Non-farm payrolls (NFP) is currently not critical to the FOMC’s thinking.

Economists argue over the precise amount of slack in the US economy, but most are at least agreed that whatever it is, it is somewhere near full employment.

At this stage then, last month’s surprise dip in non-farm payrolls to 160k is perhaps more consistent with job creation gradually slowing as the labour market reaches this point, rather than anything more concerning.

Anything at or above last month’s figure will be acceptable for the FOMC.

That said, with consensus particularly low (160k), an upward surprise is possible.

Whatever the state of the underlying labour market, the high monthly volatility (created, amongst other things, by statistical/seasonal adjustment gyrations) in NFP makes the risk of a higher reading than last month (160k) much greater than the risk of a lower one.

We look for a reading closer to 200k or above (INGF 210k), consistent with an underlying trend of around 185k.

On this basis though, anything sub-consensus could raise a few question marks for the FOMC doves, who may want to see June’s data before hiking.

Statistical noise could bring the unemployment rate down to 4.9%.

The participation rate fell back last month as a downward correction in the household measure of employment fell much more than unemployment. This kept the unemployment rate at 5% – any retracement of these moves could bring it back to 4.9%.

Ultimately though this is simply statistical noise and thus is probably the least important part of this labour report.

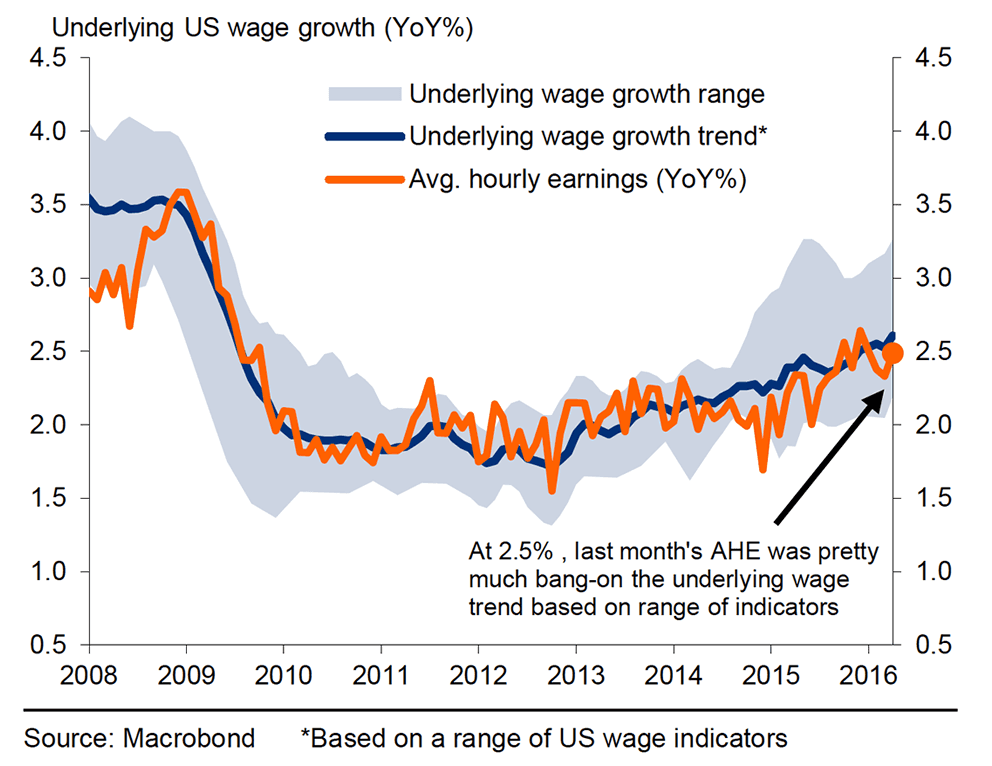

Wage growth is a potential wild card in the June/July debate.

Although average hourly earnings (AHE) notched up to 2.5% YoY last month, it is not yet enough for the FOMC to conclude that tight labour market conditions are putting upward pressure on wages.

Above: Average hourly earnings has caught up with trend.

That said, if AHE sticks around the 2.5% area, it should be sufficient for the next hike.

