Written by Marios Hadjikyriacos, Senior Investment Analyst at XM.com. An original version of this article can be found here.

The storm in US bond markets has evolved into a hurricane, inflicting deep wounds on riskier assets such as stocks.

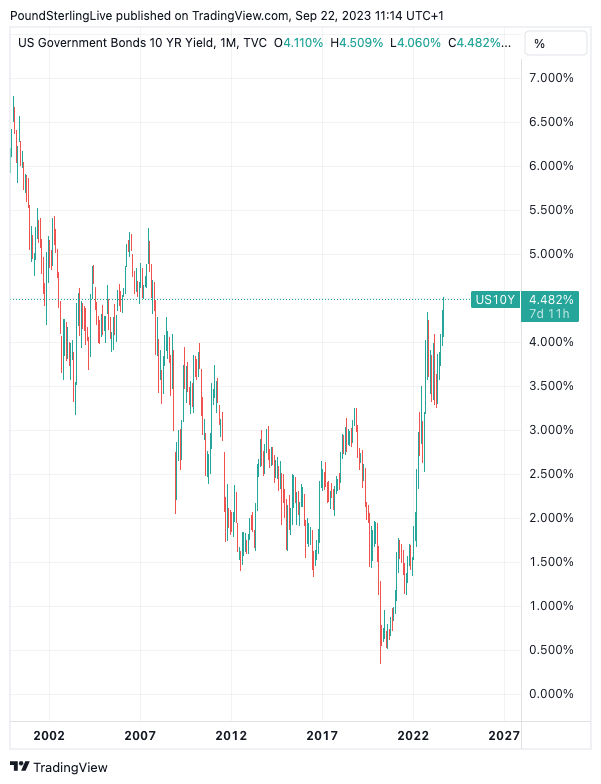

Yields on US government bonds have gone ballistic, with the yield on ten-year notes hitting a fresh cycle high of 4.50% earlier today.

When yields climb with such force, it has repercussions for every other asset class.

Since yields are essentially market-determined interest rates, a move higher incentivizes investors to increase their allocation to cash and decrease their exposure to riskier plays like equities.

This dynamic was on full display yesterday, with the S&P 500 losing 1.6% of its value as yields charged higher.

Above: Yields on U.S. government ten-year bonds haven't been this high since 2007.

Behind this fierce rally in yields lies a mismatch between supply and demand. The Fed raised its rate path this week and incoming US data validated this view, with applications for unemployment benefits falling sharply last week, reaffirming the resilience of the labour market.

Meanwhile, the Treasury continues to flood the market with newly issued debt to finance a gaping budget deficit.

With a deluge of supply set to hit the bond market next quarter while the Fed retains a stance of higher interest rates for longer, the upward pressure on yields could persist.

The striking part is that despite the stunning rally in US yields and the ensuing selloff in stock markets, the dollar did not manage to shine bright.

Yes, the dollar index is headed for a weekly gain, but the scope of the advance has not been impressive considering the seismic moves in bonds.

Euro/dollar is about to close the week almost unchanged, even though rate differentials have clearly moved in the dollar’s favor.

The stabilisation in oil prices may have helped the energy-sensitive euro to gain some footing, alongside some signs that economic activity in Germany has started to bottom out.

The latest business surveys raised hopes that the Eurozone economy might be stabilizing after a severe slowdown, as Germany’s services sector showed signs of life again in September. However, the French readings moved in the wrong direction, keeping a lid on any optimism.

Overall, the PMIs are consistent with a Eurozone economy that contracted in Q3 and the outlook for Q4 is not great either, keeping the risk of a mild recession firmly on the euro’s radar.

In the United Kingdom, the Bank of England shocked traders yesterday by keeping interest rates unchanged, citing slowing economic growth and a loosening labour market. The twist is that the BoE still tightened policy, by accelerating the pace of its quantitative tightening program to £100bn per year from £80bn previously.

The British pound fell sharply after the BoE decision, as the disappointment on interest rates joined forces with the retreat in stock markets to drag the currency lower. In fact, the BoE’s move on quantitative tightening might have amplified the selloff in stocks, coming back like a boomerang to hit the risk-sensitive pound. The pain train for sterling continued to roll on Friday, following some dismal business surveys.

Finally, the Bank of Japan kept its policy settings unchanged earlier today, as widely expected. Markets were searching for any signals about a potential exit from negative interest rates, but Governor Ueda clarified that his previous remarks on this subject were taken out of context, pushing back against such speculation and sinking the yen in the process.