When will the US Federal Reserve raise interest rates? Following the release of the latest FOMC minutes, a number of analysts give us their forecasts.

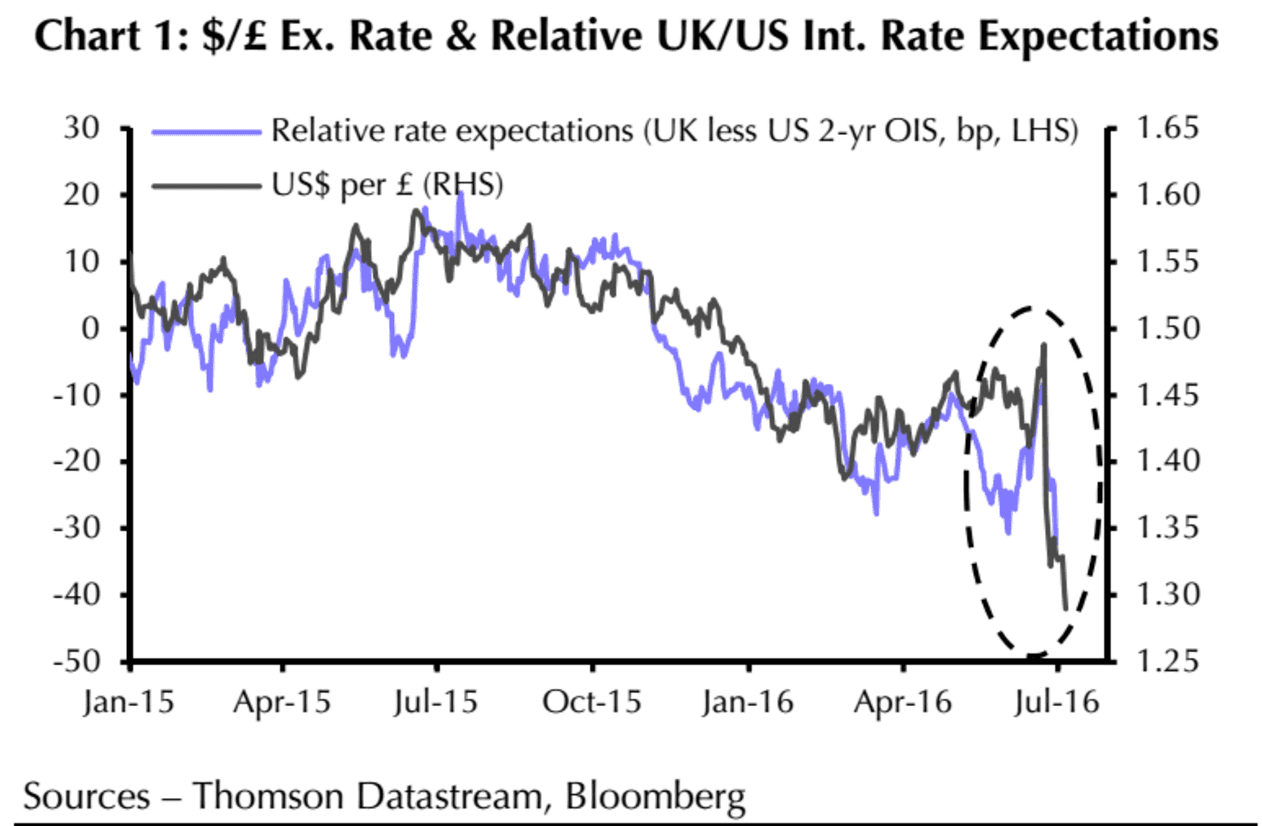

The timing of the next interest rate rise at the US Federal Reserve is incredibly important for the Pound’s outlook in that the GBP/USD exchange rate tends to follow changes in the difference in yield that exists between the US and UK.

As can be seen, the relationship is incredibly well entrenched and will continue to be so:

Therefore, moves on interest rates at the Bank of England and US Federal Reserve are big news.

Minutes from the Fed’s June 14-15th Open Market Committee (FOMC) meeting shows a divided committee, unwilling to commit to rate rises.

Nevertheless, most analysts have chosen to look through the dovishness and expect another rate rise to come.

But when?

Royce Mendes at CIBC Markets writes:

Even though many members apparently believed that the slowdown in the pace of job gains could be temporary, almost all saw the May payroll print as adding to the very uncertain environment.

