- EUR/USD poised to end historic 2020 year with near-10% gain.

- But new as well old challenges now lurk on path ahead for 2021.

- Virus woe grows ECB's share of bond market to new extremes.

- Policy risks stoking German euroscepticism ahead of election.

File image: Image © Alfred Yaghobzadeh, European Commission Audiovisual Services. Webpage image; Lady Justice statue, Frankfurt © Adobe Images.

- EUR/USD spot rate at time of writing: 1.2247

- Bank transfer rate (indicative guide): 1.1832-1.1918

- FX specialist providers (indicative guide): 1.2060-1.2155

- More information on FX specialist rates here

The Euro is on course to end the year strengthened by a near-double-digit gain over a depreciated Dollar but will face a cocktail of risks in 2021 and beyond, including a coronavirus that increasingly threatens to foster an already-present euroscepticism at the very heart of the common currency bloc.

Europe's single currency was 9.17% higher against a down and out Dollar for 2020 on Tuesday having benefited from both a depreciation of the U.S. currency as well as renewed investor interest for reasons of its own merit, although by many accounts the rally is not yet done.

Bullish forecasts abound still, in anticipation of a global economic recovery that favours exporting countries and currencies, as well as a further deflation of the greenback. However, the single currency's suitors may be overlooking the prospect of a sharp rise in euroscepticism within the Eurozone's largest economy and financial sponsor, Germany, and federal elections scheduled for September 2021 could act as a wake-up call.

Especially as since the last occasion when voters had an opportunity to express their views in such a way, European Central Bank (ECB) monetary policy has likely become a greater concern for any Germans who lean toward euroscepticism. The ECB has increased its ever-incendiary footprint in the Eurozone government bond market significantly since the federal election of September 2017, and is set to go on doing so for a while yet.

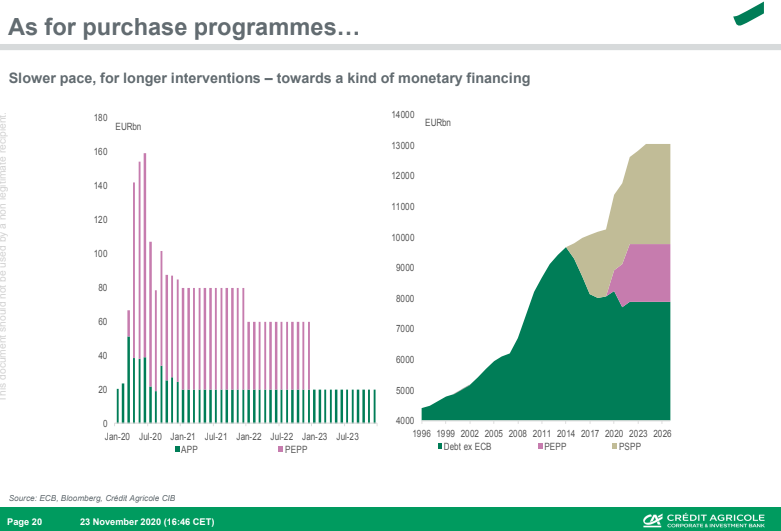

"The ECB has recently pledged €1T in QE between now and Q1 2022, probably enough to suck up somewhere around 80% of net sovereign debt issuance over the same period," says Claus Vistesen, chief Eurozone economist at Pantheon Macroeconomics. "The ECB is more or less explicitly tailoring its asset purchases to the pace of government debt issuance...It's difficult to imagine a political backlash against fiscal and monetary support at this point, but not that it might change, eventually."

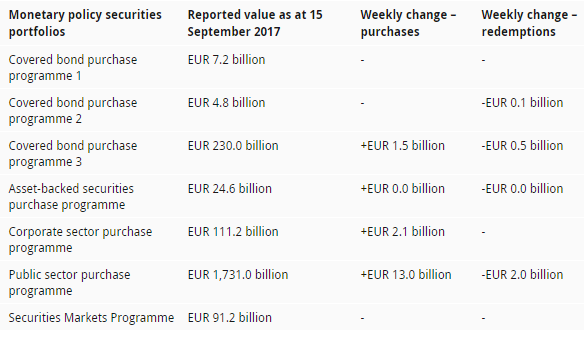

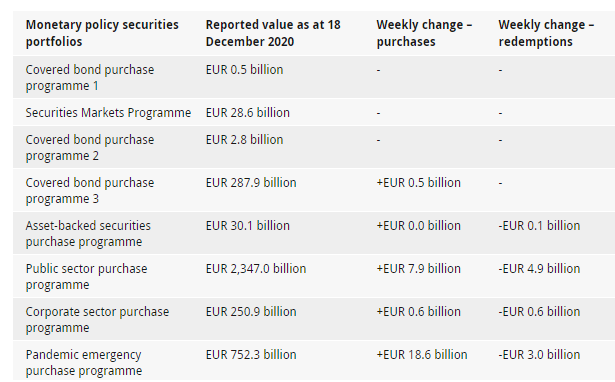

Above: ECB's monetary policy asset holdings in September 2017 (left) and December 2020 (right).

