- GBP/EUR supported at 1.17, may see new highs

- If BoE’s inflation stance continues to inspire GBP

- BoE rolling up sleeves as inflation rises on agenda

- Crisis rate cuts could be reversed from early 2022

- BoE speeches, GDP eyed for next clues on outlook

Image © Pound Sterling Live

- GBP/EUR reference rates at publication:

- Spot: 1.1788

- Bank transfers (indicative guide): 1.1475-1.1558

- Money transfer specialist rates (indicative): 1.1682-1.1730

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Pound-to-Euro exchange rate has rallied sharply and could be apt to rise further over the coming days should the seemingly shifting interest rate stance of the Bank of England (BoE) continue to inspire market confidence and appetite for Pound Sterling.

Sterling was one of the better performing major currencies last week having advanced against all counterparts in the G10 contingent except the oil-linked Canadian Dollar and Norwegian Krone, while the Pound notched up its largest gains over a retreating Euro and Japanese Yen.

The Pound-Euro exchange rate entered the new week above 1.1750 after rising more than one percent previously when global markets extended their rebound from late September losses and after traders appeared to reward the BoE’s attentiveness to mounting inflation risks.

“Obviously I am concerned with inflation above target,” Governor Andrew Bailey told Yorkshire Post in an interview reported on Saturday.

“We are going to have a very delicate and challenging job on our hands so we have got to in a sense prevent the thing becoming permanently embedded because that would obviously be very damaging,” the governor also said after warning that further price increases are likely ahead.

Remarks from Governor Andrew Bailey and the typically more ‘hawkish’ Monetary Policy Committee (MPC) member Michael Saunders demonstrated again at the weekend how inflation is rising up the agenda and shifting the BoE’s thinking on the interest rate outlook.

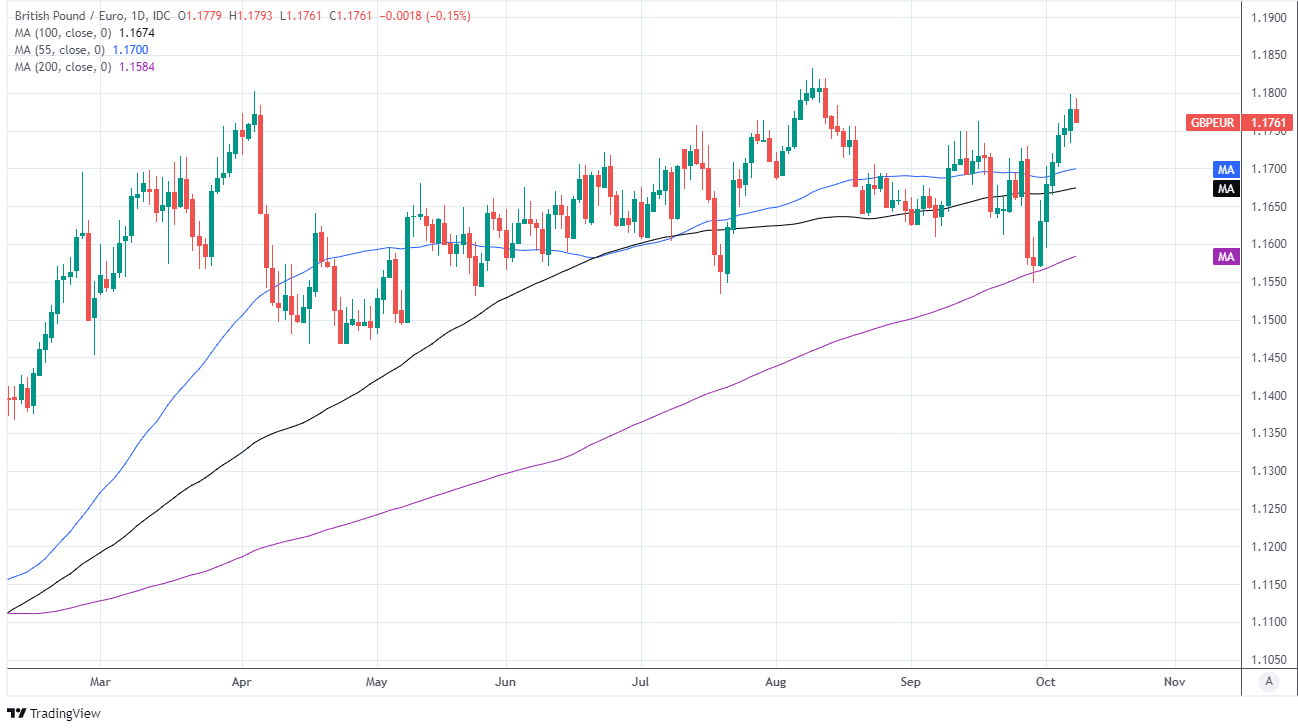

Above: GBP/EUR at daily intervals with 55, 100 & 200-day averages indicating possible areas of support at 1.17, 1.1674 & 1.1584 respectively.

