Image © Adobe Images

- EUR/USD reference rates at publication:

- Spot: 1.1580

- Bank transfers (indicative guide): 1.1175-1.1256

- Money transfer specialist rates (indicative): 1.1478-1.1522

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

Eurozone inflation rose sharply in September and is expected to extend higher during the fourth quarter.

However Euro exchange rates failed to respond as early 2022 should see the rate of price increases start to decline, according to economists.

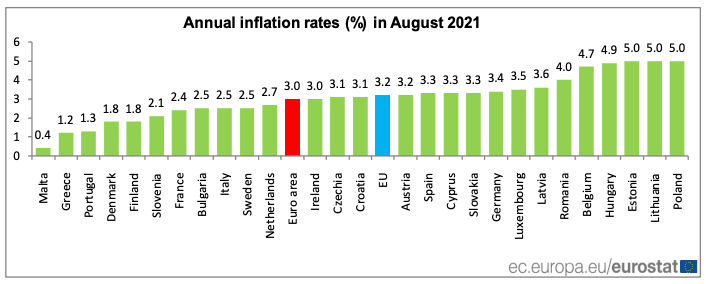

Eurozone inflation reached a decade high in September, rising 3.4% year-on-year from 3.0% in August, beating the 3.3% print the consensus was expecting.

"Eurozone inflation is still advancing," says Claus Vistesen, Chief Eurozone Economist at Pantheon Macroeconomics, adding that both core and headline inflation will remain elevated in the fourth quarter.

Eurostat says the highest contribution to the annual euro area inflation rate came from energy (+1.44 percentage points, pp), followed by non-energy industrial goods (+0.65 pp) and food, alcohol & tobacco and services (both +0.43 pp).

"Inflation concerns arising from food and energy prices continue to be a point of concern in Europe," says Selena Ling, Head of Research & Strategy at OCBC Bank.

The ECB in September raised its long-term inflation projections to 2.2% for 2021, 1.7% for 2022 and 1.5% for 2023.

The ECB's core inflation is now forecast at 1.3% for 2021, 1.4% for 2022 and 1.5% for 2023.

As can be seen in the above projections, the ECB estimates that the spike in inflation will be temporary and that it will fall well below its 2.0% target by 2022.

Euro exchange rates will therefore be little bothered by inflation data until it becomes clear Eurozone inflation is moving to 2.0% - and above - during the 2022-2023 period.

Vistesen says the contribution of energy prices to the Eurozone's inflation mix means the Eurozone's inflation rate is unlikely to materially impact the ECB's inflation expectations, and therefore policy.

"History is pretty clear; when energy components go vertical in y/y terms, they only do so for a short while, even if the price level remains elevated," he says.

The latest Eurozone inflation data comes amidst a spike in investor concerns that global inflation will stay elevated for a longer-than-anticipated stretch of time as global supply chain issues remain stubbornly disrupted.

The surge in European gas prices is of particular concern owing to stubbornly low Russian imports and intense bidding with Asia for any available seaborne natural gas supplies.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Numerous central banks have come out this week to warn that the longer the supply-side inflationary pressures seen over recent weeks persist the greater the chance they start impacting inflation elsewhere.

For example, if consumers believe inflation will continue to rise they will start demanding higher wages, business respond by raising their own prices.

Hence, a spiral is born.

"Supply-side disruptions and a reopening bump in prices could be drivers of a more lasting rise in inflation, insofar as goes the possibility that they lead to a sustained shift in firms’ price setting," says Vistesen.

Pantheon Macroeconomics nevertheless still expects Eurozone inflation to drop in the first quarter of 2022.

They expect ECB policy to remain accommodative as although the emergency quantitative easing programme (PEPP) will cease in March the longer-running APP will be augmented and run at €40B per month.

The big picture then is that the current inflation bout is unlikely to shift the dial on the Euro's longer-term inflation problem.