- EUR/USD steadies after retreat back below 1.14

- But ECB-Fed divergence set to grow heavier still

- Rising inflation risks could see ECB move faster

- But EZ vulnerabilities could see it weigh on EUR

ECB President Christine Lagarde. Image: Andreas Reeg/ECB.

For the Euro to Dollar exchange rate the gulf between central banks on each side of the Atlantic is set to become a more daunting headwind that could all but rule out any prospect of a recovery in the months ahead.

Europe’s single currency edged higher on Friday as a nascent slide in global stock markets extended and some commodity prices came under pressure, although it was still set to end the week lower against many major counterparts including the Dollar.

While risk aversion in global markets helped the Euro advance tepidly against many peers on Friday, it had previously lagged behind all but the Swedish Krona and was unable to capitalise from earlier declines in the U.S. Dollar exchange rates.

One possible reason for this is a European Central Bank (ECB) monetary policy that was underlined afresh with burdensome clarity this week, and which could become a greater headwind for the single currency over the coming months.

“Lagarde stuck to message, saying that inflation is expected to continue to decline in 2023 and 2024—which would imply no hikes until some point in 2024—while noting that the ECB is ready to respond to elevated inflation if necessary,” says Shaun Osborne, chief FX strategist at Scotiabank.

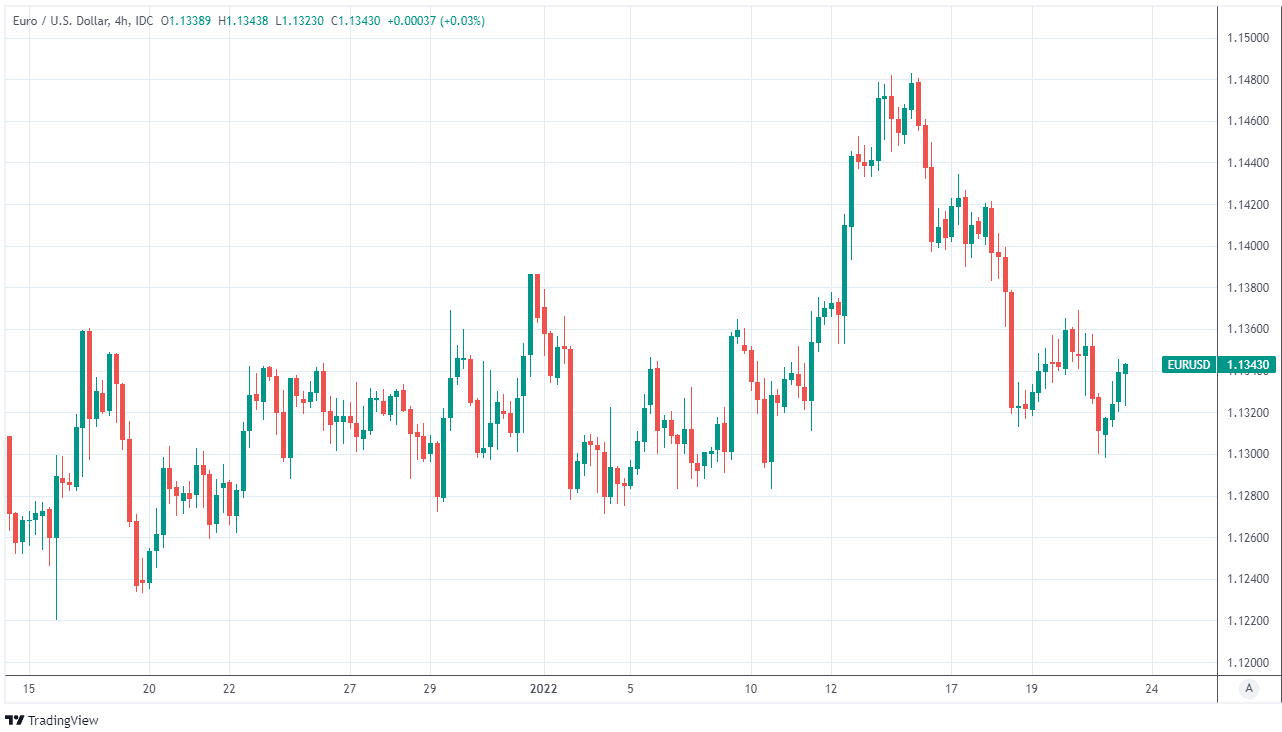

Above: Euro-Dollar rate shown at 4-hour intervals.

- EUR/USD reference rates at publication:

Spot: 1.1350 - High street bank rates (indicative band): 1.0935-1.1032

- Payment specialist rates (indicative band): 1.1250-1.1293

- Find out more about market-beating rates and service, here

- Set up an exchange rate alert, here

"As inflation in the Eurozone decelerates, we think markets will begin to remove bets on the ECB hiking as soon as September/October, and the EUR should head back toward 1.10 in the coming quarters,” Osborne and colleagues said in a Thursday research note.

ECB President Christine Lagarde was reported to have reiterated on Thursday, in an interview with France Inter radio station, that Europe’s economies are expected to escape the eye watering inflation rates seen in the U.S. during recent months.

This is why the ECB feels able to wait patiently for inflation to decline of its own accord even as surging prices lead the Federal Reserve (Fed) into a scramble to withdraw the monetary policy support provided by it to the U.S. and global economies since the onset of the pandemic.

"The ECB remains committed to substantial monetary policy support for now, but the scepticism towards further asset purchases is growing and rate hikes will come into play in 2023. Upside inflation risks already worry the central bank," says Jan von Gerich, an economist at Nordea Markets.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

While the ECB has put in place a plan to steadily end some of the government bond purchases carried out under its quantitative easing programmes, it remained adamant that some of those purchases will need to continue and that its interest rates are unlikely to change this year or next.