“I think it is appropriate that the markets have moved to pricing a significantly earlier path of tightening than they did previously,” the BoE’s Saunders told The Telegraph on Saturday.

The BoE and various members of the nine seat MPC have suggested of late the bank could begin reversing last year’s interest rate cuts at any point in the months ahead - though perhaps unlikely before the early months of 2022 - to minimise the risk of inflation exceeding the 2% target for too long.

Inflation reached 3.2% in August while the BoE has projected that it would exceed 4% by year-end before falling only slowly thereafter, although this was before natural gas prices surged by double-digit percentages in late September and early October.

“The prospects of a BoE hike help to cushion GBP, especially relative to low-yielders like the EUR,” says Mark McCormick, global head of FX strategy at TD Securities, who tipped GBP/EUR as a buy at 1.1607 on September 30 and is looking for it to rise as far as 1.1976 in the coming months.

Commodity price increases would mostly cause only a temporary burst of inflation but now that price pressures have become embedded in the national news agenda and popular conversation the danger is that business and household expectations for inflation also begin to rise sharply in response.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Rising expectations could trigger a self-perpetuating cycle of rising prices if corporate pricing intentions and workers’ wage demands are also raised as a result, which is a risk that may explain more than any other why the BoE has rolled up its sleeves and made clear a readiness to lift interest rates.

“And if expectations rise by more than the increase in actual inflation would suggest and/or they don’t fall back as actual inflation falls next year, then the Bank may raise interest rates earlier and faster than we currently expect,” says Bethany Beckett, an economist at Capital Economics.

The BoE’s readiness reflects "the primacy" of the inflation target in the UK monetary policy framework, according to minutes of the BoE's September meeting, and will be in focus again over the coming days as MPC members including Deputy Governor Jon Cunliffe, Slyvana Tenreyro and Catherine Mann air their own views on monetary policy in public engagements this week.

Sterling could be sensitive to the views expressed whichever way they cut, although it’s relevant that these three members are the closest thing the MPC has to a ‘dovish camp’ as this means there’s every chance the views aired may not be so supportive of the Pound.

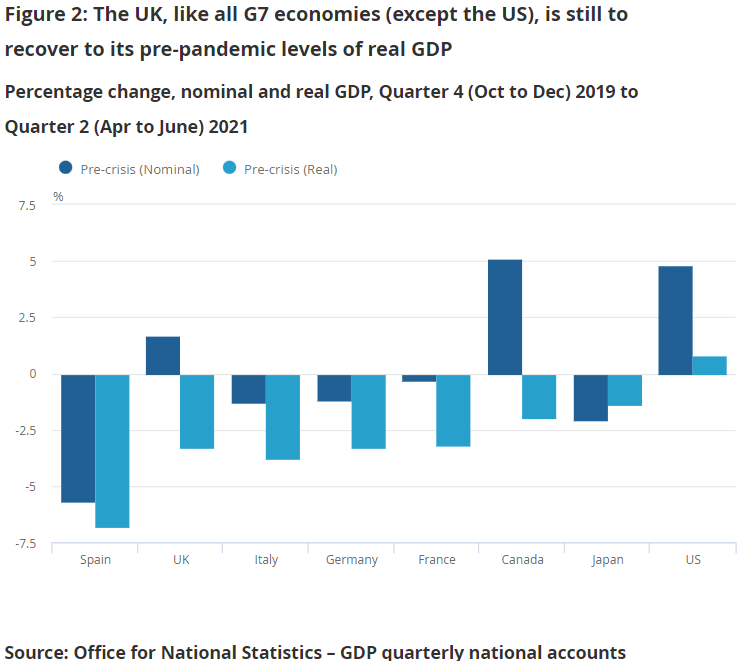

Along the way Wednesday’s GDP number for August will be of enhanced importance because it will provide clues about the likely time over which the economy could be expected to recoup the remainder of the GDP lost to coronavirus containment attempts in 2020.

Above: UK GDP compared with pre-crisis level before (nominal) and after (real) inflation is taken into account. Source: ONS.

"While we're not completely out of the water I expect us to be back to the pre-pandemic level, certainly in the early part of next year, but possibly a month or two later than we thought we would be in the summer," Governor Baileysaid in a panel discussion at the annual ECB Forum on Central Banking on September 29.

The Office for National Statistics recently estimated the shortfall of GDP as -3.3% when the second quarter is compared with the final quarter of 2019.

