The rally in GBP/EUR is by no means over says a leading foreign exchange analyst.

The GBP/EUR pair has risen from the 1.09s of the October flash crash to November highs at 1.18 with a good boost being provided by the US election result on November 9.

The pair has however been unable to breach the resistance point at 1.18 with questions being asked if the uptrend is in danger of stalling and reversing.

Our technical analysis of the pair suggests it is still to early to argue the uptrend is over, however other studies do see signs of weakness.

For a fundamental spin on the the outlook we have received a timely note from Lloyds Bank Commercial Banking’s Gahan Mahadevan which argues that the period of appreciation for GBP/EUR is not yet done.

Mahadevan sees more upside for the pair into 2017.

A difference in the path of interest rates, set by the central banks of the UK and Eurozone, is said to underpin the current rise in GBP/EUR.

And importantly, the divergence is tipped to extend.

UK interest rates are expected to remain broadly unchanged whilst in the Eurozone they are expected to fall, or at least remained at low levels due to the European Central Bank’s (ECB’s) policies.

The note comes as the ECB's Mario Draghi tells the European Parliament on Monday, November 28 that the ECB will do all it can to keep policy accommodative enough to boost inflation.

Thus, the Bank may announce an extension of its QE programme as early as next week’s ECB meeting while the likelihood of a similar extension to the Bank of England's QE programme remains remote at best.

This is likely to keep a cap on Euro upside and keep the Pound underpinned as the UK's interest rates advantage attracts more foreign capital which in turn strengthens the currency.

"The recent GBP/EUR rally has been well supported by interest rate divergence. Having bottomed-out in August, and held support in October, UK yields (5-year and 10-year) have been on a sharp upward trajectory," says Mahadevan.

Further upside for the Pound is seen as government bond yields stay elevated as they chase US yields higher after Trump’s victory.

The European debt market has remained expensive, however, due to expectations of more bond buying from the ECB, and this has kept the yields on that debt relatively low.

"In contrast, short-dated German yields (2-year) made new record lows, with the noteworthy divergence assisting GBP/EUR in its recent move higher," says Mahadevan.

The difference in the price of debt and the yield rates will increase flows to Sterling pushing up GBP/EUR.

"We expect UK gilt yields, especially in the 5y-10y segment, to increase further over the forecast horizon, driven by higher US yields," says a note from Danske Bank backing the theme of a more robust Sterling profile.

The rise in UK yields and the Pound has been driven by four factors argue Lloyds:

Firstly, the rise in inflation expectations following GBP’s significant depreciation since June;

Secondly, the realisation that monetary policy may have reached its limits;

Thirdly, the possibility that future fiscal spending in the UK could worsen the government’s budgetary position and increase inflationary pressures; finally, the rise in US yields dragging UK yields with them.

Latest Pound/Euro Exchange Rates

| Live: 1.17▼ -0.05%12 Month Best:1.1719 |

*Your Bank's Retail Rate

| 1.1302 - 1.1349 |

**Independent Specialist | 1.1536 - 1.1583 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Political Risk to Keep Euro Capped

Then there is the Euro side of the equation.

Whilst political risk had been a dampener on the Euro its impact is starting to wear off due to improving prospects, particularly for the outcome of the French Presidential election.

“The odds of non-centrist outcomes in the upcoming Italian constitutional referendum and next year’s French and German elections have narrowed significantly,” said Mahadevan.

This should keep enthusiasm for a Euro rally in check.

However, fears appear to have moderated considerably.

The prospect of anti-EU Marine Le Pen winning the French presidency have narrowed after primaries saw the centre-right Francois Fillon take the nomination.

Fillon is already a fairly right-wing politician whose policies share considerable overlap with Le Pen, except in the more extremist and anti-EU areas.

He is, therefore, likely to appeal to many of the same voters as Le Pen, who might see some of her core vote migrate over to Fillon who is more likely to beat her than some of the other potential contenders would have been, such as Nicholas Sarkozy for example.

Of all the candidates she could have met he is considered the most likely to beat her.

GBP/EUR

Daily Chart Showing live Inter-Bank Rate and Indicative Rates for International Payments.

Italian Referendum Could Hurt the Euro

In Italy, which has a referendum on December 4, Mahadevan calculates only a 15% probability of a snap election, which is a possibility if Matteo Renzi loses and resigns.

It is only in the case of a snap election that he anti-EU Five Star party could grab power and take Italy out of the Euro.

The Lloyds analyst says:

“PM Renzi is lagging behind in the polls by more than 7 percentage points – and therefore there is a possibility of him losing the vote and deciding to subsequently tender his resignation.

“This would increase political uncertainty in the Eurozone even further, however, as we outline in our scenario analysis, we believe there is a 40% chance that the Italian populace will support Renzi’s position by voting ‘yes’, and less than a 15% probability that the referendum will lead to snap election.”

Nevertheless, Renzi’s defeat could move markets temporarily whilst everyone is uncertain as to whether a new government can be formed without re-election, and this could force the Euro down in the short-term, possibly lifting the pound for a few weeks.

Downside Risks: UK Political Landscape Unclear

The Pound seems to have settled on a bed of low-level, uncertainty ahead of the triggering of Article 50.

Yet uncertainty remains and this remains the one weakness undermining Sterling.

It is still unclear whether PM Theresa May will be able to trigger Article 50 without consulting Parliament – the case is to be heard by the Supreme Court, 5th – 8th December, and a ruling will likely be announced early next year.

Until the ruling on Brexit, the pound is likely to be moved by changes in data, which currently seems to be coming out better-than-expected.

Last week’s Business Investment data for Q3 for example beat market estimates and although still down over one and a half percent on the year nevertheless showed a resilient economy bearing up better-than-expected.

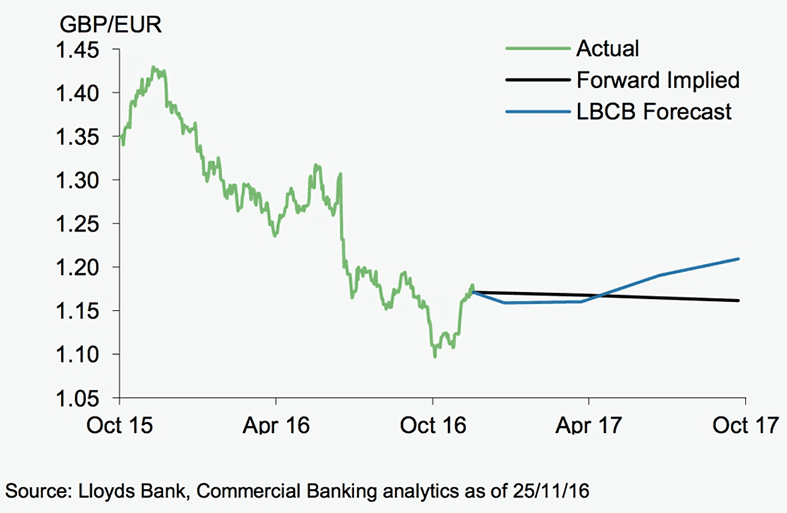

Forecasts for GBP/EUR

“Overall, given our macroeconomic outlook, we anticipate GBP/EUR settling around 1.16 at year-end, before continuing on its upward trajectory towards 1.21 by end-2017,” Mahadevan says.