Image © European Commission Audiovisual Services

Foreign exchange strategists at Goldman Sachs say they are minded to maintain a positive medium-term forecast profile for the Euro relative to the Dollar, seeing it leaping 1.10 over coming months.

The Wall Street bank is however not yet willing to make a buy recommendation, primarily because the Ukraine war remains a tail risk to their assumptions for a recovery in the Euro.

The call comes as the Euro to Dollar exchange rate recovers from its early May floor at 1.0349, leading to speculation that the bottom might have been reached.

"Could we be setting up for a continued rebound in the single currency?" asks Zach Pandl, Co-head of FX Strategy at Goldman Sachs. "This is a possibility in certain scenarios."

For a meaningful rebound to transpire the U.S. economy must slow faster than that of the Eurozone.

"We see downside risks to U.S. growth," says Pandl.

Goldman Sachs anticipate the European Central Bank's (ECB) looming exit from negative rates to have a meaningful positive impact on fixed income flows as the incentive to hold Eurozone bonds improves.

This flow is expected by Goldman Sachs to "support the single currency over time".

Euro exchange rates rose on May 23 after ECB President Christine Lagarde cemented expectations for a July interest rate hike.

"I expect net purchases under the APP to end very early in the third quarter," said Lagarde in a post on the ECB's website. "This would allow us a rate lift-off at our meeting in July, in line with our forward guidance."

The Euro rose sharply against most major currencies in the wake of the comments, with a quarter of a percent advance being registered against the Pound and a more substantial 1.0% gain coming against the Dollar.

"The conditions facing monetary policy have changed markedly. Three shocks have combined to push inflation to record highs," said Lagarde.

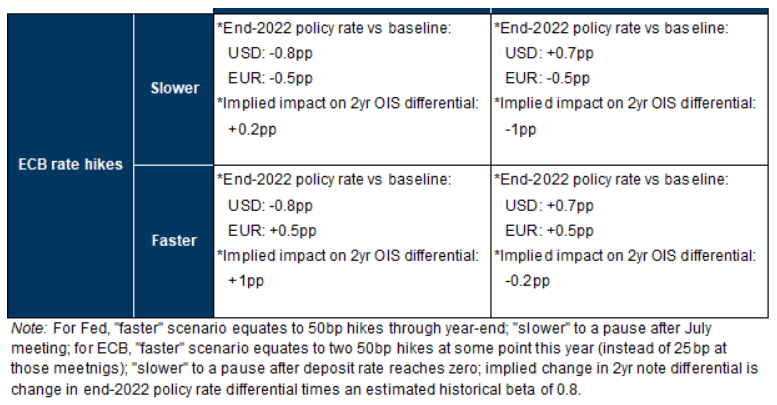

Goldman Sachs have strategies four different potential scenarios whereby the Fed and ECB alter their current paths on delivering rate hikes.

"Divergence between the two central banks this year could move 2yr note differentials by as much as ~100bp, which implies a +/- 8% move in EUR/USD, all else equal," says Pandl.

Above: "Euro Could see Continued Rebound if Fed Slows, ECB Quickens Pace". Image courtesy of Goldman Sachs.

However, Goldman Sachs cautions it might yet be too soon to all-out back the Euro given the conflict in Ukraine continues.

Instead they recommend selling the Dollar against the Yen as an expression of a view the U.S. economy could be about to slow materially.

"Tail risks from the Russia/Ukraine war remain an important challenge," says Pandl. "While a full halt to Russia gas exports is not our expectation, any perceived change in the probability of that outcome can affect markets, given the severity of the possible impact on Euro Area growth".

Goldman Sachs economists forecast a -2.2% hit to the Eurozone economy under such a scenario.

Nevertheless, "given our views on the US economy, the broad Dollar’s high valuation, and the imminent end to negative cash rates in Europe, we are sticking with our constructive medium-term forecasts for EUR/USD," says Pandl.

Goldman Sachs forecast the Euro-Dollar rate at 1.15 in twelve months. (Set your FX rate alert here).