Image © Adobe Images

The Euro could retest early August lows in the coming days, warn FX strategists.

"EUR/USD could conceivably fall back to 1.14," says strategist Kit Juckes at Société Générale.

This assessment comes as market attention returns to France, where the government of Francois Bayrou faces a confidence vote on September 08 that he is likely to lose.

This opens the door to a period of political and financial uncertainty in Europe's second-largest economy, and already we are starting to see the Euro reflect this.

The Euro to Dollar exchange rate (EUR/USD) fell through the midweek session and into Thursday as France's bond yields - the interest rate paid to those who lend money to France - have risen to account to perceptions of rising risk.

Juckes says EUR/USD could fall back to 1.14 if the difference between the yield on French bonds and those of Germany widens to around 90 basis points.

The last time this happened was in December when Michel Barnier's government was ousted. "At that point, against a different economic backdrop, EUR/USD fell below 1.05," says Juckes.

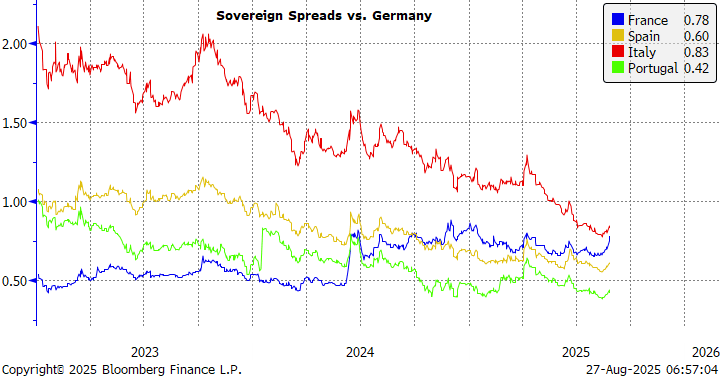

When it comes to Europe, we measure investor anxiety by measuring how a country's bonds are trading relative to those of Germany. This is because Germany is considered the European safe haven, courtesy of its sheer size and fiscal prudence.

When a bond's interest rate (yield) rises faster than that of its German equivalent, we say its 'spread' with Germany has increased. This indicates that the market's risk perception of that country's bonds are rising; in this case it is France that is under the spotlight.

As the chart below shows, the French-German spread is rising again:

Image courtesy of Brown Brothers Harriman.

"Wider European sovereign spreads still correlate with a weaker euro, even if the relationship is less significant than it was before Mario Draghi's 'whatever it takes' intervention."

Analysts are able to map the Euro's performance against changes in the French-German spread, and they find that small changes are typically inconsequential.

However, when a certain threshold is reached, the currency market takes notice and the Euro comes under pressure, as was the case in December, and to a lesser degree in April.

Consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

"In April this year, when the spread widened to 80bp (marginally wider than it is today) we saw EUR/USD's upward momentum merely stall, and when the bond market quietened down, the rally to 1.15 resumed. There's a clear danger that this mini crisis lasts longer," says Juckes.

Analysis from ING bank shows that the euro’s correlation with EU bond spreads to German bunds tends to be either very low most of the time or quite high for short bursts.

For Italian bonds, the pain threshold was around 200 basis points. "For French bonds, we don’t have enough history to be sure, but a break above December’s high of 90bp (currently 77bp) can trigger a significant euro reaction," says Francesco Pesole, FX Strategist at ING Bank.

However, there are warnings that the window for Euro-Dollar weakness could be brief.

"Given the absence of generalised fiscal uncertainty across the Eurozone region, we also do not expect the latest French developments to have a long-lasting impact on the euro over the medium-term," says Nick Bennenbroek, an economist at Wells Fargo.

In December the Government of Michel Barnier was voted down, and the Euro fell, but soon recovered. The episode provides the market with a blueprint of what to expect heading into the Septermber vote, which does cut through the fog of uncertainty.

Given this, the potential for significant moves in the exchange rate market is lessened somewhat.

"We also note the "bad outcome" is already a base case, which means the market impact is more likely to happen now - if at all - rather than on September 8," says Daniel Tobon, an analyst at Citi.