- GBP selloff extends on PMI disappointment

- PMI signals economic contraction in Sept.

- But inflation is falling rapidly

- Justifying Bank of England's decision to hold rates

- Good news seen in latest consumer confidence data

Image © Adobe Images

The British Pound extended a multi-week decline after survey data revealed the UK economy saw a marked slowdown in September that exceeds anything seen since the Covid lockdown period.

The S&P Global Composite PMI fell to 46.8 from 48.6 in August, undershooting consensus expectations for 48.7.

A reading below 50 signals contraction and the findings are therefore consistent with an economy that has gone into reverse.

The headline figure was hinted at in the minutes from this week's Bank of England Monetary Policy Committee meeting and appears to have helped swing the MPC into voting to keep interest rates unchanged at 5.25%.

"With the Bank of England having had sight of the survey data prior to its latest policy decision, the worrying signals from the survey of heightened recession risk and cooling inflationary pressures are likely to have added to calls to halt rate hikes," says Chris Williamson, Chief Business Economist at S&P Global Market Intelligence.

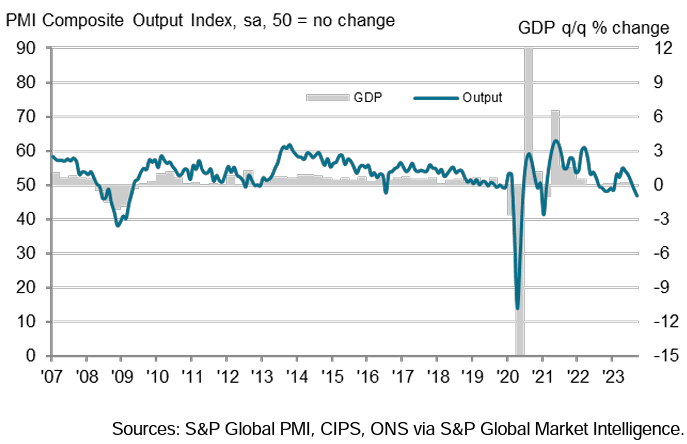

Above: PMI data signals economic contraction is likely to be revealed by incoming official data.

Looking at the components of the report reveals services - the largest sector of the economy - contracted with the PMI recorded at 47.2, below expectations for 49.2 and down on August's 49.5.

Manufacturing remains mired in contraction at 44.2, but this was a shade higher than August's, and the consensus expectation, reading of 43.

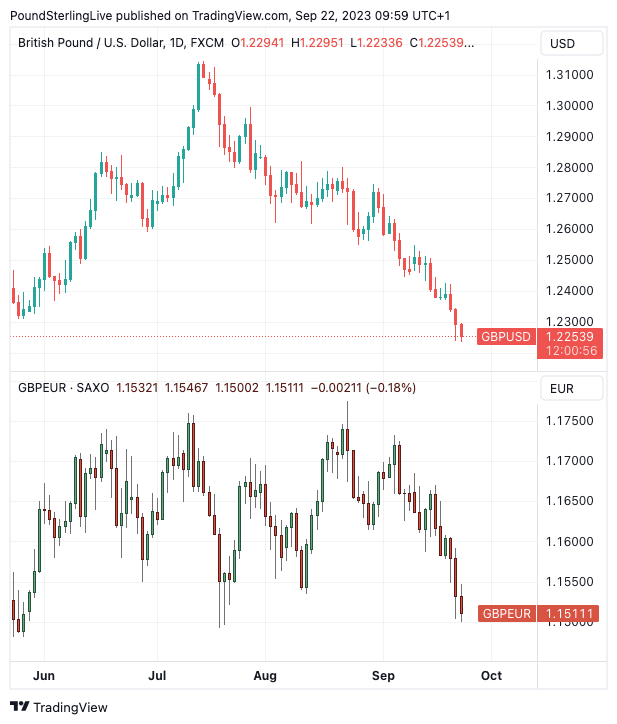

Following the data, the Pound to Dollar exchange rate (GBPUSD) was quoted at 1.2246, down 0.40% on the day, and the Pound to Euro exchange rate (GBPEUR) rate was at 1.1511, down 0.18% on the day. These losses build on the sizeable declines that followed Thursday's Bank of England decision.

"It’s another dismal outcome," says James Smith, Developed Markets Economist at ING, of the data. "The Bank will remain on hold in November and that August’s rate hike marked the top in this tightening cycle."

Further losses are likely for Pound Sterling as markets bet the UK is headed for recession and that the Bank of England will be swift in cutting rates, potentially as early as May 2024, despite expectations for inflation to remain at elevated levels.

By selling the Pound against the Euro and Dollar markets are saying the UK's economic outlook is worse than that of the Eurozone and the U.S. and that the Bank of England will cut harder and faster than the European Central Bank and U.S. Federal Reserve.

S&P Global said September data pointed to a reduction in UK private sector output for the second month running. Moreover, the rate of decline accelerated to its fastest since January 2021.

To put the decline in perspective, the fall in activity between August and September represents the fastest reduction in output since the lockdown period in January 2021.

Above: GBPUSD (top) and GBPEUR shown at daily intervals.

Having seen the data ahead of Thursday's Bank of England decision, policymakers will have noted inflationary pressures are cooling markedly. Input price inflation saw its largest monthly fall so far in 2023, despite widespread reports citing pressure on costs from higher fuel bills.

A combination of weak demand and lower cost inflation contributed to the slowest increase in average prices charged by private sector companies since February 2021.

The Bank said on Thursday it expects inflation in the UK to fall sharply over the coming months.

The Bank will have also taken note of the PMI survey reporting an abrupt turnaround in private sector employment numbers, thereby ending a five-month period of growth.

"Aside from the pandemic lockdown months, the rate of job shedding was the fastest since October 2009. Solid declines in staffing levels were seen in both the manufacturing and service sectors, with the respective index for the latter posting in negative territory for the first time in 2023 to date," said S&P Global.

The UK economy is slowing, inflation is coming down, jobs are being cut and this should prompt wages to fall over the coming months.

Some Good News

There was some good news out Friday with reports that UK consumer confidence reached a 20-month high as the latest GfK consumer confidence survey surprisingly improved by 5 points to read at -21 in September.

The improvement nevertheless matters for the UK economic outlook given the UK's is primarily a consumer-driven economy.

GfK says improvement comes amidst a backdrop of falling core inflation, higher interest rates and rising average weekly earnings, although challenges still remain. But he adds that the survey shows individuals are confident their personal financial situation for the coming year will improve.

The Personal Financial Situation for the next 12 months measure is heading back towards positive territory, a metric GfK says is key to indicating the future financial position of households.

"This renewed optimism can also be seen in the similar turnaround for our view on the general economic outlook for the next 12 months, and the eight-point advance in major purchase intentions is potentially better news for retailers as we move into autumn," he adds.

Gabriella Dickens, Senior UK Economist at Pantheon Macroeconomics says the consumer outlook will likely improve over the rest of the year, supported by further growth in real wages, as the pace of price rises continues to slow.

Pantheon's calculations show mortgage refinancing looks set to subtract about 0.2 percentage points from quarter-on-quarter growth in households' disposable income in Q3 and Q4, which is an unhelpful but not decisive headwind.

"On balance, then, real household disposable incomes should be around 2.0% higher in Q4 than a year ago," says Dickens.