The Euro remained well supported on Friday after the release of Manufacturing data confirmed analyst's expectations of continued growth in the sector.

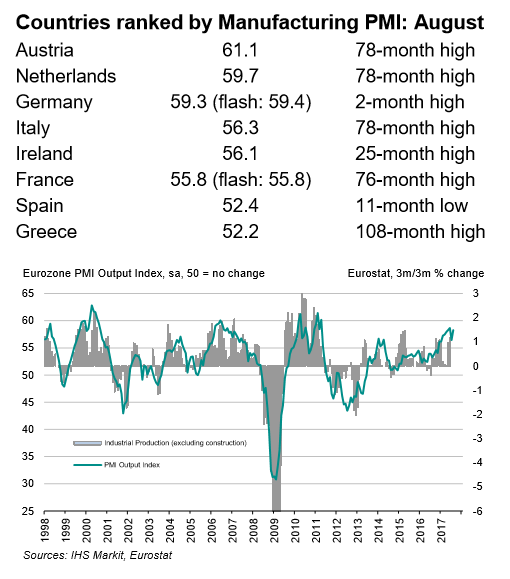

The final estimate for IHS Markit Eurozone Manufacturing PMI (Purchasing Managers' Index), a survey of managers in the Manufacturing Industry, rose to 57.4 in August, up from 56.6 in July and equalling June’s 74-month high.

A reading of over 50 indicates expansion and of below 50 contraction.

Eurozone PMI has remained above the 50.0 mark for 50 successive months now, and activity in May, June, and August has been particularly intense.

Growth in the region was mainly driven by Germany, the Netherlands, and Austria, according to the report, although all the countries bar Spain saw growth hit new multi-month highs.

Markit said: "August saw euro area manufacturing production rise at one of the fastest rates since April 2011, bettered or equaled only by the expansions seen in May and June of this year. The trend in new order inflows also improved, with the rate of expansion similarly among the best since early-2011."

Fears that the strong Euro might be hampering export competitiveness were not supported by the data which showed growth equally balanced between domestic and export markets, and exports hitting a "six and a half year high".

The data also showed pressure rising from backlogs of orders as companies struggled to keep pace with new orders.

This, in turn, led to a rise in employment as companies sought to bring new staff onboard to cope with the increased demand.

Prices also rose in August both for raw materials (input) and end products (output), feeding into heightened inflation expectations.

ECB Reticent

Given the recent strong Eurozone inflation data which came out at 1.5% instead of the 1.4% predicted and strong data releases from the Euro-area could probably provide the Euro with an additional boost, which could see EUR/USD revisit the 1.20s.

This may not be as welcome as it sounds, since mutterings from the European Central Bank (ECB) have indicated that the governing council is not happy with the strong Euro, as it hampers exports.

With eyes now turning towards next Thursday's ECB rate meeting a further upmove in the Euro could lead to speculation Draghi may pull up the drawbridge for an exit on monetary stimulus and tapering may be put off to another day.

"The euro traders could have mood swings before next week’s European Central Bank (ECB) meeting, provided that the strong euro revived discussions about an eventual reluctance from the ECB to exit the Quantitative Easing (QE) program at the desired speed. Strong euro may move the ECB away from its 2% inflation target," said LCG's dealing team on the subject.

Later in the morning we may get confirmation from the 'horses mouth' as it were when ECB's vice-president Vitor Constancio gives a press conference.

Hello, Non-Farm Payrolls

The US monthly Labour report, or Non-Farm Payrolls as it is more commonly known is the big release for the Dollar on Friday.

Current market expectations are for a 180k result, which would be down from the 209k of the previous month (July).

SEB Bank's Mattias Bruér is of the opinion that the actual result may dissapoint due to seasonal factors.

"The seasonal pattern is suggesting that employment growth in August will be much lower compared to the 209k expansion in July; in five of the past six years August payrolls have been weaker than the July number and the average absolute difference is 65k (unrevised data). While history doesn’t repeat itself, it often rhymes and against that backdrop 144k employment growth is a reasonable guess."

He goes on to say that, "this is not a bad number per see, but nevertheless a sizable miss and a headline grabber. The consensus is opting for 180k and our official forecast is at 190k."

Could the Dollar take a hit after NFPs?

Bruer notes that it's not suo much the payrolls number now but the wages figure which has the greater impact on Fed expectations.

"According to our analysis, the US Phillips curve is still alive and as such the continued tightening of the labour market should result in accelerating wage growth eventually; another monthly gain of 0.3% should push y/y hourly earnings growth up to 2.7% and by the end of 2017 a 3-handle is reasonable."

With the market pricing in only a 33.8% chance of a rate hike from the Fed in December odds are tenuous.