File image of Chancellor Rachel Reeves. Picture by Kirsty O’Connor / Treasury.

The Chancellor is about to squeeze demand through a sizeable fiscal tightening, which reduces inflationary pressure.

Next week’s UK budget is shaping up to be a decisive moment for monetary policy.

And according to ANZ Research, the measures the government is preparing will push the Bank of England toward cutting interest rates again - starting as soon as December.

✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.

Why? Because the budget is set to be disinflationary.

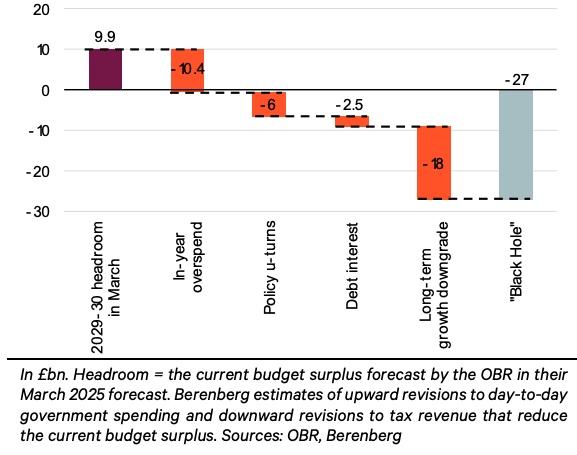

That’s the core message from ANZ, which says the government is "poised to tighten fiscal policy" in its 26 November autumn budget, with the deficit currently running at 5.3% of GDP and the Treasury still committed to achieving a balanced day-to-day budget by FY2029-30.

To meet those fiscal rules, ANZ estimates the Chancellor will need to tighten by 0.4-0.9% of GDP, equivalent to £15-30bn.

The anatomy of a budget black hole. Image courtesy of Berenberg.

And fiscal tightening of that magnitude hits demand.

ANZ says such a stance "will reinforce disinflationary pressures across the economy"; a clear signal that government policy will be pushing inflation down, not up.

That matters for the Bank of England.

The Monetary Policy Committee has been easing cautiously, and ANZ argues this shift in fiscal policy will give it room - and pressure - to go further.

Several elements of the budget backdrop reinforce the case.

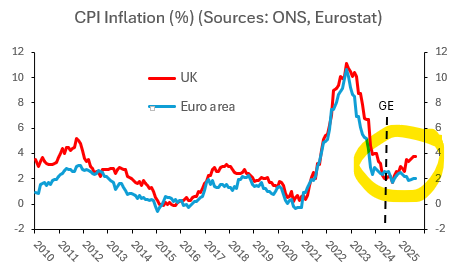

Above: The UK has an inflation problem, with economists blaming the government's generous welfare spending.

First, the UK’s growth environment is already soft.

The report notes that both investment and consumption are "vulnerable to fiscal headwinds," with business surveys pointing to deferred corporate spending and households pulling back due to “elevated inflation, a weak labour market and fiscal uncertainties."

Household savings are still high at 10.8%, signalling caution.

Second, productivity is weakening.

The OBR has admitted its forecasts have been overly optimistic, and productivity fell 0.8% year-on-year in Q2, the sixth straight quarter of decline.

ANZ expects the OBR to cut its productivity assumption by 0.3ppt, which mechanically widens the fiscal hole and forces more tightening.

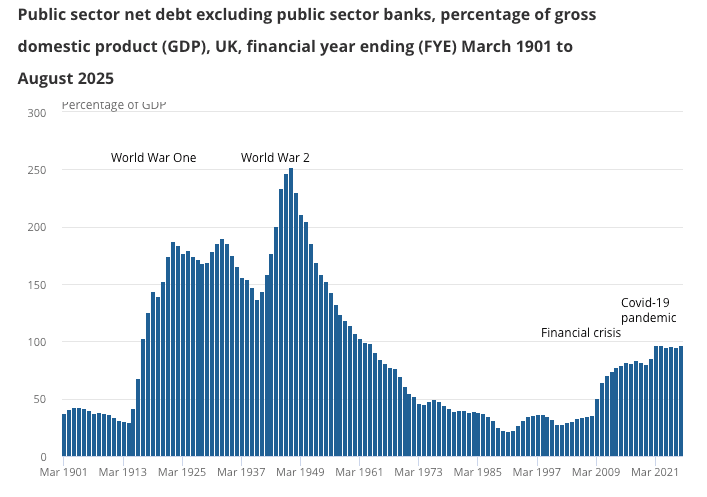

Above: The UK's public debt is at its highest level outside of a world war.

Third, borrowing costs are still elevated.

Term rates have risen because markets are uneasy about the fiscal backdrop and because the BoE’s recent easing has been “cautious,” keeping government financing costs high.

Put together, the budget and the economic environment are pulling in the same direction: weaker demand, slower growth and downward pressure on inflation.

For ANZ, the policy implication is straightforward.

They argue the BoE will need to "fall towards neutral," estimating that neutral sits between 3.3–3.8%. With Bank Rate currently above that range, further cuts are needed to avoid over-tightening the economy.

And the timing is soon.

ANZ forecasts a 25bp cut in December followed by another in Q1 2026, taking Bank Rate to 3.50%.