“There is a record of failed attempts to get inflation under control, which only raises the ultimate cost to society of getting it under control, hence the need to do this job now and keep at it,” - Federal Reserve Chairman Jerome Powell

Image © Adobe Images

U.S. inflation has fallen lately but remains far too high for the Federal Reserve and with companies long overlooking its concerns when setting prices, the bank now appears to be reaching for its ‘Feddie Krueger’ mask and so there may be some risk of a Volckerian fright night for global markets on September 21.

Recent falls in U.S. inflation rates have been notable but a busy week of commentary and insights from Federal Reserve officials has made clear, to the author at least, that these price declines were very likely too little and too late for U.S. interest rate setters.

Goods prices have risen significantly in the last year, leading inflation and corporate profit margins higher, but by indulging in this reckless price gouging and consumption it now appears that companies and consumers may have invited upon themselves something like a Volckerian interest rate experience.

For readers' background, Paul Volcker was the Fed Chairman who famously used brutally high interest rates to drive double-digit inflations rates out of the U.S. economy between 1979 and 1989: a turbulent period for global markets.

Above: Price gouging and a red rag to hawkish central bankers. Source: Federal Reserve.

Above: Price gouging and a red rag to hawkish central bankers. Source: Federal Reserve.

This Volckerian experience might involve a steep increase in interest rates on September 21 and the risk of further follow-up actions later on in order to drive down selling prices across the economy using all of the sheer brute force that can be mustered by the Federal Reserve.

That’s the author’s interpretation of this week’s policy commentary from a long list of Fed officials with the latest coming from Chairman Jerome Powell himself at the Cato Institute’s 40th Annual Monetary Conference on Thursday.

“If you look at longer term expectations by households, businesses and forecasters and also markets, you’ll see that they are pretty well anchored around 2%. Of course, short-term expectations are higher because of high current inflation,” Chairman Powell told Cato Institute’s Peter H. Goettler.

“The clock is ticking and as I mentioned the longer that inflation remains well above target, the greater the concern that the public will start to just naturally incorporate higher inflation into its economic decision making and our job is to make sure that doesn’t happen,” he added.

Source: Federal Reserve.

Source: Federal Reserve.

There was a strongly evident common theme in this week’s remarks from Fed officials including from others like Vice Chair Lael Brainard and Cleveland Fed President Lorretta Mester with all of them expressing concerns about an upward drift in shorter-term inflation expectations.

This upward drift in short-term expectations is a dangerous outcome for policymakers and the reason for why was explained in detail by Bank of England (BoE) Monetary Policy Committee member Catherine Mann on Monday.

“We believe that the public’s expectations of inflation will play an important role in the actual path of inflation. So that is kind of the fundamental basis of our framework and as I just discussed, it is very important that inflation expectations remain well anchored,” Chairman Powell said on Thursday.

“There is a record of failed attempts to get inflation under control, which only raises the ultimate cost to society of getting it under control, hence the need to do this job now and keep at it,” he also said at a later point.

Source: Bank of England.

Source: Bank of England.

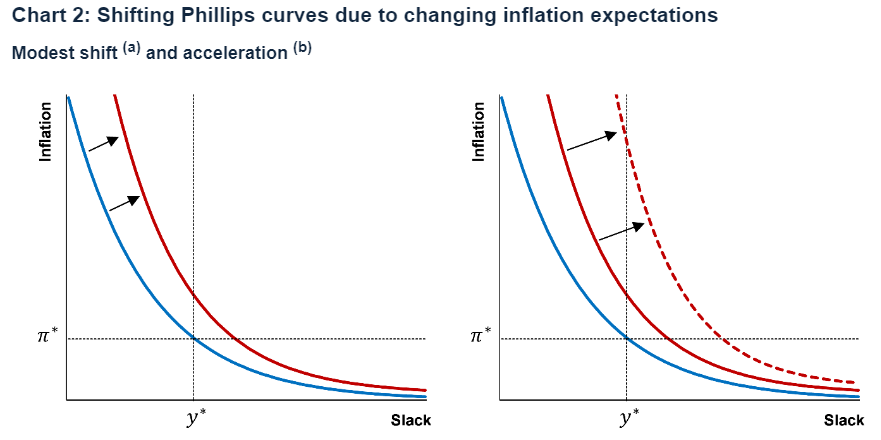

The above chart shows how higher levels of unemployment and lower growth potential can become permanently entrenched in economies if and when any upward drift in short-term inflation expectations is allowed to go unattended to because of the inevitable knock-on implications for longer-term expectations.

Any upward drift in longer-term expectations would inevitably lead to higher levels of interest rates over the longer-term, with these and all of the adverse economic consequences becoming embedded into the economy.

This concern is not unique to the Federal Reserve, however, and has also been voiced by the Bank of England in recent months too.

“Medium-term measures of inflation expectations have drifted up alongside realized inflation, albeit not by as much. This may indicate a worrying shift in trend inflation, e.g. a shift in the Phillips Curve. A drift in medium-term inflation expectations is the development that monetary policy needs to firmly lean against and it should be a key yardstick for whether the MPC’s decisions are effective,” the BoE’s Catherine Mann said on Monday.