- Partial shutdown beckons for the UK

- Sentiment shored up by extra fiscal support

- Growth to take ~2.0% hit

- GBP is amongst worst performers

- Comes amidst hostile global market backdrop

Above: Prime Minister Boris Johnson gives a televised briefing on the UK Covid situation. Image: Simon Dawson / No 10 Downing Street.

The British Pound is recovering recent losses against the Euro, Dollar and other major currencies amidst a recovery in global investor sentiment and a move by the UK government to provide additional fiscal support for under-pressure businesses in the hospitality sector.

The Pound was amongst the largest losers on Monday on suggestions the government might tighten restrictions at month-end to contain the spread of Omicron, but Chancellor Rishi Sunak on Tuesday announced additional money would be made available to support the hospitality sector.

£683M of new money was made available to businesses in hospitality and leisure, with a business able to apply for a maximum of £6K for each of its premises.

Fiscal support is critical in limiting any long-term damage to businesses and is on net a sentiment boost for the Pound.

"The Chancellor has provided welcome breathing space to boost confidence and provide support for hospitality and leisure businesses to keep their doors open through tough disruption to their crucial winter trading," said Rain Newton-Smith, CBI Chief Economist.

- Reference rates at publication:

GBP to EUR: 1.1756 \ GBP to USD: 1.3254 - High street bank rates (indicative): 1.1530 \ 1.2983

- Payment specialist rates (indicative: 1.1670 \ 1.3188

- Find out more about specialist rates, here

- Set up an exchange rate alert, here

Sterling could yet be amongst the major losers in the approach to Christmas as media reports swirl that the UK hospitality industry could be effectively shuttered from December 28 onwards, while curbs on household mixing will also be introduced.

The plans for a "circuit breaker" that would be put in place after Christmas would resemble 'stage 2' restrictions from the previous winter's lockdown.

Closures would impact an economy already suffering the effects of surging inflation, spent fiscal support from government and the prospect of higher interest rates at the Bank of England.

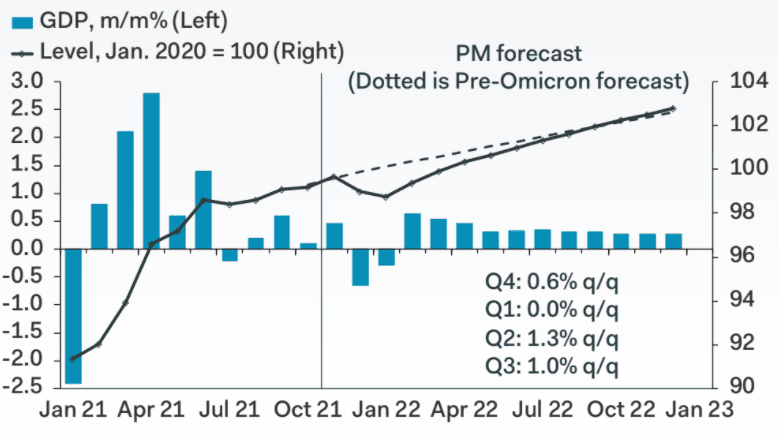

Modelling from independent research firm Pantheon Macroeconomics anticipates a 2% hit to GDP from any return to 'stage 2' rules.

A full lockdown would meanwhile deal a 6% blow to growth. But their modelling assumes that Covid-19 cases will fall back in the second half of January, giving people confidence to venture back to consumer services venues in February.

Their base-case looks for a 0.6% month-to-month rise in GDP in February and a 0.5% increase in March. GDP in the first quarter will be largely unchanged from the fourth quarter.

Above: "Our base case: No major new restrictions, but consumer caution" - Pantheon Macroeconomics.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Although the Eurozone economy also faces various forms of additional restrictions, the UK economy is uniquely exposed given the dominance of the services sector to the economy making Sterling particularly vulnerable.

With services accounting for over 80% of UK economic activity the impact of restrictions will always tend to be more severe for the UK economy which suffered the largest contraction amongst peers in the first stage of the Covid pandemic.

Plans are said to potentially involve a ban on people from different households mixing indoors and restrictions on hospitality, according to numerous media outlets.

The Times reports December 28 has been pencilled in by officials as a possible starting point for new curbs.

The Telegraph says Parliament is likely to be recalled on December 28 to discuss measures that could include restrictions on pubs and restaurants, return of bubbles for households and social distancing.

Prime Minister Boris Johnson did however bypass the imposition of any additional restrictions at a Monday Covid briefing, saying he was monitoring the data "hour by hour".

The Times said a two-week circuit breaker banning indoor mixing was indeed discussed at a Cabinet meeting held ahead of the briefing.

Heading into the news the Pound had already lost ground against the majority of its G10 peers with the largest losses coming against the safe haven Yen and Franc as a cocktail of sour domestic news and cold global market sentiment was stirred.

"The GBP is among the currencies that are particularly sensitive to spikes in risk aversion," says Valentin Marinov, Head of G10 FX Strategy at Crédit Agricole.