At the time of the last election the ECB owned an estimated 17.5% share of the Eurozone government debt market but had set out a clear plan for a steady winding down of its quantitative easing programme, which was responsible for adding the bonds to it balance sheet in what was an unsuccessful bid to stimulate the economy into producing the near-2% inflation target that has mostly eluded ECB since the debt crisis.

In June 2017, the ECB hinted at plans to taper off its controversial bond buying programme while minutes of its latest meeting confirmed ahead of Germany's September election that it was in fact planning to end purchases later that year. It successfully, but ill-fatedly ended the programme in December 2018, before being forced in September 2019 to resume purchases in response to subpar economic growth and ebbing inflation pressures.

Dear fellow German economists, if you are wondering what you can do for Europe: Please help to dispel the harmful & wrong narratives about the @ecb's monetary policy, floating around in political and media circles. These threaten the euro more than many other things.

— Isabel Schnabel (@Isabel_Schnabel) November 20, 2019

But 2019's resumption of QE and the unprecedented economic disruption of 2020 have now seen the bank's government debt holdings grow to €3.01 trillion, which is equivalent to nearly 30% of the available supply. And by the time Germans head to the polls in September 2021, the bank is expected to hold closer to €4 trillion of Eurozone government bonds on its balance sheet. Also, and increasingly, these bonds will be those issued by Meditteranean nations who've often been painted and perceived as profligate in the past.

"Some German eurosceptics have repeatedly asked the German supreme court in Karlsruhe to outlaw some unconventional ECB policy responses," says Holger Schmieding, chief economist at Berenberg, in briefing ahead of May's constitutional court ruling on the legality of some of the ECB's policies.

Germans especially have long opposed Frankenstein's Monster-like policies that have proven popular with many central banks, in what external observers have sometimes interpreted as a psychological scar born of the hyperinflation that caused widespread suffering in the country during the early part of the 20th century. Many Germans have long viewed the quantitative easing programmes of the ECB and others suspiciously.

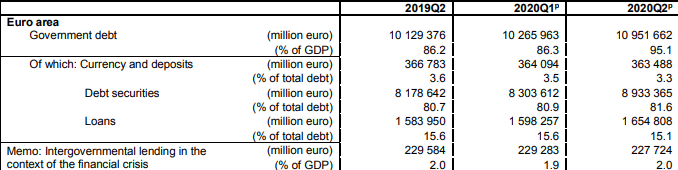

Above: European Commission estimates.

To some, quantitative easing is tantamount to a backdoor financing of governments that is in this case an inordinate risk to the family finances, a perception that could only be bolstered by the fact that in 2020 the ECB has necessarily tilted its bond purchases further in the favour of 'periphery' nations than is advised by its so-called capital key. The bank faces having to continue doing that for at least the foreseeable future. Furthermore, and adding insult to injury for eurosceptics of the German variety, hard-won fiscal rules that were negotiated as a form of quid pro quo for debt crisis-era aid to deficit countries have been suspended and their fate is unknown.

"Neither Corona nor the euro justify the German taxpayers being blamed for the debts of the whole EU," says Jörg Meuthen, federal spokesperson of the opposition Alternative for Germany (Alternative fur Deutschland, AFD) in an April statement which opposed the concept of so-called coronabonds.

AfD brings a new lawsuit against the #ECB this time challenging #PEPP as monetary financing. Tricky one, b/C the ECJ itself - when ruling on PSPP - effectively elevated the legal standing of the self imposed limits that the ECB said it would ditch for PEPP https://t.co/JoZiXJDJEi

— Silvia Merler (@SMerler) June 17, 2020

This could become a bigger political issue if a continued suspension of the so-called stability and growth pact is perceived as handing Mediterranean nations a de facto licence to grow the ECB's balance sheet at will, or because a familiar and public European political process is facilitating the return of a post-crisis fiscal order which for years made austerity a mandatory menu item and source of political risk in Southern Europe.

