The CBI has reported that Britain’s SMEs are expecting to boost exports over coming quarters as the UK becomes more competitive thanks to a devaluation in the overvalued Pound Sterling.

A survey of UK SMEs, conducted by the CBI, shows that they are expecting a pick up in exports over coming quarters.

No doubt, the shift in fortunes will certainly have the decline in the value of Sterling to thank.

The Pound has devalued in the region of 10% since Brexit - a welcome boost to UK exporters who have struggled under the weight of an over-priced currency for years now.

While most believe a stronger currency to be a good thing, it certainly is not for a good chunk of the UK economy.

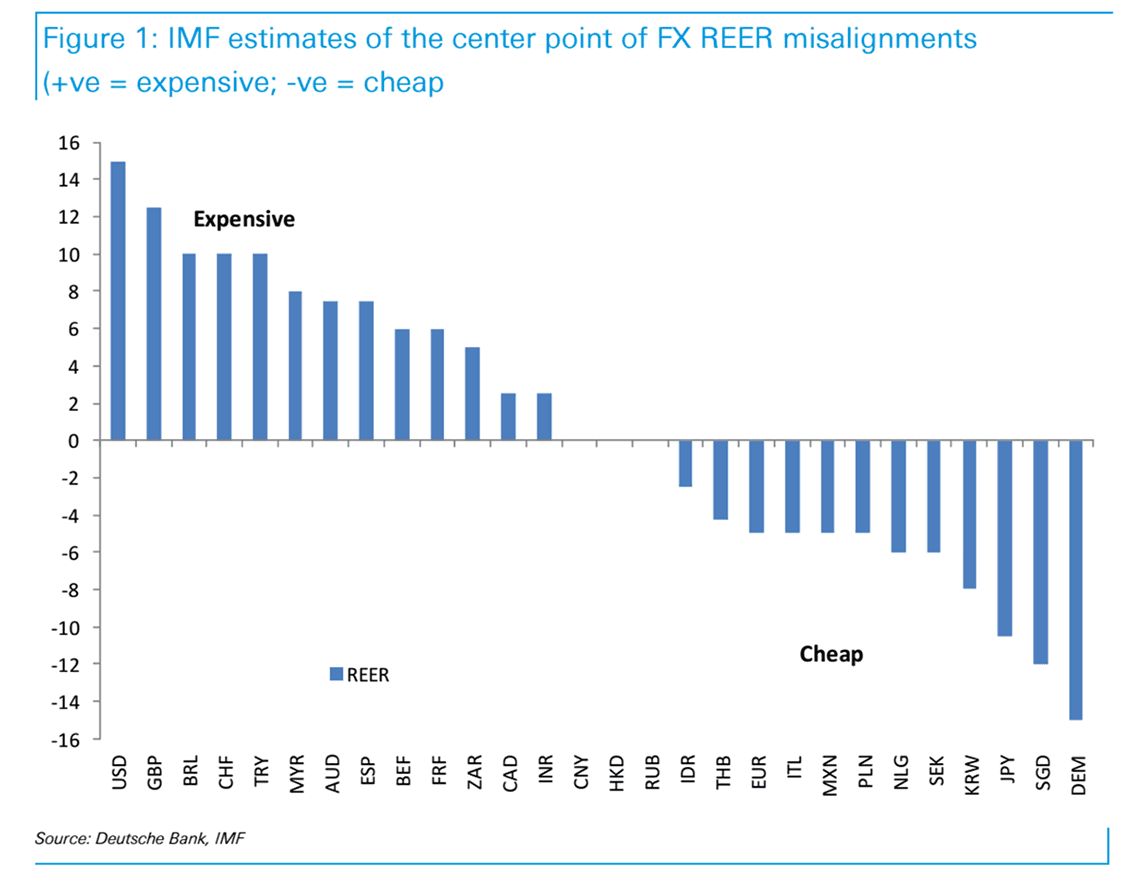

The UK currency was deemed overvalued ahead of the EU referendum with the latest IMF External Sector Report showing the UK’s Real Effective Exchange Rate (REER) as being amongst the most expensive in the world.

In fact, the data, which covers the period leading into the EU referendum, showed only the US Dollar could be considered overvalued to a greater extent.

REER is the nominal effective exchange rate (a measure of the value of a currency against a weighted average of several foreign currencies) divided by a price deflator or index of costs.

“An increase in REER implies that exports become more expensive and imports become cheaper; therefore, an increase indicates a loss in trade competitiveness,” notes the IMF.

Look how overpriced the Pound was in REER terms:

We already know the UK economy is suffering a mismatch in terms of global competitiveness with the country importing far more than it exports.

The country’s Current Account deficit is running at record highs - the Current Account is best thought of as the country’s bank balance with the rest of the world.

When we import more than we export the account tends to go into negative as we become a net debtor to our trading partners.