That’s been a burden for the Euro already, although one that could grow heavier still if the ECB’s assumptions about inflation prove to be too optimistic and if as a result, further increases in price pressures begin to argue for a faster pace of stimulus withdrawal during the year ahead.

“We have flagged the risk of an abrupt shift in the ECB's policy stance multiple times during the past 2 months. Credit spreads in the Euro Area indicate this risk is still perceived to be low. But recent price developments in the German economy make us uneasy about the monetary policy backdrop,” says Stephen Gallo, European head of FX strategy at BMO Capital Markets.

“As such, we are conscious of the 'squeeze risks' from net-short positions in the EUR on numerous axes, if the ECB is forced into another policy shift (we say 'forced' because we believe the preference at the highest level of ECB decision-making is for the central bank to remain deeply involved in Euro Area debt markets on a permanent basis). But we're also anxious about the relative health of the currency if ECB support is withdrawn,” he added.

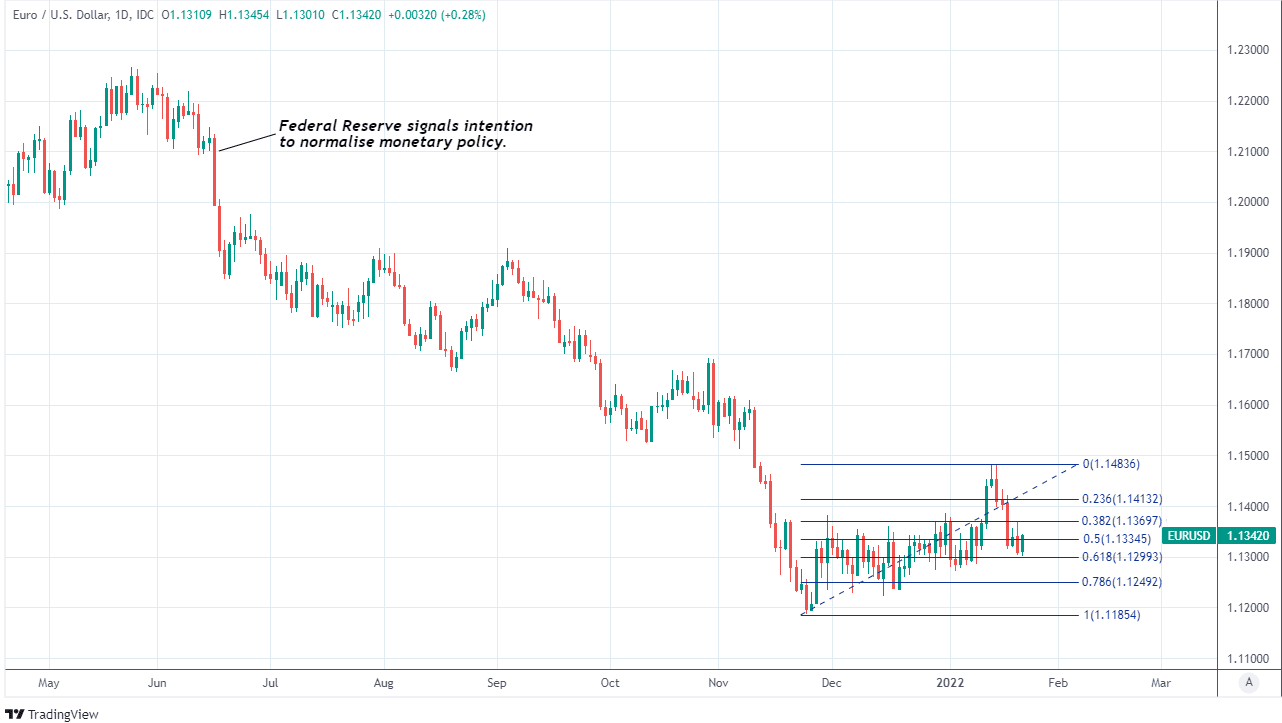

Above: Euro-Dollar rate shown at daily intervals with Fibonacci retracements of December rebound indicating possible areas of technical support.

There are reasons for why the ECB could prove to be too optimistic when assuming that inflation will fall back below the bank’s target of its own accord, and there are other reasons for why a faster pace of stimulus withdrawal in Europe may not be quite the fillip for the Euro that it has been for the Dollar.

“The US did not go through a debt crisis in 2010 to 2012, the Fed did not have to intervene to control that. As a result, the Fed is not under suspicion that when implementing its monetary policy, it is considering that asset purchases might be made for anything but monetary policy motives,” says Ulrich Leuchtmann, head of FX research at Commerzbank, writing in a Friday market commentary.

Minutes from December’s monetary policy meeting released this week showed the ECB’s forecast for a natural and unassisted decline in inflation later this year is built upon the assumption that energy price inflation will fall over the course of 2022, and double-digit-percentage commodity price gains thus far in January have already challenged that outlook.

The potential problem for the Euro is that if a sustained increase of inflation does pressure the ECB to withdraw its monetary stimulus at a faster pace, financial markets may worry about the impact higher borrowing costs could have on some of the more fragile Eurozone economies.

This might deprive the single currency of the same benefits enjoyed by the Dollar as a result of the Fed’s policy shift.

That would be especially likely if rising bond yields made borrowing costs prohibitive for some European economies.

Thursday’s minutes confirmed that this risk was already under consideration at the ECB in relation to December’s decision to begin reducing its footprint in the Eurozone bond market and is often referred to by the bank as threat “financial fragmentation” or “market fragmentation.”