- GBP buoyant against Dollar

- Nursing wounds against EUR

- Bank of England could cut rates 50 basis points

- Tipped to restart quantitative easing

Image © Bank of England

The Bank of England will surprise markets and deliver a sizeable cut to interest rates in March and restart quantitative easing in April, as part of a global effort to shore up economic activity and investor sentiment in the face of a coronavirus-linked economic slowdown.

This is the view of Bill Diviney, Senior Economist for the U.S. and UK at ABN AMRO, who says the Bank of England will cut interest rates by a sizeable 50 basis points, taking the basic lending rate to 0.25%.

The foreign exchange rule book suggests that when a central bank cuts interest rates - particularly when the cut and the scale of the cut are a surprise - the currency it issues declines in value.

Those watching the Pound should also be aware of the timing of any Bank of England action: the next meeting is scheduled for March 26, but there is growing speculation that the Bank could act as soon as Wednesday, in tandem with the announcement of the government's budget.

Such a move would fulfil incoming Governor Andrew Bailey's testimony to the Treasury Select Committee that a coordinated approach by Government and the Bank of England was required to fight the slowdown inspired by the coronavirus outbreak.

"The Chancellor looks set to unveil measures to help firms affected by the coronavirus outbreak in Wednesday's budget, but markets will be more interested in any coordinated Bank of England action," says James Smith, Developed Markets Economist at ING Bank.

However, because the economic impact of coronavirus is expected to be to the supply side (i.e. a shortage of components for manufacturing) and to sentiment (falls in consumer spending) there is an agreement amongst economists that it is in fact the government who is best placed to assist the economy. This can come in the form of special loans to business, increased sick pay, debt holiday's etc.

Therefore, any Bank of England action on Wednesday would more likely be assistance to government programmes, not necessarily a rate cut. "BoE officials will also be acutely aware that a rate cut – lowering debt-service costs - is likely to be a less effective demand boost that it normally would, and is unlikely to mitigate the wider cashflow issues facing affected firms as effectively as some fiscal measures," says Smith.

But of course a mid-week rate cut cannot be discounted.

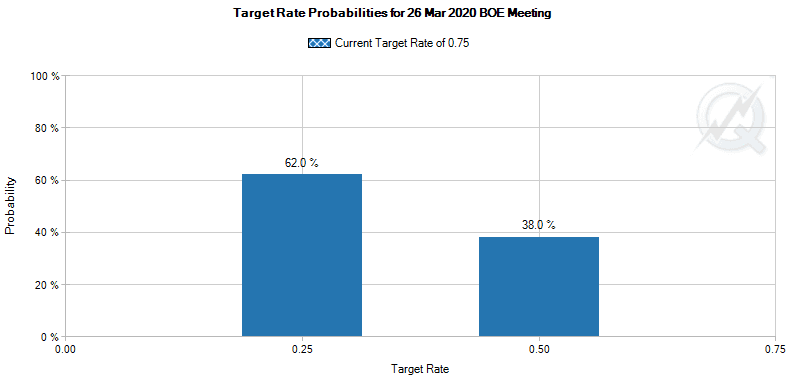

Above: The odds of a 50 basis point rate cut being delivered by end-March, according to CME.

The scale of the Bank's intervention in the market won't just rest with an interest rate cuts says ABN AMRO's Diviney who tips the Bank to restart quantitative easing the following month, the process whereby it prints money to purchase bonds.

"For similar reasons to our Fed call change, we also now expect more aggressive easing from the Bank of England to counter the coronavirus fallout. At the MPC meeting on 26 March, we expect the Committee to cut by 50bp; previously, we expected a 25bp cut. This would take Bank Rate to 0.25%, and given the BoE’s similar scepticism over negative rates, we expect the next move in April to be a restart of quantitative easing," says Diviney.

In contrast to previous rounds of quantitative easing, ABN AMRO expects this to be announced as open-ended at GBP20bn per month rather than a stock announcement.

"This should give the BoE the flexibility to provide accommodation and potentially bring it to an early halt once activity looks to be normalising. Alternatively, if there is a prolonged hit to activity, asset purchases could continue for longer," says Diviney.

Lowering Forecasts for the Pound

ABN AMRO have meanwhile told clients they are cutting their forecasts for the Pound amidst expectations for aggressive monetary easing and the unwinding of 'long' bets on the currency being held by the market.

"Investors will probably further close their net positions in currencies," says Georgette Boele, Senior FX Strategist at ABN AMRO. "We think that they are still net-long Dollar and Sterling and net-short Euro and Yen.

Being 'long' a currency means the net position of bets in the markets are for rises in a currency. When the facts on the ground change and investors are forced to unwind those bets the natural result is a selling of the currency, creating downside pressures.

"Therefore, we expect the weakness in the Dollar and Sterling in the near-term and strength in the yen and the Euro. Emerging market currencies will probably decline as weaker global growth and the risk-off environment is negative for these currencies," says Boele.

The most recent data covering the positioning of the market up until March 03 - which covered the late February market sell-off - showed that the net positioning for Sterling gains stood at 35162.

The Euro meanwhile saw net 'short' positions stand at 86.7K contracts, down from 114K a week prior, suggesting substantial scope for further weakness.

ABN AMRO now forecast the Pound-to-Dollar exchange rate to be at 1.26 at the end of the first quarter of 2020, 1.25 by the end of the second quarter, 1.28 by the end of the third quarter and 1.30 by year-end.

The Pound-to-Euro exchange rate is forecast at 1.15 by the end of the first quarter, 1.1360 at the end of the second quarter and at 1.12 by the end of the third and fourth quarters.