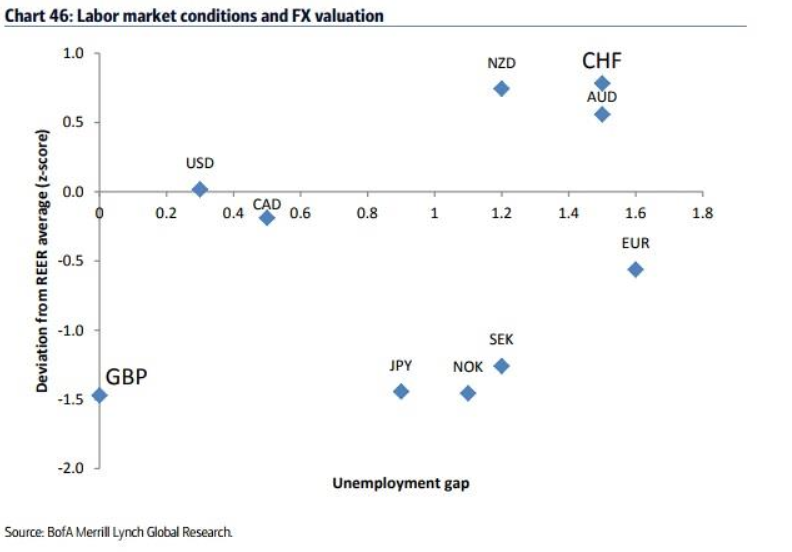

“The UK labor market is the tightest in G10, with the unemployment rate at an all-time low. At the same time, GBP is the most undervalued G10 currency.”

The Pound could rise against the Swiss Franc in 2018, according to strategists at Bank of America Merrill Lynch, who have highlighted an opportunity for speculators to play the developed world’s cheapest currency off against its most expensive.

One of the American bank’s top trades for 2018 is to buy the Pound against the Franc using a complex FX options strategy. The strategy enables clients to profit from an upward swing in the GBPCHF rate while minimising losses if the bet doesn’t work out.

Betting that the Pound strengthens while the Swiss Franc, which is a safe haven currency, falls relative to Sterling will of course be fraught with risk in 2018 and not for the faint of heart.

After all, the year ahead will be a make or break time for the Brexit negotiations and, some argue, the UK economy. Just about the only thing that can probably be taken with some degree of certainty is that Pound Sterling exchange rates will be volatile.

“The UK labor market is the tightest in G10, with the unemployment rate at an all-time low. At the same time, GBP is the most undervalued G10 currency,” says Athanasios Vamvakidis, a foreign exchange strategist at BAML.

“On the other hand, unemployment remains relatively high in Switzerland, while the CHF is overvalued.”

Above: BofA Merrill Lynch graph plotting unemployment alongside exchange rate valuation.

Vamvakidis and the team at Bank of America Merrill Lynch have developed a unique framework that uses the relative strength of labour markets in different countries as a predictor of central bank inflation expectations.

“In ‘Jobs and FX’ we argued that labor market conditions were becoming more important than inflation for FX, as G10 central banks had started ignoring low inflation and were focusing on labor market tightness instead,” Vamvakidis writes.

Inflation expectations, whether they’re informed by actual inflation or by labour market tightness, are key to determining central bank interest rate decisions. Interest rates themselves, are the currency market’s kingmaker.

BAML’s team has combined this labour market insight with analysis of the “real effective exchange rates” of relevant countries to assess whose is the most overvalued, fairly valued and undervalued. From these insights, the strategists have crafted a series of 2018 trading ideas.

“This simple approach avoided the difficult discussion of estimating the natural rate of unemployment,” Vamvakidis adds.

For the purposes of the investment idea, it helps that Bank of America Merrill Lynch has an outright negative view of the Swiss Franc as a standalone currency for 2018.

“CHF has fallen precipitously through the summer months with EUR/CHF now standing less than 5% below the previous SNB floor of 1.20,” writes Kamal Sharma, a colleague of Vamvakidis, in a recent note.

“Our analysis of the Swiss balance of payments data suggests the pressure on CHF is likely to continue over the medium term as foreign investors continue to sell Swiss domestic assets.”

Above: GBP/CHF rate at weekly intervals. Captures 2015 SNB De-pegging and Brexit vote reaction.

Meanwhile, the extreme sell off seen in 2016 and 2017 has left the Pound undervalued on a fundamental basis and prone to a sudden relief rally should Brexit negotiations progress better than the market has been willing to give credit for.

“The lack of progress in the Brexit negotiations so far suggests a volatile outlook for GBP ahead, even if the final outcome is positive. However, this also suggests sizable potential gains if investors get the final outcome right,” Vamvakidis writes.

“It is all about the Brexit transition, in our view... A transition deal will effectively “kick the can down the road,” postponing a number of risks and uncertainties for at least two years, and will therefore be bullish for GBP.”

Instability within the British government and the declining popularity of Prime Minister Theresa May are both risks to the BAML trade thesis as they have the potential to result in another general election.

As a minimum, another election would disrupt the Brexit negotiations, heightening the risk of a “no deal Brexit” where the UK and the EU default to trading with each other on WTO terms. Another election also risks installing another Labour Party government in Downing Street.

“Such risks justify an option structure for the trade, assuming a positive eventual outcome,” says Vamvakidis.

Vamvakidis idea is to buy a 6 month “1.40/1.45 GBPCHF call spread”. This trade will profit if the Pound-to-Franc rate rises above 1.40 but will limit losses to the cost of purchasing the options. It is a complex derivatives strategy that is intended for use by professionals, not retail investors.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.