Indeed, this is the area of the labour market that the Fed is watching the closest and a meaningful positive surprise could (at the margin) secure a few more votes for June over July.

In short, the Fed’s labour market box is already ticked (and arguably has been for several months).

As speeches and statements have shown, the factors constraining the Fed’s normalisation lie outside of the labour market.

With inflation heading in the right direction, activity data has improved slightly after a weak first quarter, with April’s retail sales surge being offset by fairly neutral industrial production (IP) and durable goods data.

Aside from the labour report, only retail sales and IP data will add any extra information before June’s meeting, both of which are unlikely to rock the boat too much.

Barring any negative surprises, the answer to the June/July debate lies with Yellen. Chair Yellen will make a speech next Monday (1630GMT) and will provide the final, and probably definitive, green or red light to a June hike.

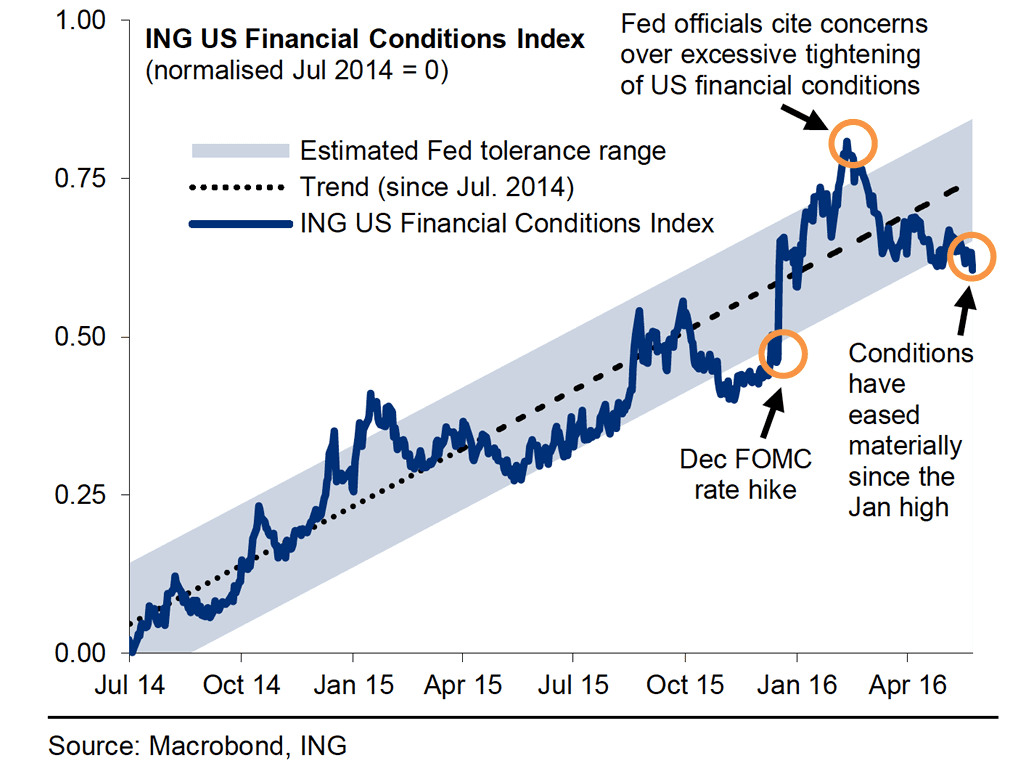

As we noted recently, with financial conditions stable and the data broadly going in the right direction, many on the FOMC may feel that a June hike is justified.

Above: Financial conditions are sufficiently stable for a hike.

But from a risk-management perspective, with the UK’s EU referendum one week after the next meeting, some may want to wait until this known event risk has passed.

Indeed, whilst the economic spill over may be marginal, the immediate effect on US financial conditions could be more noticeable.

With that in mind, the question now facing the FOMC is “would delaying a hike to July be a mistake”. On balance, we think the answer is probably “no”, and therefore think we may be faced with a “phantom rate hike”, where the conditions are right for a June move, but a cautious approach to external risks keeps the FOMC on hold until July.