“Participants remarked that, although recent declines in gasoline prices would likely help produce lower headline inflation rates in the short term, declines in the prices of oil and some other commodities could not be relied on as providing a basis for sustained lower inflation, as these prices could quickly rebound,” - FOMC minutes.

Image © Adobe Images

Multiple pieces of recent economic data have offered early signs that U.S. inflation pressures may be moderating but minutes of July’s Federal Reserve monetary policy meeting make clear that these are unlikely to keep hawkish Fed officials from lifting interest rates to restrictive levels this year.

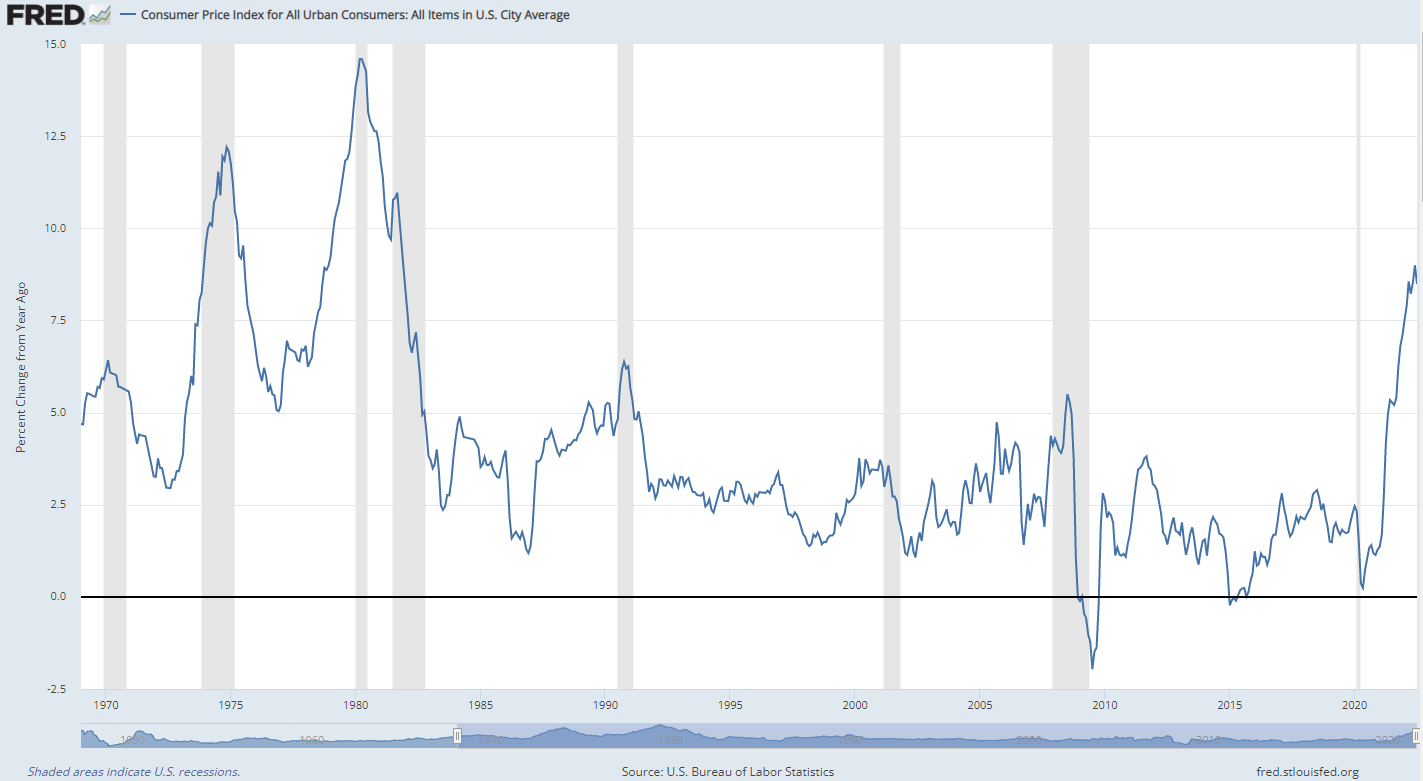

Official measures of U.S. inflation moderated in July and surveys suggested expectations of future inflation had eased while other indicators such as gauges of producer and import prices also ebbed from high levels.

But while cooling demand in parts of the economy played a role, recent falls in commodity prices were far more prominent drivers of those developments and minutes of July’s meeting made clear on Wednesday that Federal Open Market Committee (FOMC) members will leave nothing down to commodities.

“Participants remarked that, although recent declines in gasoline prices would likely help produce lower headline inflation rates in the short term, declines in the prices of oil and some other commodities could not be relied on as providing a basis for sustained lower inflation, as these prices could quickly rebound,” July’s meeting record states in part.

Source: Federal Reserve Bank of St Louis.

Source: Federal Reserve Bank of St Louis.

“Several participants stressed that improvements in supply would be helpful but by themselves could not be relied on to resolve the supply and demand imbalances in the economy sufficiently rapidly. Participants emphasized that a slowing in aggregate demand would play an important role in reducing inflation pressures,” the record states in another part.

The minutes relate to a meeting in which Fed officials voted unanimously for a second consecutive 0.75% increase that lifted the top end of the Fed Funds rate range to 2.5% while collectively reiterating support for a June consensus that borrowing costs will need to rise to as much as 3.5% this year.

That meeting was followed by a press conference in which Fed Chairman Jerome Powell told reporters that FOMC members will be especially attentive to a range of economic barometers as they lift interest rates further and that the pace and magnitude of rate steps could diminish in the months ahead.

“Participants judged that, as the stance of monetary policy tightened further, it likely would become appropriate at some point to slow the pace of policy rate increases while assessing the effects of cumulative policy adjustments on economic activity and inflation. Some participants indicated that, once the policy rate had reached a sufficiently restrictive level, it likely would be appropriate to maintain that level for some time to ensure that inflation was firmly on a path back to 2 percent,” minutes of the meeting stated on Wednesday.

Source: Federal Reserve Bank of St Louis.

Source: Federal Reserve Bank of St Louis.

Dollar exchange rates had already corrected lower from what were in some cases two decade highs ahead of the meeting but continued to fall amid widespread profit-taking following the July decision, although since then the big Dollar correction has stalled and given way to a period of consolidation.

The Dollar's stall likely reflects some of the latest economic data and the most recent remarks from Fed policymakers who’ve roundly warned that they will not be swayed easily from their June plan and current hawkish monetary policy pathway. There was further evidence of this stance in July’s minutes.

“Participants generally judged that the bulk of the effects on real activity had yet to be felt because of lags associated with the transmission of monetary policy, and that while a moderation in economic growth should support a return of inflation to 2 percent, the effects of policy firming on consumer prices were not yet apparent in the data,” minutes of the meeting stated on Wednesday.

“In light of elevated inflation and the upside risks to the outlook for inflation, participants remarked that moving to a restrictive stance of the policy rate in the near term would also be appropriate from a risk-management perspective because it would better position the Committee to raise the policy rate further, to appropriately restrictive levels, if inflation were to run higher than expected,” the minutes also stated.