- Barclays says "GBP vulnerable"

- BNY Mellon says BoE "will probably disappoint"

- Another analyst warns of 'hawkish' surprise

Image © Adobe Stock

The Bank of England event on Thursday could disappoint those eyeing a stronger British Pound say analysts at two leading global investment banks.

The Bank of England (BoE) will deliver a monthly policy decision as well as its quarterly Monetary Policy Report, it is on these occasions that substantive guidance changes are typically issued which can often encourage currency market volatility.

Ahead of the event, research teams at Barclays and Bank of New York Mellon (BNY Mellon) say the Pound is unlikely to receive a boost from a central bank which will prove unequivocally cautious.

"Even though the market may be looking for an optimistic tone from the BoE and sterling’s recent recovery across the board reflects such views, the Monetary Policy Committee (MPC) will probably disappoint parts of the market anticipating mentioning of tapering, let alone hikes," says Geoff Yu, FX and Macro Strategist for EMEA at BNY Mellon.

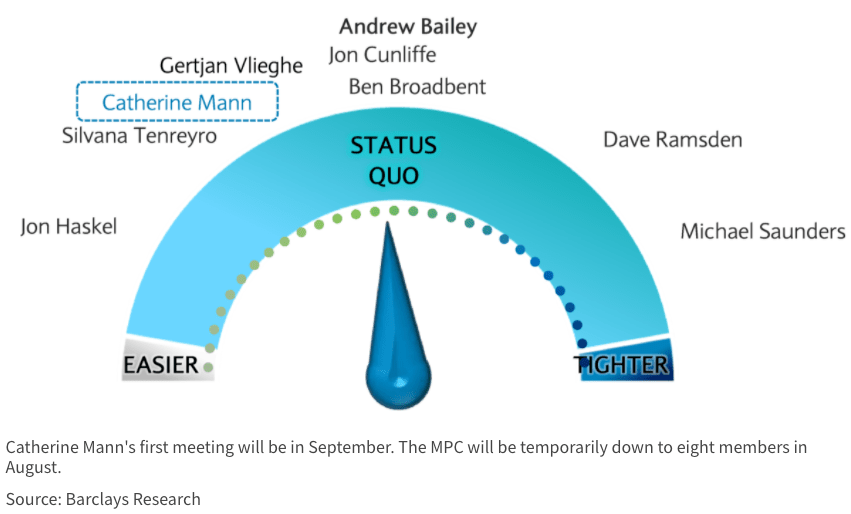

Foreign exchange strategists at Barclays say the market will focus on the vote count on whether or not to end the BoE's asset purchase programme (quantitative easing) ahead of the existing December cutoff, as well as the updated medium-term inflation forecasts to assess any incremental move towards tightening.

July saw a number of MPC members offer their views on the outlook for the economy with two - Michael Saunders and Dave Ramsden - saying inflation levels risked sitting above the BoE's target 2.0% level for an uncomfortably elevated period.

As such, the time for a rate rise was approaching in their opinion.

The views steered the market to price in a first rate rise in 2022 which was seen as supportive of the Pound. "Expectations for at least one hike in 2022 to take the base rate to 50bps by year-end have remained relatively stable," says Yu.

Whether the BoE's guidance entices that 'lift off' date towards the start of the year or pushes it back into 2023 will have implications for the Pound: if the date comes forward expect the Pound to rise, if it is pushed back expect it to fall.

"Two BoE members’ recent hawkish rhetoric has raised market expectations that more members will vote for a reduction in the Bank’s asset purchase target. We expect these expectations to be disappointed, leaving the GBP vulnerable to a temporary move lower," says Marvin Barth, Head of FX and EM Macro Strategy at Barclays.

