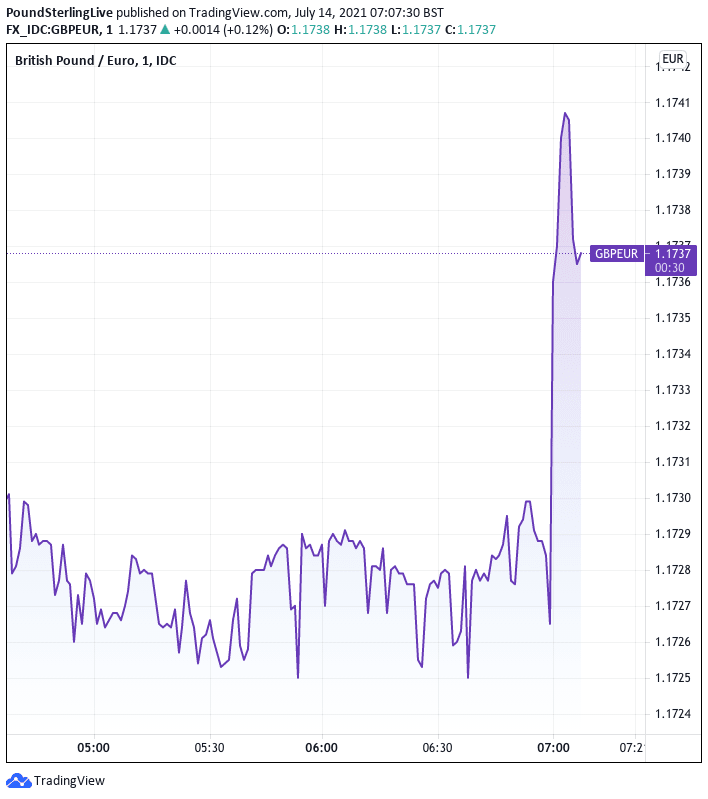

- GBP higher in mid-week trade

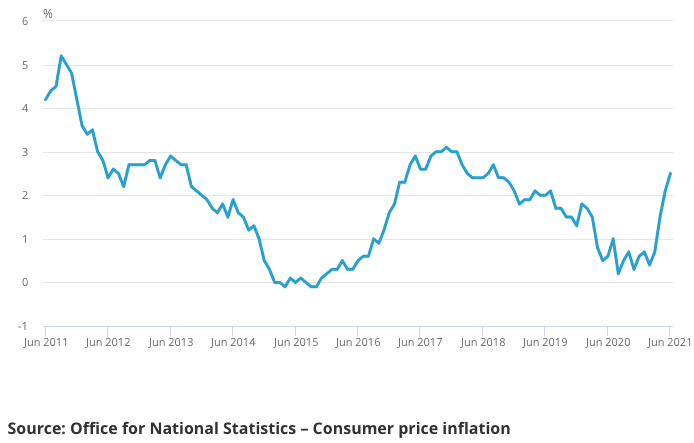

- Inflation hotter than expected

- Could go to 3% by year-end

- But back to 2.0% in 2022

Image © Adobe Images

- GBP/EUR reference rates at publication:

- Spot: 1.1737

- Bank transfers (indicative guide): 1.1420-1.1508

- Money transfer specialist rates (indicative): 1.1630-1.1655

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The British Pound was bid in mid-week trade following the release of UK inflation data for June which came in hotter than expected, prompting expectations that a 2022 Bank of England interest rate rise was increasingly likely.

According to the ONS, CPI inflation rose 2.5% year-on-year in June, which is greater than the 2.2% forecast by the market and the 2.1% reported in May.

Inflation rose 0.5% in the month to June, which is more than the 0.2% the market was expecting but less than the 0.6% reported in May.

Following the data the Pound-to-Euro exchange rate rose to its highest level since April, but the gains look at risk of fading (see why below).

The ONS says the contribution of transport costs has made a particularly notable contribution to inflation.