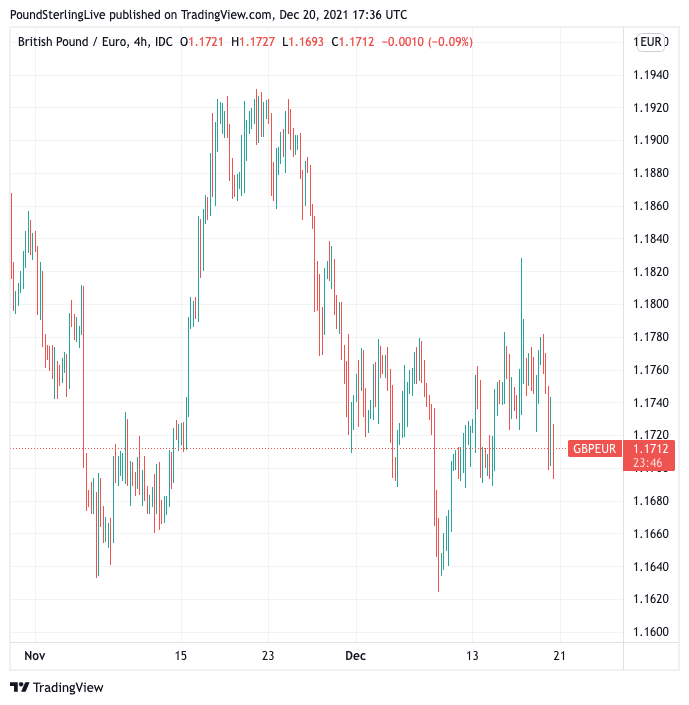

Above: GBP/EUR since November.

In a 'risk off' market the Pound would be expected to register healthy advances against the Australian Dollar, but losses in GBP/AUD testify to the domestic and idiosyncratic risks facing the UK currency in addition to global factors.

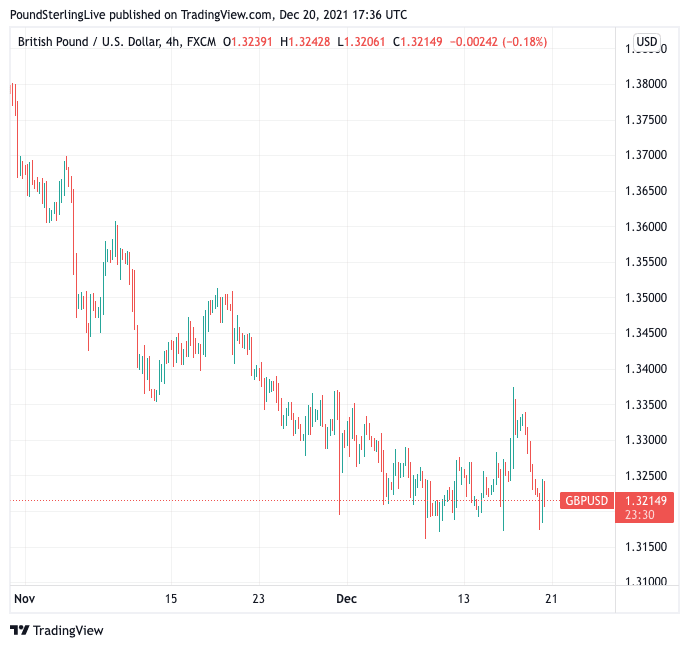

The Pound to Euro exchange rate fell half a percent to quote at 1.1700 on the developments while the Pound to Dollar exchange rate was down at 1.3215.

At the very least, the odds of a recovery by the Pound against the Euro, Dollar and 'safe-havens' into year-end would require the global market to find its feet again and confidence to return.

"The clock is ticking down towards Christmas but there’s still no sign of a Santa rally," says Chris Beauchamp, Chief Market Analyst at IG. "The macro backdrop isn’t particularly appealing, thanks to the rising numbers of Omicron cases that threatens to bring back tighter restrictions in both the UK and the US."

Above: GBP/USD since November.

Analysis from Capital Economics - an independent research provider - finds that if worries about the spread of Omicron abated, stock markets would probably recover some of the ground they’ve lost recently.

"Nonetheless, we wouldn’t expect that to mark the beginning of another big rally," cautions Thomas Mathews, Markets Economist at Capital Economics.

In a note to clients Mathews observes the situation between now and last year is not that different in that the global economy was facing another wave of Covid.

But the stock market has reacted differently: this year it is losing value while in 2020 it was rallying.

"Equities had been boosted last year by the prospect of highly effective vaccines, which seemed to mean that the longterm economic damage from the virus wave would be limited. This year, the prospect of a potentially vaccine-resistant variant seems to have given that optimistic view a harsh reality check," says Mathews.

He also notes sentiment is materially different given that at the end of 2020 governments and central banks were proving generous with fiscal and monetary support.

But faced with high inflation this generosity will unlikely be repeated.

Capital Economics anticipates some recovery potential once Covid fears subside, but for the given reasons a material rally is unlikely.

"We expect fairly underwhelming returns from equities over the next couple of years," says Mathews.