UK economic growth was aided by a jump in exports and a surprise rise in business investment which has been labelled "another major blow to Brexit doomsayers".

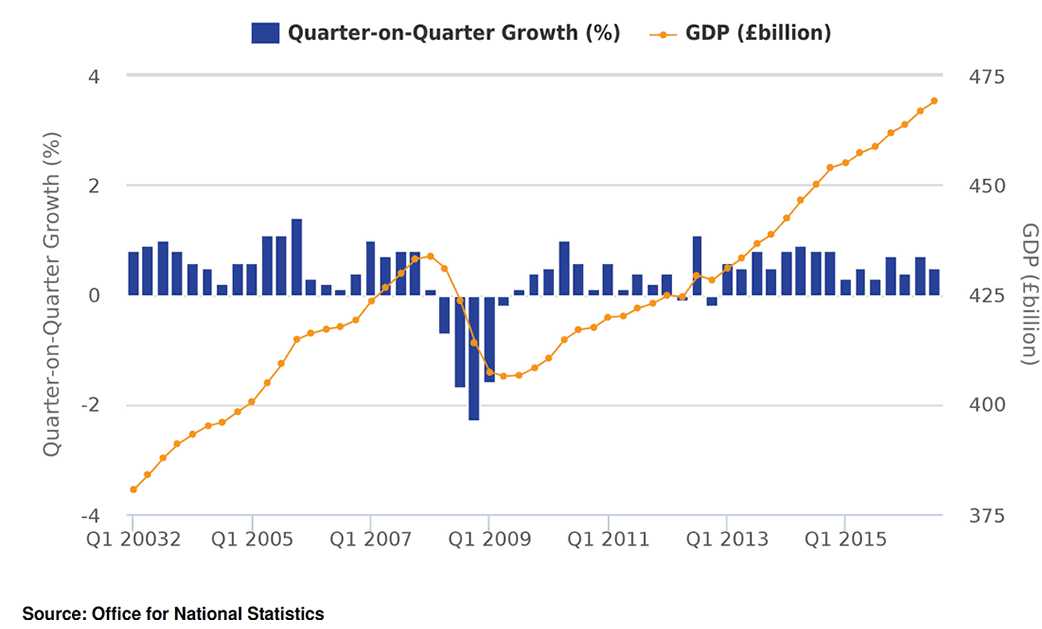

UK GDP growth for the third quarter was confirmed as being unchanged in the ONS’ first review of their initial release.

Annualised GDP remains at 2.3% while quarterly growth is set at 0.5%.

That negative revisions were avoided was enough for Pound Sterling to recapture this week’s gains.

The breakdown of expenditure in the GDP data reveals that consumer spending, which rose by a quarterly 0.7%, accounted for a sizeable part of Q3’s increase.

However, there were positive surprises in that it was revealed the key driver behind the strength in GDP growth was the external sector.

After subtracting 0.8% in Q2, net trade provided a large boost of 0.7%, with exports rising by a quarterly 0.7% while imports fell by 1.5%.

“What’s more, the improvement in survey measures of firms’ export orders suggests that the drop in the Pound should have a greater beneficial effect on exports in time,” says Ruth Gregory at Capital Economics.

As we have noted in our various anecdotal interviews with UK businesses, the weaker Pound really is providing a positive shove for businesses following the EU referendum.

In addition we have found that those businesses that have too long leaned on Sterling’s strength and built their businesses around imports are going to have to rapidly shift strategy to build a more balanced business that derives value from a mix of both imports and exports.

Business Investment Rises

There was another good surprise for the UK economy from the ONS.

Business investment for the third quarter rose 0.9% ahead of expectations for 0.6%, confirming that the vote to leave the EU has not resulted in a sudden drying up of investment.

“The eye-catcher was the rise in business investment to 0.9% on the quarter, further banishment of Britain’s doomsayers,” says Richard de Meo, Managing Director of Foenix Partners.

Capital Economics’ Ruth Gregory agrees that the reading puts paid to worries that referendum uncertainty would dampen spending in the immediate aftermath of the referendum.

“The dark clouds of looming Brexit negotiations are advancing less ominously now and, in surveying the landscape of UK cyclical data, the immediate economic surroundings offer more than a few pockets of optimism,” says Gregory.

Growth will Slow in 2017

Concerning the outlook there remain concerns that UK consumer sentiment could slide should the recent fall in Sterling make its way into prices in a more obvious way.

“The adverse impact of the Pound’s fall – in the form of the upward impact on inflation and corresponding squeeze on real incomes – has not yet been felt,” says Gregory.

But, Capital Economics suspect that importers and retailers will absorb some of the increase in imported costs, ensuring that the squeeze on household incomes is not too intense.

Furthermore, the actual triggering of Article 50 next year could prompt further falls in business sentiment and investment.

Yet with ultra-accommodative monetary policy continuing to support spending and discourage saving, Capital don’t think a sharp slowdown in spending is on the cards.

“So although we expect a bit of a slowdown from Q3’s rate in the quarters ahead, we still think growth will beat expectations and forecast GDP to grow by 1.5% next year,” says Gregory.

This is more or less in line with the Office for Budget Responsibility’s forecasts for growth of 1.4% to be recorded in 2017.

Consensus forecasts from the world's leading economists are for 1.1% growth for next year.

Economists at Barclays are more cautious than peers saying they now expect GDP to edge 0.7% next year.

This is however an upgrade on the 0.5% they previously forecast. Growth for 2018 is forecast at an unchanged 1.5%.

"We continue to believe that the actual triggering of Article 50 and the subsequent drop in sentiment will deliver some negativity in the first half of next year. We also believe that the restrictive fiscal stance of the government, if executed, creates downside risks to overall activity," says Andrzej Szczepaniak at Barclays in London.