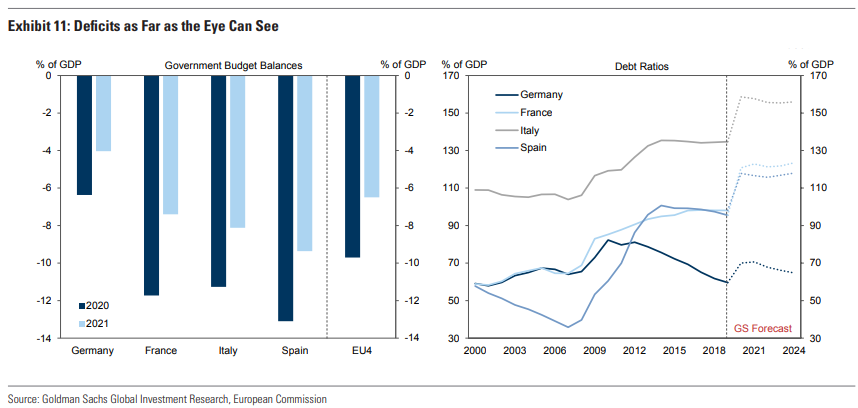

"Although subdued in the shadow of the pandemic, the risk of political fragmentation still exists, especially in Southern countries. In Spain, this relates to regional fragmentation, which is likely to resurface as soon as the emergency ends. In Italy and Northern countries, it relates mainly to the popularity of the Eurosceptic parties, which remain a strong political force," says Stven Jari Stehn, chief Europe economist at Goldman Sachs, contemplating risks to an otherwise positive outlook. "Tensions around the upcoming discussion in Europe about the monitoring of the Recovery Plan funds and the reactivation of the EU fiscal surveillance framework are likely. A too lax (stringent) approach could create tensions in the net contributor (beneficiary) countries, risking another anti-European populist wave. These risks could resurface with the upcoming national elections in 2021 (Germany and the Netherlands) and 2022 (France and, possibly, Italy after the election of the President)."

Above: Deficit & debt-to-gdp ratios for major Eurozone economies. Source: Goldman Sachs Investment Research.

Germany's Constitutional Court already attempted this year to withdraw its central bank from participation in the ECB's bond buying programme, although in an action that was initiated long before the pandemic as well as at a point when the stability and growth pact fiscal rules were still in full force. The regulations enabled the enforcement of a distinctly Germanic form of financial discipline across the Eurozone in what was a victory at the time for those who'd opposed the idea that they, already the Euro's main underwriters, should finance the bailout and recovery of 'profligate' countries who'd gone from boom-to-bust following the financial crisis.

The European Commission suspended the rules in 2020 to prevent them hampering the response to the pandemic, although inevitably, a highly political decision will have to be made sooner or later as to whether and what extent they return. Neglecting to reimpose them while the ECB goes on" tailoring its asset purchases to the pace of government debt issuance," would be an incendiary if-not unthinkable proposition for many in Germany and possibly a gift to the AfD, a party that was formed by academics and financial professionals in 2013 with the objective of withdrawing the country from the Euro.

One key lesson from the last 30 years in British politics is that the Eurosceptics were consistently underestimated. In the 1990s, they were laughed at. In the 2000s, they were derided as loonies, fruitcakes & racists. In the 2010s, as Little Englanders. Yet still, they won.

— Matt Goodwin (@GoodwinMJ) December 23, 2020

It's not without irony that these post-crisis quid-pro-quo rules have led to only dissatisfaction in Germany as well as Southern Europe. Mandatory deficit and debt reduction targets have served only to limit the growth in GDP and population that determines a country's contribution to, and share of the ECB's capital key. This is best thought of as an instruction manual or template for the apportionment of policy support monies and the like. Subsequently, and over the medium-to-long term, this forced austerity reduces those countries' shares of the capital key and simultaneously accentuates their need for ECB support.

"Purchases of public sector bonds have been carried out with some flexibility with respect to the capital key and in particular have exceeded the capital keys for Italy and, more moderately, for Spain and France, while they have been lower for Germany and the Netherlands," says Chiara Cremonesi, deputy head of fixed income strategy at UniCredit. "The ECB has been purchasing a significant amount of short-maturity debt, particularly in core countries and depending on how issuance has been structured."

Source: Credit Agricole.

As a result, the post-crisis fiscal rules entrench the very circumstances which originally led the ECB to develop a greater footprint in periphery markets, and could yet necessitate an ever further deviation from the capital key in favour of the 'periphery,' thus imposing a form of backdoor monetisation of Southern Europe's deficits. Perhaps this is a poetic attempt by often circular and self-propelling forces of nature to resolve the seemingly-intractable problem underlying much of the above; the ongoing absence of a fiscal union to accompany the monetary union in the Eurozone?

Investors have long assumed that if the bloc is ever again to find itself the subject of breakup speculation, it would be because a country like Italy is openly contemplating vaulting a Euro-denominated wall. Yet it's possible if-not likely that before then, the ECB will arrive at a point where it can no longer purchase another Italian bond without prompting a palpable fallout in Berlin, with possible implications for perceptions of Germany's likely future commitment to the Euro.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

2021 and after will reveal the extent of euroscepticism in Germany, not to mention a handful of other European countries, and along the way the European Council's 2020 reform to the budget process might be found triggering ugly political scenes every autumn. After all, that reform gave each national leader a veto over other countries individual budgets, in addition to their existing veto over the entire EU budget.

Feelings run high when @Nigel_Farage ‘s name is mentioned...however it’s time he became Sir Nigel Farage...

— Lord Ashcroft (@LordAshcroft) December 27, 2020

Meanwhile, a cautionary tale is in Britain's Brexit saga, which illustrates among other things how supposedly fringe political actors need not necessarily ascend to the highest office or even any office at all in order to shape the political landscape for years if-not decades to come.

One of the many questions that might be worth keeping in mind as the year and its happenings unfold is; which opinion poll warned that Britons would vote in sufficient number for Brexit and Americans for a President Donald Trump?

Above: Euro-to-Dollar rate shown at monthly intervals.