Image © lj16, accessed Flickr, Reproduced Under CC Licensing

- Euro gains in H2 on falling capital outflows

- Higher bund yields warning of change

- Deeper integration required to protect the Eurosystem

The Euro will rise in the second half of 2019 as the ability of the Eurozone to ‘export capital’ declines, limiting the extent of outflows, and this will reduce Euro-selling, says Hans Redeker, chief global FX analyst at Morgan Stanley.

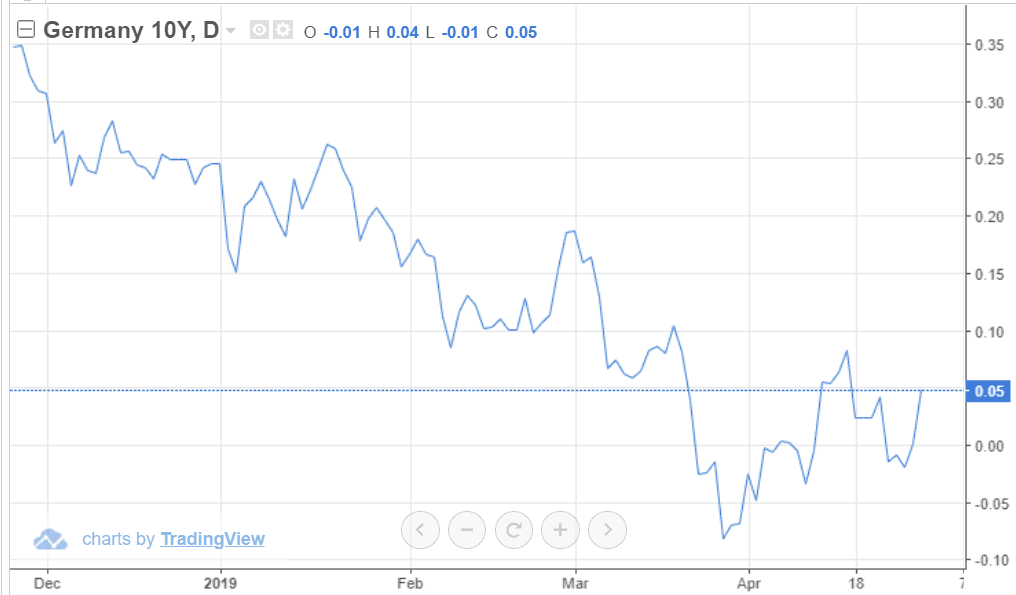

The main indicator capital flows are moving in favour of the Euro is a rise in the German bund yield, currently hovering at around 0.05% after bottoming and rising during April.

“The investment flow is the most important one to look at and the bund yield is a very good indicator of the behaviour of net savings in the Eurozone and when the bund yield goes up then obviously those net savings in the Eurozone go down and that actually means the ability of Europe to export capital, under those circumstances, would decline, and that would be positive for the Euro,” says Redeker in an interview with Bloomberg TV.

Above: The yield on Germany's 10-year sovereign bond could just be turning supportive of the Euro.

Easing political uncertainty after a win for the incumbent ruling party at the Spanish elections on Sunday may also prove supportive of the Euro.

The elections saw the Spanish socialist government returned with a larger share of the vote, which may have helped support the Euro. The populist threat from the Vox party, meanwhile, receded after it only picked up a handful of seats.

The political threat posed by anti-EU parties remains a distant threat it would appear.

“The heat is maybe coming off a little bit” says Redeker of political uncertainty in the region. “We have seen the case of Spain that populism can be contained if there is a high turnout in the election.”

One remaining major source of uncertainty for the Euro in the short-to-medium term, however, is the threat of auto-tariffs from America.

“The second uncertainty we still have to deal with is the auto-tariffs. We have not dealt with that, we have some deadlines to surpass in May, and then we will have to see how we are coming out of May, and if those auto-tariffs have been implemented, or implemented in only a weak form, or not implemented at all, if that would happen then you would certainly have a Euro rebound,” says the chief analyst.

Redeker sees the threat of financial stability risks to the Euro from years of ultra-loose monetary policy as fading, and is optimistic that deeper integration at a financial level with solve the problem.

The ultra-easy monetary policy adopted by the European Central Bank (ECB) has driven interest rates to rock-bottom levels and swelled the ECB balance sheet via a gargantuan money printing programme, and this means there is now not much scope for further easing in the event of an economic downturn. Further money printing (quantitative easing) would also be hampered by a lack of supply of eligible bonds for the ECB to purchase.

Under the quantitative easing programme the ECB creates money to buy corporate and sovereign bonds that meet its eligibility criteria. The purchase pumps money into the Eurozone economy with the intent of stimulating growth.

But, it appears eligible products to purchase are running dry, for instance there now exists a distinct lack of available German bunds, and this makes the Euro-area vulnerable in the case of a downturn.

“We all know that when it comes to the next downturn the Eurozone monetary policy is going to be much more constrained compared to the last economic downturn,” says Redeker. “We have reached the capital key limitation. We are running short of what we call safe assets.”

The solution says Redeker is to create deeper member state integration. This would be positive because it would help create more ‘safe-assets’. Currently, the safest assets are German bunds but if a Eurozone-wide bond was created then that could replace the bund. Such a pan-European bond could only be created, however, via fiscal union.

“That actually means we need to create safe assets at one point, and therefore we have to reform the Eurozone,” says Redeker. “I think there is no alternative to that. Even from a German perspective Target 2 imbalances come in at 1tr Euros that actually means that if the Eurozone would fail, then Germany is going to lose a lot of assets.”

“I think the core of Europe would be very well advised to press ahead with integration, the deepening of the Eurozone in a political process, in a capital market process, in a banking market process, therefore, having seen the limitations of the monetary policy it makes these reforms much more pressing. And I am an optimist I think it is going ahead,” adds the analyst.

Forecasts for the Euro

Morgan Stanley are forecasting the EUR/USD exchange rate to trade at 1.22 in the third quarter of 2019, ahead of a move to 1.25 in the final quarter.

It appears however that the lion's share of the move could be driven by a turn lower in the U.S. Dollar which the bank believes will be the major story in global FX in the second half of the year.

The EUR/GBP exchange rate is meanwhile forecast at 0.83 in the third quarter, ahead of a move down to 0.82.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement