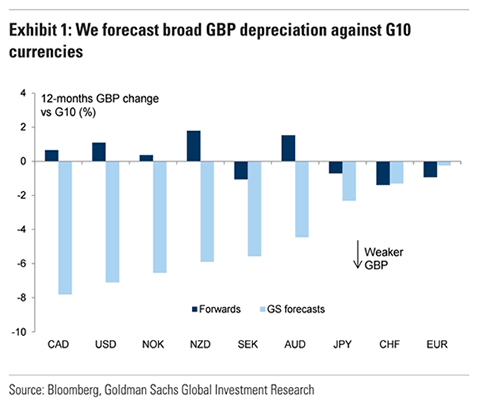

Pound Sterling is still going to end 2017 lower against the Euro and Dollar than current levels say analysts at Goldman Sachs.

However, the GBP/USD is looking the most at risk of a sizeable decline with analysts at the Wall Street giant saying they “continue to hold a bearish view on GBP, particularly against the USD.”

The call comes following what has been a relatively good week for the UK currency which has breached the 1.30 level against the US Dollar in a move that potentially frustrates Goldman's stance.

Less frustrating will be the Pound to Euro exchange rate’s apparent unwillingness to slip below a floor at 1.1287 as analysts at the bank believe GBP/EUR will muddle along at around current valuations over coming months.

Sticking with a Negative View on Sterling

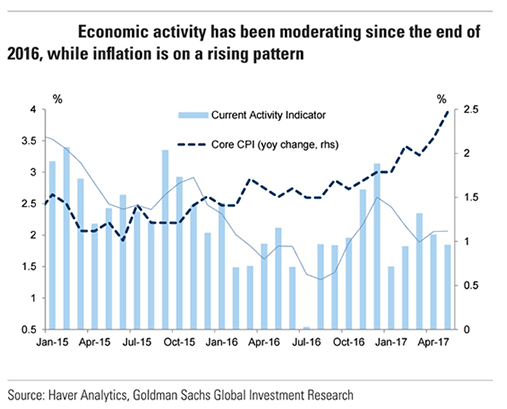

"The market seems to be taking the opposite view to ours that activity matters less than inflation in monetary policy decisions," says analyst Silvia Ardagna at Goldman Sachs’ London office. "Perhaps this is because activity is decelerating from a high level and growth remains above trend, while inflation is above the policy target."

But the market will ultimately be proven wrong argues Ardagna, her negative view on the outlook is based on "below consensus UK growth and a less hawkish monetary policy stance than the market anticipates."

And then there is Brexit and the state of the UK Government; “we think Brexit uncertainties will not be resolved quickly with a weaker Government.”

But, herein lies a risk to Goldman Sachs’s negative stance on Sterling, “the major risk to our view is news that makes the UK remaining in the Single Market via a “Norway” type of deal more likely.”

The securing of a transitional deal to soften the exit process will also likely support Sterling says Ardagna ensuring the currency defies Goldman's negative forecasts.

Goldman Sachs forecast GBP/USD to fall to 1.20 in twelve months.

While Sterling is seen falling against all the major G10 currencies, as can see though, weakness against the Euro is less pronounced:

“We forecast EUR/GBP to trail around current levels at 0.88,” says Ardagna. This is a Pound to Euro rate of 1.1364.

Consensus forecasts by 45 investment banks and brokers sees GBP/EUR at 1.15 at the turn of the year and at 1.15 for the duration of 2018.

Consensus sees GBP/USD at 1.26 at the turn of the year and at 1.32 for much of 2018.

Current Account Deficit Grows, Spells for Pound Weakness

When it comes to the Pound - keep the current account in mind - it is arguably the single most important economic concept when it comes to determining currency value.

This is the country’s bank balance with the rest of the world and the currency’s fundamental long-term valuation depends on a combination of how much we import, export and how much foreign capital the country attracts.

Unfortunately for Sterling, the current account has been in deficit for many years now as the UK imports more than it exports, leaving it reliant on foreign investment inflows to keep the Pound propped up.

