Image © Adobe Images

Week Ahead Forecast: GBP/EUR trades with a firm bias, although building political risks and an ECB rate hike should conspire with formidable technicals to prevent a breach of 1.16.

The pound to euro exchange rate starts Monday on a softer footing, at 1.1568, most likely due to news of renewed tensions in the Middle East, where Israel attacked Tehran overnight.

"Stock and bond markets are under pressure from a triple headwind: a pullback of the AI trade, rising Fed rate hike expectations, and a jump in crude oil prices triggered by escalating tensions between Iran and Israel," says Elias Haddad, Global Head of Markets Strategy at Brown Brothers Harriman.

Risk-off sentiment is a natural headwind to GBP/EUR and explains Monday's deflated price, but declines related to the Middle East tend to be shallow, as investors see risks as contained by the backstop of U.S. President Donald Trump's need for the conflict to end.

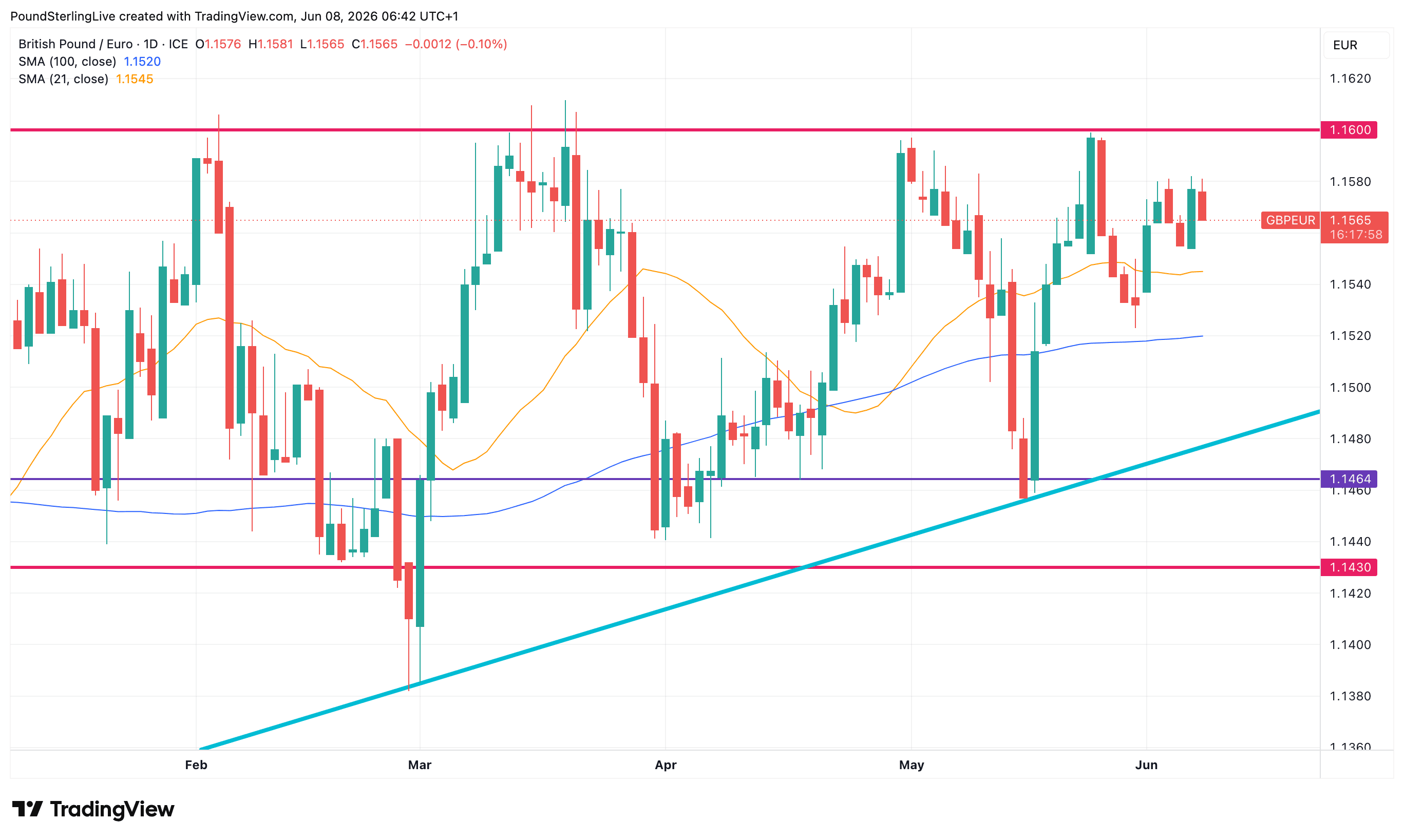

Early losses are not yet large enough to erase Friday's solid 0.20% advance, a move that underscored the constructive technical setup underpinning short-term GBP/EUR action; the broader post-Budget uptrend, in place since November, remains intact while support levels continue to hold:

The pair sits above both its rising 100-day moving average near 1.1520 and the ascending trendline that has underpinned trade since November, suggesting sterling retains an underlying advantage against the euro.

Importantly, recent pullbacks have been relatively shallow, with buyers consistently emerging above the 1.1540–1.1520 region.

However, the chart also highlights a familiar challenge: resistance at 1.1600. Sterling has now tested this area on multiple occasions since February without securing a decisive breakout, making it the defining level for the medium-term outlook.

While repeated tests can weaken resistance over time, the lack of follow-through above 1.1600 suggests sellers remain active near the top of the range.

The moving-average structure remains supportive. The 21-day moving average is above the 100-day moving average and both are trending higher, reflecting positive medium-term momentum. Price continues to trade above both averages, reinforcing the view that dips are currently corrective rather than the start of a broader reversal.

So although a move above 1.16 is not forecast, the pair is expected to remain above 1.1554 this week.

Euro Week Ahead: ECB Rate Hike

The coming week will see the European Central Bank (ECB) likely raise interest rates to guard against the prospect of Eurozone inflation running too hot in the coming months.

This insurance hike will surprise no one and is therefore 'in the price' of the euro, meaning it will be the guidance that has the ability to move the market. Specifically, does the ECB hint at the need for another rate hike in the coming months? If yes, then the euro could strengthen on the day, if no, it would likely weaken.

"Since inflation is likely to remain above the 3% mark for longer, we now expect not only one rate hike at the next ECB meeting on June 11, but also a second one," says Commerzbank in a recent assessment.

The challenge for euro 'bulls', though, is that the market is looking for up to three hikes this year. Anything less and then a repricing lower in expectations occurs, which can weigh on the single currency.

We don't see the ECB event challenging the constructive GBP/EUR setup.

UK Week Ahead: Politics Heats Up

Bigger risks to GBP/EUR upside are likely to emerge from the UK side of the equation.

There is some GDP data due for release in the UK this week, on Friday. Economists have generally been looking for something in the region of -0.1% to -0.2% month-on-month, reflecting a payback from the strong Q1 growth of 0.6%. It would also reflect signs that higher energy prices and rising borrowing costs have started to weigh on activity.

Anything worse, and GBP struggles into the weekend; anything stronger, and the pair could strengthen.

Political risks will increasingly be in focus given we're approaching the Makerfield by-election, due 18 June.

Andy Burnham is the firm favourite to win, meaning markets must begin to pay attention to the fact that his victory means he will be able to take on Keir Starmer in a Labour Party leadership election.

"Political fever heats up this week thanks to the Makerfield by-election. Although voting itself does not take place until Thursday 18th, campaigning and coverage of the poll will intensify," said Philip Shaw, economist at Investec, on the same day Andy Burnham confirms he will challenge Keir Starmer for Prime Minister.

The concern for markets is that Burnham has consistently hinted at the need to take the government in a leftward direction, meaning more spending and borrowing, something markets will struggle to absorb.

Late last week he failed - not once, but twice - to explain what the fiscal rules actually are, despite insisting he would stick to them if he entered Downing Street.

Speaking to Victoria Derbyshire on Newsnight, Burnham repeatedly sidestepped the question, saying he was "not going to go through… an exam on the fiscal rules."

The rules require the government's current budget balance to fall as a share of GDP in the medium-term (currently 2029/30). As it stands, the current government will oversee a significant squeeze on households via tax rises that are backdated to the end of the parliamentary term in order to meet the rules.

Burnham will therefore inherit a very difficult fiscal landscape if he is to replace Starmer, and the risk is that he tries to loosen the rules to seek his government's re-election.

For currency and fixed income markets, the process of pricing those risks starts soon.