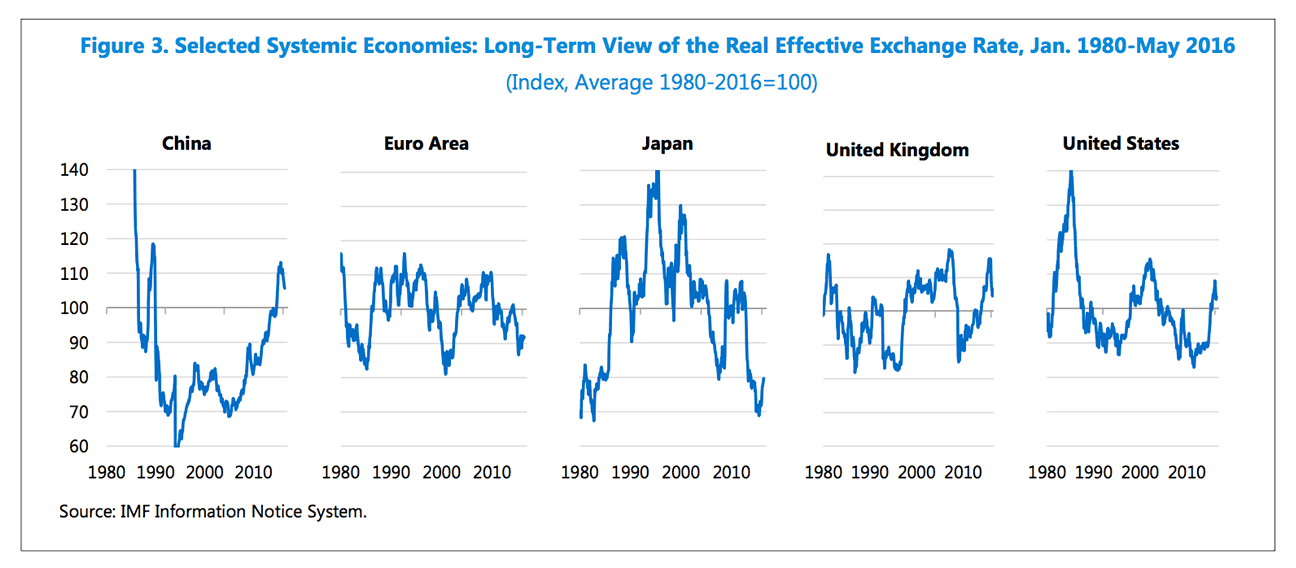

The overpriced Pound is also reflected in the following long-term graphics:

As can be seen, the currency has ample space within which to come back down towards longer-term averages; this should help increase the UK’s export competitiveness with the rest of the world.

And this could well be happening, thanks to Brexit.

“Optimism about export prospects for the year ahead rose slightly, with SMEs reporting the first improvement in competitiveness in EU and non-EU markets since 2013,” notes the CBI in their latest Quarterly Trends publication.

Although the volume of export orders fell again on the previous quarter – SMEs anticipate that they will rise in the coming quarter, after no increase since April 2014.

However, it is not all plain sailing as a pick up in UK exports also depends on the health of our export markets.

“The proportion of firms reporting political or economic conditions abroad as a factor likely to limit export orders over the next quarter climbed to a record high,” note the CBI.

However, we continue to expect the global economy to tick over in positive fashion over coming months, largely supported by global central bank stimulus.

This should surely allow UK exporters to take advantage of the gift that is a weaker domestic currency.

A Weaker Euro Works for Germany and the Eurozone Periphery

If one needs an example of how a weaker currency aids an economy then look no further than the Eurozone.

Following the bout of aggressive ECB policy easing over recent years the Euro’s REER has fallen dramatically.

At the same time the Eurozone boasts a strong Current Account surplus - lead largely by German exports.

“The EUR is less exciting in aggregate (about 5% undervalued) but for Germany the EUR is assessed to be 15% cheap, while for France and Spain the EUR is assessed to be 6% and 7.5% too expensive respectively. This will add pressure for a German fiscal stimulus to realign savings relative to investment,” says Alan Ruskin, a currency analyst with Deutsche Bank.

However, now even peripheral Eurozone countries have the Euro to thank for their recoveries.

The IMF notes that external positions of systemic countries in the euro area have improved markedly since the global financial crisis.

This process of external adjustment has been particularly visible in countries with large external deficits, which have witnessed steep improvements in their current accounts—all of which have reached or are near positive territory by now.

“Most noticeable adjustments have taken place in Greece and Portugal, (10-11 percentage points of GDP since 2010) followed by Italy and Spain (5-6 ppts),” report the IMF.

The adjustment is explained by the IMF to be owed to a marked contraction in domestic demand, supported by the real depreciation of the euro (10 percent during 2010-15) resulting from relatively weak cyclical position easy monetary policy in the euro area.

Can the UK economy now expect a fundamental improvement from a balancing in economic activity?

It depends on how long the GPB stays at competitive values.