- GBP softer in wake of Bank of England announcement

- Bank says economy has turned a corner

- But is worried about outlook for employment

- Economists say more QE inevitable

Image © Adobe Stock

The Bank of England increased the scale of its quantitative easing programme by £100BN it announced on June 18, taking the programme's total to £745BN.

The increase comes in line with market expectations and therefore did not come as a shock to the Sterling exchange rate complex, as any larger or smaller amount would have come as a surprise and moved the market. However, expectations are elevated that further action will be announced by the Bank over coming months and this should keep the Pound under pressure.

The Bank voted unanimously to keep interest rates unchanged at 0.1%, suggesting there is little appetite amongst the Monetary Policy Committee to cut rates to 0% and below, which is on balance supportive of Sterling. Any message that negative interest rates (NIRP) were possible over coming months would have likely sunk the currency.

In the wake of the event, Sterling is seen losing ground with the Pound-to-Euro exchange rate quoted at 1.1125, the day's low is at 1.1092. The Pound-to-Dollar exchange rate is quoted at 1.2502, the day's low is at 1.2475.

"Given the immediate market reaction it appears investors were hoping for a little more than the £100bn increase in quantitative easing that has been announced by the Bank of England. Indeed they may have a point in being disappointed by this announcement given the Federal Reserve and European Central Bank are both guiding the market that they will do whatever it takes to keep the economy afloat," says Hinesh Patel, portfolio manager at Quilter Investors.

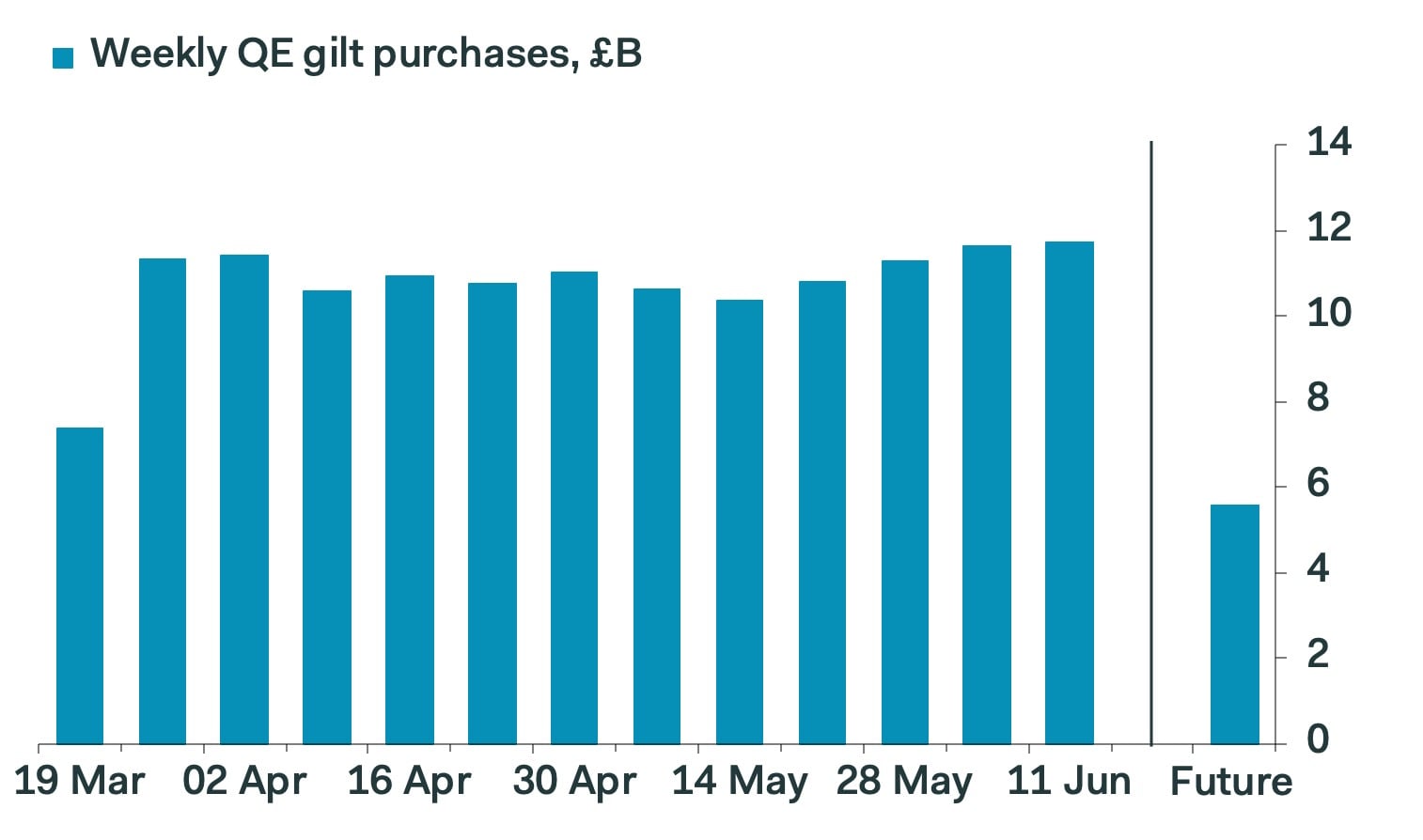

The Bank had bought £150BN worth of UK government bonds (gilts) out of a potential £200BN by June 10. This works out at a spend of around £11.5BN per week plus, excluding the fraction of £10BN in corporate bonds.