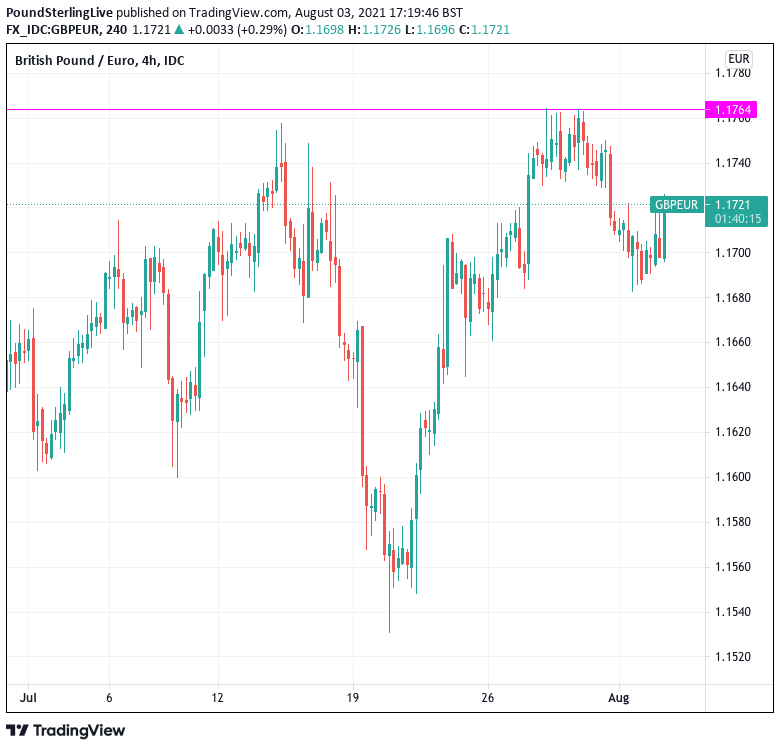

The British Pound has settled somewhat ahead of the Thursday event, understandably so given investors would not want to be caught on the wrong side of the market heading into the event.

The Pound-to-Euro exchange rate trades around the 1.17 mark while the Pound-to-Dollar looks capped by 1.39.

Breaks towards fresh 2021 highs in GBP/EUR located at 1.18 are possible in the event of a hawkish outcome, while GBP/USD could retest levels above 1.40.

But, strategists at BNY Mellon are not convinced the time for such moves is now, saying the BoE wants greater clarity concerning the state of the country's labour market.

"Because of the scale of the government’s intervention in the labor market, the BoE has avoided basing decisions on present employment numbers due to high distortion risk – especially for wage growth," says Yu.

The Government will in September end their employment support schemes, which could trigger a sharp rise in unemployment.

Economists say the BoE will want to assess the scale of the unemployment jump before pegging down a date for a future rate rise, something alluded to recently by the BoE's newest member Catherine Mann in her appearance before the House of Commons Treasury Select Committee.

"Any hikes over the next 18 months will purely be precautionary, reflecting the UK economy has recovered to pre-pandemic levels. However, there is not enough data to suggest that that there is enough growth momentum to push through a full hiking cycle," says Yu.

Indeed, BNY Mellon reflects the pace of the UK's economic rebound has subsided over summer months, a development that came alongside a third wave in Covid-19 cases.

"It appears that the low-hanging fruit for growth was already picked during the post-Q1 lockdown period," says Yu.

Covid-19 cases have nevertheless started to come down and consumer and business confidence might pick up through the August and September period as a result.

Should the BoE touch on this positive development Sterling could benefit.

"We believe that Europe as a whole is most likely to follow the UK’s live with the virus approach which would support a more sustainable economic recovery, ultimately benefitting the region’s assets," says Yu.

But, for now patience is the watchword.

BNY Mellon says ultimately the BoE would want to wait until the labor market normalises to assess whether there are any structural constraints in the labor market, which would support more sustainable wage growth rather than a simple one-off recovery push.

"The process will be extremely cautious for governments and central banks alike, necessitating patience for investors looking to re-engage in GBP and EUR positions," says Yu.

Barclays expects the BoE to leave medium-term inflation forecasts unchanged, which they say risks further dispelling recent market perceptions of a growing 'hawkish' faction at the BoE (Saunders and Ramsden).

"Despite recent market perceptions of a growing hawkish faction at the BoE, we expect the MPC doves to pose downside risks to the GBP," says Barth.

Barclays expect the committee to vote 7-1 to keep asset purchases unchanged, with Saunders effectively replacing Haldane as the dissenter, leaving the overall MPC view largely unchanged from the previous meeting.

"We also expect the Bank’s medium-term inflation forecast to be broadly unchanged, despite a likely upward revision of its short-term forecasts," says Barth.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Data meanwhile shows investors have over the course of the past two weeks built up a net bet against the Pound, for the first time in months suggesting the currency market is not necessarily expecting a 'hawkish' BoE August update.

The elimination of the net 'long' bet on the Pound - i.e. a position that favoured gains in the currency - nevertheless means positioning is no longer a headwind to gains should the BoE surprise and come out on the 'hawkish' end of the spectrum.

"More sterling short positions could be jettisoned if the Bank of England's Monetary Policy Committee springs a hawkish surprise on Thursday," says Robert Howard, a Reuters market analyst.

He says a "shock trim" to the quantitative easing programme could boost the Pound, given that a 7-1 or 6-2 vote to keep quantitative easing running at full-speed is expected.

"The pound might also benefit from a larger than expected increase to the BoE's inflation projections, as this could raise the perceived probability of an earlier-than-expected BoE rate hike," says Howard. "Sterling may also react positively if the BoE sheds light on how and when it might throw its stimulus programme into reverse."

Lee Hardman, Currency Analyst with MUFG is on the more constructive side of expectations, saying in a recent monthly currency update briefing that the BoE meeting will see policy makers endorse current money market rates (for a rate hike by August 2022).

"The favourable macro backdrop helped by the early evidence of being in the final stage of the pandemic will likely be illustrated in the BoE’s updated MPR that will suggest a 2022 rate hike, which we see as GBP supportive from here," says Hardman.