London, United Kingdom. Chancellor Rachel Reeves during a visit to RAF Northolt in north west London. Treasury. Picture by Kirsty O’Connor / Treasury.

"Fiscal headroom will be rebuilt on 26 March, but it will be a case of running to stand still".

Lloyds Bank have looked at the numbers and thinks Chancellor Rachel Reeves will have to find more money and cut spending in March and then again in the Autumn.

"Fiscal headroom will be rebuilt on 26 March, but it will be a case of running to stand still," says Sam Hill, Head of Market Insights at Lloyds Bank, ahead of the Chancellor's Spring Statement.

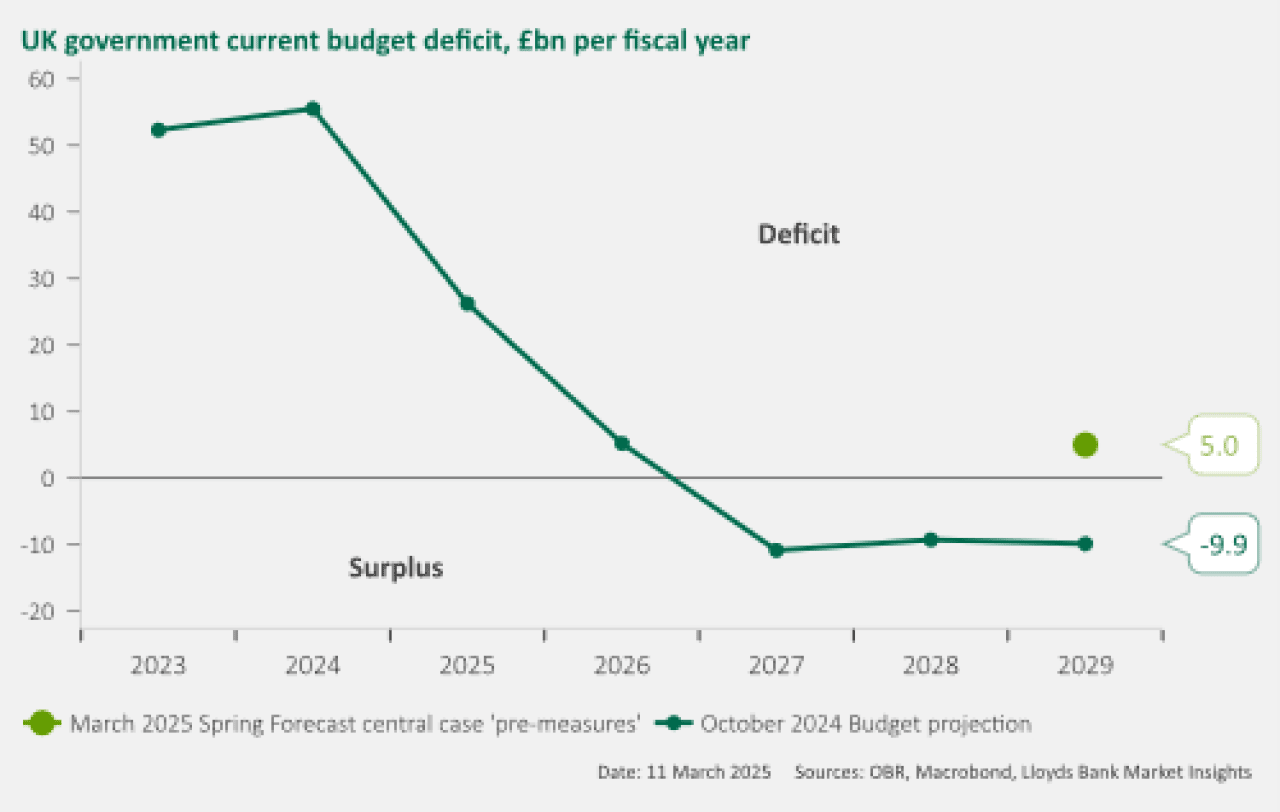

Economists at the UK bank hold a baseline assessment that the impact of the OBR’s macroeconomic forecast refresh will be that the government's £9.9BN of fiscal 'headroom' confirmed in the Autumn budget has disappeared and has evolved into a deficit of approximately £5BN.

Above: Budget deficit and projections.

"Given that the government has been insistent that its fiscal rules are non-negotiable, that means a policy response should be forthcoming," says Hill.

Welfare cuts will be where the majority of March's adjustment falls, with Prime Minister Keir Starmer telling parliament on Wednesday the current benefits system was "unsustainable, it's indefensible."

The OBR estimates that without reform, the UK’s total spending on benefits will rise by more than 25% by 2030.

An ageing population suggests a rise in pension costs, but working-age sickness-related benefits are also expected to increase significantly.

Lloyds Bank thinks the government will announce cuts to spending of about £15BN by 2029-30.

This will return the current budget balance to delivering a projected headroom of ~£10bn.

The UK's fiscal rule requires debt to be falling as a percentage of GDP by 2029-2030.

The government is expected to muddle its way forward, meaning further big decisions await later down the road.

"The political cost for the government of going further could be significant. As such, the UK’s underlying fiscal vulnerabilities aren’t likely to be addressed in a substantial way on this occasion," says Hill.

The government's budget outlook has deteriorated on a combination of lower-than-expected tax takes and higher-than-expected rises in bond yields, which drives up the cost of servicing existing debt.

"It would mean the government continues to be very sensitive to movements in bond yields. In the context of recent volatility not much imagination is required to think that the headroom could be eroded again by an Autumn Budget, requiring yet another reset," says Hill.