Image © Adobe Images

Gas prices are forecast to ease through the winter according to Goldman Sachs, a view if correct should ease downside pressure on the Euro.

The Eurozone's single currency is proving highly response to gas prices, with the new sub-parity levels against the Dollar coming amidst surging prices.

A recovery by the Euro over the course of September has meanwhile coincided with an ongoing decline in gas prices; therefore further gas price declines would prove supportive.

"We maintain our view that, while at higher levels than what we expected previously, TTF prices will decline sequentially through winter," says Samantha Dart, Head of Natural Gas Research at Goldman Sachs.

Gains by the Euro against other currencies, including the Pound, have been evident through the course of September amidst falling gas prices.

The GBP/EUR exchange rate has retreated from around 1.1850 to current levels around 1.1518. The below charts shows both TTF gas prices and GBP/EUR peaked in August:

Above: GBP/EUR has retreated as gas prices have fallen. To stay on top of this market, set your free FX rate alert here.

"In case gas prices actually start to fall more noticeably over the next few months, due to storage facilities seeming to be comparatively well-filled, especially in Germany, a less deep or at most a mild recession can be expected, which would ultimately support the EUR," says analyst Marc-André Fongern, Managing Director at Fongern Global Forex.

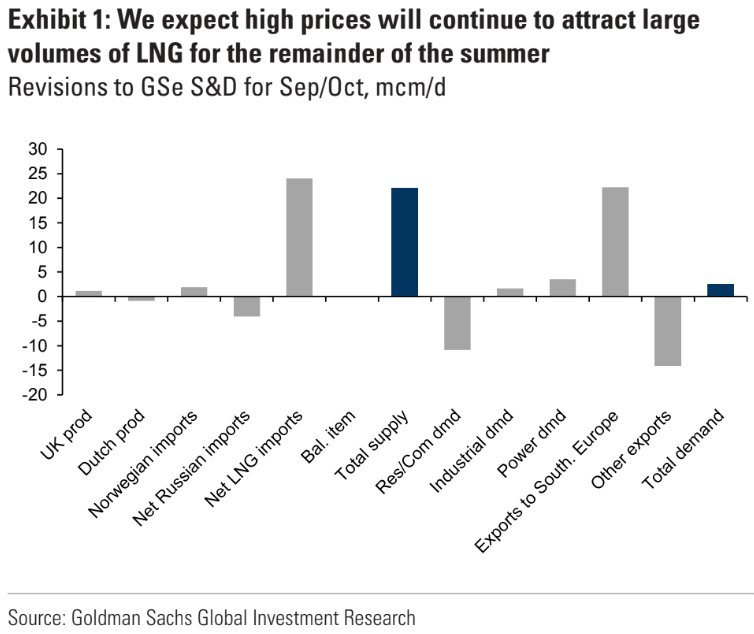

But, ahead of the winter prices should remain elevated as Europe seeks to attract cargoes of Liquified Natural Gas (LNG).

"While we expect TTF prices sustained above 200 Eur for the remainder of summer to continue to attract LNG at or above the high rates we've seen recently, leading us to modestly increase our Sep/Oct expected LNG imports into NW Europe by about 20 mcm/d to 190 mcm/d," says Dart.

The need for seaborne gas deliveries to Europe come amidst the near-total shutdown in the flow of Russian gas into Europe.

Russia's Gazprom on Sept. 02 announced an indefinite shut down of the Nordstream 1 pipeline, the crucial artery that carries gas from Russia to Germany.

But in doing so Russia played their final card from the geopolitical sense: an indefinite shutdown always posed the 'worst case scenario' outcome for the German and European economyies with regards to gas supply.

That the worst has now come to pass inherently brings an end to speculative excess in gas and currency markets.

"Peak pessimism seems to have been hit for the time being, but I do urge caution, the ongoing geopolitical landscape remains highly vulnerable and indeed volatile," says Fongern.

Goldman Sachs says the shutdown of Nordstream 1 has been mitigated by a combination of European gas demand destruction and imports via alternative channels.

They expect European gas storage levels to continue rising to a 90% threshold by the end of October.

Goldman Sachs forecasts TTF natural gas prices to fall to below 100 EUR/MWh by the first quarter of 2023.

This represents a halving from current levels, but relies on a average winter weather conditions in the region.

"As we go through winter, we expect the high storage levels at the start of the season to accommodate larger-than-average storage withdrawals, still leaving over 20% of full by end-Mar23," says Dart.

"We note that our winter TTF expectations are far lower than current prices - and lower than winter forwards. The higher the storage level at the start of the season, the easier for balances to accommodate larger-than-average storage withdrawals without threatening a stock-out. This implies a higher tolerance for lower prices vs current, and their associated higher demand," she adds.