“The recovery in GDP slowed to a crawl in July, as a rise in Covid cases and the consequent surge in the number of people asked to self-isolate caused significant disruption, But August’s data should bring better news,” says Andrew Goodwin, chief UK economist at Oxford Economics, who looks for GDP to rise by 0.6% for August.

“Covid-related disruption will have fallen, given the drop in cases and the introduction of less-stringent rules on self-isolating. And social consumption sectors should see strong pickups in activity in response to the lifting of most of the remaining Covid restrictions in late-July,” Goodwin wrote in a Friday research briefing.

Wednesday’s GDP data is doubly important because September’s MPC meeting minutes suggested that a majority on the committee may want to see the shortfall of GDP fully recovered before voting to lift the Bank Rate.

The same majority also seeks to better understand what happened to employment and unemployment levels following September’s closure of the government’s furlough scheme given that around 1.6 million workers were still reliant on the scheme in some form at the end of August.

“We expect the unemployment rate to rise only to 5.0% in Q4, from 4.5% in Q3. But underemployment likely will soar, as people return on fewer hours than they want,” says Samuel Tombs, chief UK economist at Pantheon Macroeconomics

The 45 day gap between the end of a reporting period and the publication of official ONS figures means it will be year-end almost before anybody knows for sure what happened to the job market, while it will be February 2022 before final quarter GDP data is in.

This is why the early months of 2022 could be the most likely of times for any interest rate rises that may or may not emerge from the BoE.

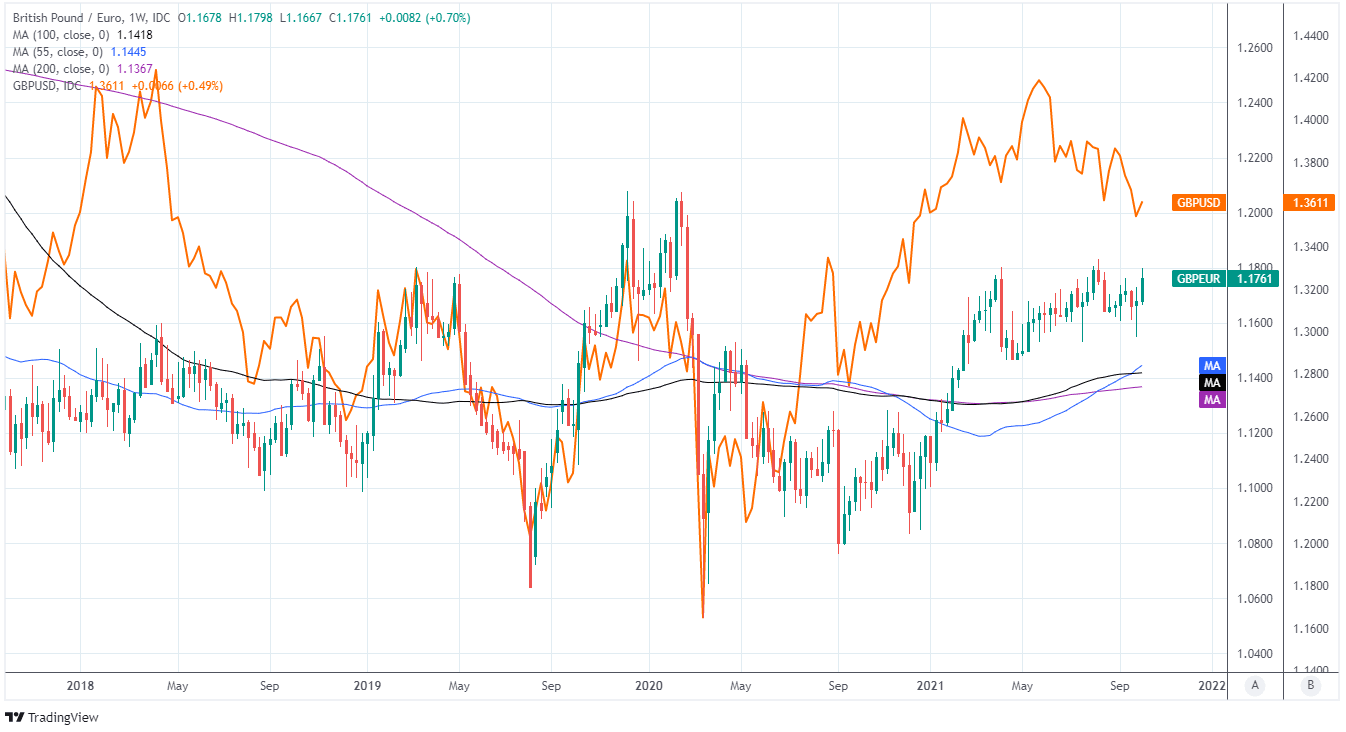

Above: Pound-to-Euro rate shown at weekly intervals with major moving-averages and shown alongside GBP/USD.