The Bank said today that the additional increase is enough to go until year-end, which implies reduction to about £6.6BN per week.

Image courtesy of Pantheon Macroeconomics

Justifying the decision to opt for a £100BN boost to quantitative easing (QE) - and not a greater amount as some analysts had expected - the Bank communicated that it saw signs that the worst of the covid-19 slump might have already passed.

"There are signs of consumer spending and services output picking up, following the easing of Covid-related restrictions on economic activity. Recent additional announcements of easier monetary and fiscal policy will help to support the recovery," said the Bank in a statement.

In what can be taken as a relatively optimistic stance, the Bank noted that the economic decline in the second quarter was potentially less severe than earlier anticipated. The view echoes that of BoE member Andy Haldane who said in late-May that the need for negative interest rates had become less likely based on evidicence that the economy was turning around.

In fact, Haldane was the only member of the MPC to vote against raising QE at this week's policy event, arguing:

"The recovery in demand and output was occurring sooner and materially faster than had been expected at the time of the previous MPC meeting. If this persisted, cumulative output losses over the policy horizon could plausibly have halved compared with what had been expected at the time of the May Report, boosting inflation prospects in the medium term. There were still material downside risks, especially around employment, but these risks were more evenly balanced than in May. Existing monetary conditions were extremely accommodative and, in the view of this member, supporting a strong recovery sufficient to return inflation to its target."

We find this glass 'half full' view on the economic outlook to be on balance positive for Sterling as investors maintain a view that negative interest rates and larger increases to the QE programme are broadly negative for the currency.

Bank of England's £100bn QE to year-end means that weekly gilt purchases will slow down to around 40% of current pace. A relatively hawkish move compared to other central banks. Obviously BoE can front-load these purchases but $GBP higher as on a not so aggressive BoE QE move pic.twitter.com/44j6ZrzkZH

— Viraj Patel (@VPatelFX) June 18, 2020

However, some economists remain of the view that the June top-up to the QE programme will be followed by further moves in subsequent months.

"We expect £300 billion more to be added to APF over the next 18 months – likely £100 billion in June, November and May 2021. However, to support inflation back to target, as quantitative easing becomes less effective with higher savings and reduced issuance, we expect the MPC to do more, likely signalled in August and implemented in November: cut Bank Rate to 0% (ZIRP) and provide bank funding at a negative rate (NIRP). In our bear case, we expect Bank Rate to go to -50bp in 2021," says Jacob Nell, Head of European Economics at Morgan Stanley.

While the Bank noted growth in the economy might have turned a corner in April, they do signal concern as to the direction of the labour market which would potentially pave the way for further action on QE.

"More timely indications from the claimant count, HMRC payrolls data and job vacancies suggest that the labour market has weakened materially. Following stronger than expected take-up of the Coronavirus Job Retention Scheme, a greater number of workers are likely to be furloughed in the second quarter," said the Bank. "Evidence from business surveys and the Bank’s Agents is consistent with a weak outlook for employment in coming quarters. Some households are also worried about their job security."

"Should things go even worse from here, they have left themselves enough bond purchasing capacity in the future to continue soothing markets and the economy as best they can," says Patel.

"We doubt that this is the last QE extension. Unemployment looks set to rise sharply in the second half of this year and to fall back slowly thereafter. The resulting prolonged weakness in domestically-generated inflation likely will necessitate the MPC doing more to stimulate the economy in the winter. We look for a further QE extension of £50B in November, but for the Committee to hold back from cutting Bank Rate below zero, due to the questionable benefits of such a step," says Samuel Tombs, UK Economist at Pantheon Macroeconomics.

The Bank's expectations for inflation also offers further evidence that further QE is possible as CPI inflation is expected to fall further in coming quarters, largely reflecting the weakness of demand. Inflation was reported at 0.50% year-on-year in May and some economists are forecasting a fall to 0% before year-end.

With further rounds of QE likely in the future it is therefore little wonder the Pound has not leapt in relief.

The QE programme sees the Bank effectively print money to buy government debt, which there is now a lot more of thanks to the coronacrisis. This debt is issued in the form of bonds - or gilts - that pay the investor a yield for the duration of its lifetime.

But, the greater the demand for these bonds then the lower the yield paid on them. This is where the Bank of England comes in: by creating significant demand for these bonds via QE their yield has fallen, with the yields of some bonds actually falling into negative territory for the first time ever in May.

The yield has long attracted significant volumes of foreign investor capital, but with yields so low that attraction is waning. This has implications for the Pound as that foreign investor demand for bonds has been a source of support; remove that support and the Pound looks exposed.

Therefore, the greater the scale of QE at the Bank of England, the lower bond yields will likely be and the less demand there is for Sterling.

"Our view that inflation will still be closer to 1.0% by the end of 2022 than the Bank’s 2.0% target, suggests more QE will be needed eventually," says Thomas Pugh, UK Economist at Capital Economics.