The reason the Pound is so vulnerable to Brexit is because a bad outcome could hit our exports or stop foreign investor inflows from shoring up the account.

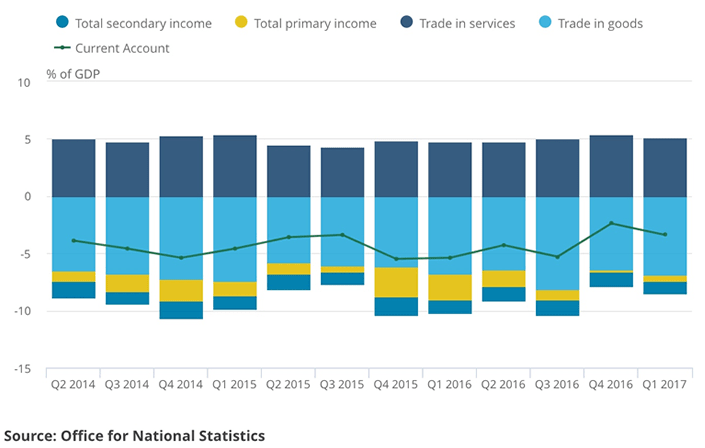

There had been some improvement in the current account towards the end of 2016; however latest data from the ONS has confirmed the improvement has stalled.

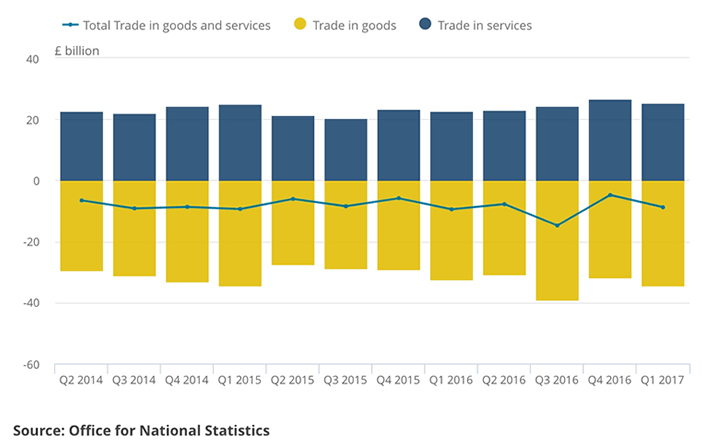

While the UK is an exporter of services the country remains hampered by an inability to export goods, particularly to Europe.

“The total trade deficit widened to £8.8 billion in Quarter 1 2017 following a sharp narrowing of the deficit in Quarter 4 2016 (£4.8 billion); this was due to a widening in the deficit on trade in goods and a narrowing in the surplus on trade in services,” report the ONS.

A current account deficit of £22.2 billion was recorded with the EU in Quarter 1 2017 whilst a surplus of £5.3 billion was recorded with non-EU countries.

In terms of the Brexit debate this point is irrefutable - the European Union gains a great deal more value from the UK than does the UK benefit from the EU.

Looking ahead, there are however signs that the UK’s trading position might improve.

“The latest monthly trade data and surveys of export orders suggest that net trade will start contributing positively to GDP growth in the coming quarters,” says Scott Bowman, UK Economist at Capital Economics.

As can be seen, the UK’s reliance on foreign goods is as sizeable as ever.

There were hopes that the fall in value of Pound Sterling would go some way in boosting exports and reducing imports.

Analysts at Goldman Sachs believe the size of the fall in Sterling must be far greater than that already experienced for this to come about.

Goldman Sachs research shows a decline in Sterling of between 20% and 40% from pre-Brexit levels was needed to bring the current account deficit back to sustainable levels.

This is a huge adjustment that would surely push inflation to levels that would shatter economic growth.

“At the end of Q4, balance of payments data showed a sizeable improvement in the UK current account which would imply that the correction towards a sustainable current account has already happened, but we highlighted that it is still too soon to assume this improvement will prove persistent,” says Ardagna.

It looks as though the current account deficit is going to a millstone around Sterling’s neck for a while longer.