Transport has ranged from a downward contribution of 0.20 percentage points in May 2020 during the first lockdown to an upward contribution of 0.80 percentage points in June 2021.

This is the largest upward contribution from any component of the price basket this month.

Within transport, the movements have been caused principally by changes in the price of motor fuels which are in turn linked to a spike in global oil prices.

Stronger-than-expected inflation matters for a foreign exchange market that has become increasingly reactive to economic data as investors try and gauge when the world's central banks will raise interest rates from record lows.

Central banks raise interest rates in the face of heating inflation, as such a move acts to cool economic activity.

When expectations for a central bank interest rate rise comes forward, the currency that central bank issues tends to appreciate.

Money market pricing suggests the Bank of England is on target to raise interest rates in 2022, ahead of then European Central Bank and potentially the Federal Reserve.

This divergence proves supportive of the Pound, although the Fed might actually have to raise sooner given hot inflation in the U.S., as per yesterday's release. This helps explain why GBP/EUR is pointing higher while GBP/USD has lost value over recent weeks.

With inflation now above the Bank of England's 2.0% target the market might feel justified on betting on a 2022 interest rate by buying the Pound.

"Looking ahead, CPI inflation now looks likely to peak slightly above 3% at the end of this year, though we expect most of the further increase to be driven by food and energy prices," says Samuel Tombs, Chief U.K. Economist at Pantheon Macroeconomics.

The Bank of England is however of the view that inflation in the UK will prove temporary in nature and they are therefore willing to look through near-term 'noise' which has helped keep market expectations on the outlook for interest rates and the Pound in check.

The Pound's gains following the inflation data release might have been more significant were it not for some PPI inflation numbers that actually underwhelmed against expectations.

These input prices are suggesting some signs that supply-side pressures to prices might have turned a corner, with a number of readings coming in lower than expectations.

Producer Price Index inflation (output - also known as factory gate prices) read at 4.3% year-on-year, which is lower than the 4.8% forecast by markets and the 4.6% reported in May.

Producer Price Index inflation (input - which reflects the rising costs of commodities) read at 9.1% year-on-year, less than the 10.8% the market was looking for and the 10.7% reported in May.

The Producer Price Index matters as it shows price pressures earlier on in the production pipeline which will ultimately be passed on to consumers and reflect in the CPI.

The Bank of England will be aware that much of the spike in inflation in 2021 is down to 'base effects' - whereby current data is flattered by comparison to the unusual slump in prices a year prior. (The ONS has a good explainer here).

As the 'base effect' fades a more accurate picture of inflation emerges.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

However, the Covid crisis has had a significant impact on global supply chains, making some goods and components scarce.

This in turn reflects in the higher prices consumers are paying at the till.

The Bank of England believes that both the base effect and supply-side inflation will ultimately fade, leaving inflation at lower levels in coming months.

If the cost of fuel is providing upside pressure on inflation at present, then the recent cooling of global oil prices would be expected to be felt in the forecourt over coming months.

The risk however is that some prices prove sticky and don't simply just fade back as time passes, something the Bank's ex Chief Economist Andy Haldane has been particularly vocal about.

Indeed, a shortage of labour appears to be a potential feature of post-Covid UK which in turn puts pressure on wages.

Wage-lead inflation is something the Bank of England would be required to respond to with higher interest rates.

Pantheon Macroeconomics say that while inflation can be expected to rise further over the reminder of 2021, 2022 will likely see inflation ease back.

"The combination of sterling’s recent appreciation and fading lockdown-induced demand should ensure that core goods inflation eases over the next year, despite the increase in producer output prices," says Tombs.

Accordingly, Pantheon Macroeconomics think that CPI inflation will return to the 2% target in the second half of next year.

Such a decline would arguably take the pressure off the Bank of England to raise interest rates and it would therefore take some persistently stubborn inflation readings to really shift the dial on interest rate expectations and the Pound.