Keeping in mind that the Brexit vote may have changed some voters' minds, at the time of the meeting many believed that, if growth were to pick up, policy tightening would be warranted.

However, it should be noted that following the UK vote, Fed officials have sounded decidely more dovish in public appearances.

Indeed, even during the meeting, many participants saw the level of the neutral federal funds rate being lower than previous estimates, with the revised summary of economic projections released alongside the statement also showing a lower long-term rate.

As a result, several officials reiterated that considerable uncertainty meant that rate hikes, when they occur, would have to be gradual.

Overall, the minutes are consistent with our forecast for a rate hike around the end of the year, with Brexit related uncertainties likely taking earlier meetings off the table.

Rob Martin at Barclays writes:

Although the minutes adopted a modestly dovish tone, overall, we found them less informative than normal.

In part, the minutes have been overtaken by events — the UK referendum happened; inflation expectations were revised higher. But more importantly, members' views over the near-term outlook for the US economy, whether optimistic or gloomy, will likely be transformed by the near-term evolution of labor markets.

Therefore, learning their views on the outlook at the time of the June meeting is not informative for the near-term path of policy. If the labor market firms (as per our baseline forecast), they are likely to hike in September (our baseline expectation). If the labor market remains soft or deteriorates further, the FOMC will be unlikely to hike in September.

Data dominate FOMC communication, for the moment. In our view, the FOMC would like to hike rates in September; the employment data will determine if they are able to do so.

Paul Mortimer-Lee, at BNP Paribas writes:

The June FOMC minutes were dovish and painted a picture of a divided committee. On one hand some Committee members still expect (or we would say hopes for) progress on employment and inflation toward their mandate and on the other hand there is a growing group of members who are worried about the slowing in employment and the risks to the outlook. We are squarely in the second camp and view the June set of minutes as very supportive of our long-standing high conviction call that the FOMC will keep rates on hold throughout 2016 and 2017.

We continue to think that the US economy is slowing. The Brexit vote was emblematic of the lurking risks on the horizon. In our view, the Committee is becoming more aware of the risks to the outlook and less confident in their forecasts for a Goldilocks outcome.

We remain confident in our view that the Fed will be on hold throughout 2016 and 2017.

Michael S. Hanson, Global & US Economist, Bank of America Merrill Lynch writes:

The June minutes revealed a fair bit of caution by Fed officials — no surprise as the UK referendum loomed a week after the meeting. Voting members thought it “prudent to wait for additional data” on both the vote and the US labor market.

“Most” cited greater uncertainty following recent weak payroll data, yet “many” participants were reluctant to change their outlook on one report.

As a result, the Federal Open Market Committee (FOMC) has returned to a data-dependent, watching-and-waiting mode. We do not expect the Fed to hike before December this year, and they could wait longer.

Yet uncertainty about the long-run neutral funds rate increased in the minutes as well, which contributed to a lower policy path in the dot plot despite few changes to the economic projections.

Our forecast implies a likely further flattening of the dot plot at subsequent FOMC meetings, with just two hikes each in 2017 and 2018 in our base case.

Mikael Olai Milhøj, Senior Analyst at Danske Bank writes:

Little news in the minutes from the June FOMC meeting, which took place just eight days before the UK's EU vote. Most of the information we already got in the FOMC meeting statement and Fed chair Yellen's press conference after the end of the meeting.

With Brexit this is even more true and we think the Fed will 'wait and see' for even longer. Market participants agree that the Fed is on hold for now as markets only price in a fifty-fifty chance of a Fed hike before year-end next year.

Now that we know the UK voted to 'leave' the EU, we have lowered our growth forecasts for the US economy from 1.9% to 1.7% this year and from 2.3% to 1.9% next year.

The reason is that the US economy is not immune to a slowdown in Europe. Hence, we also expect the Fed to be on hold until June 2017 and only to hike twice next year (we expect the following hike in December 2017).

We think the risk to our Fed view is balanced so the next hike could come sooner if the impact of Brexit on the economy is smaller than we currently expect (or later if bigger).

Otherwise, the FOMC mainly discussed how to interpret the mixed data, especially the weak jobs reports. The minutes state that the FOMC ' discussed a range of interpretations of these data '.