“If we don’t get inflation back to target then things get worse so we’ve got to get inflation back to target and we will do it,” - BoE Governor Andrew Bailey.

Image © Adobe Stock

The latest remarks and commentary suggest the Monetary Policy Committee at the Bank of England (BoE) is only one inflation number or employment report away from a step change in the pace at which Bank Rate is being lifted, and that any such step change could come as soon as the August policy decision.

Governor Andrew Bailey and Chief Economist Huw Pill are two members of the nine seat Monetary Policy Committee who’ve so far favoured lifting Bank Rate in only standard sized increments of 0.25% but remarks made by them in the last week suggest that their stances may be changing.

This is important because any lean toward larger moves from these two would likely tip the balance on the MPC in favour of exactly that, although it may also be doubly important following the inflation data emerging from the U.S. and interest rate decision coming from the Bank of Canada on Wednesday.

The BoE was one of the first major economy central banks to act when it began lifting Bank Rate in December 2021 and has since raised the benchmark to 1.25%, its highest level since 2008, although all of its five separate rate increases have involved increments of 0.25% or less.

“We think and this has been the case in a number of our recent meeting assessments, we think that inflation should come down rapidly next year as those shocks wear off. Now in the May Monetary Policy Report, however, we said that the risks are on the upside,” Governor Bailey told David Marsh, Chairman of the Official Monetary and Financial Institutions Forum (OMFIF).

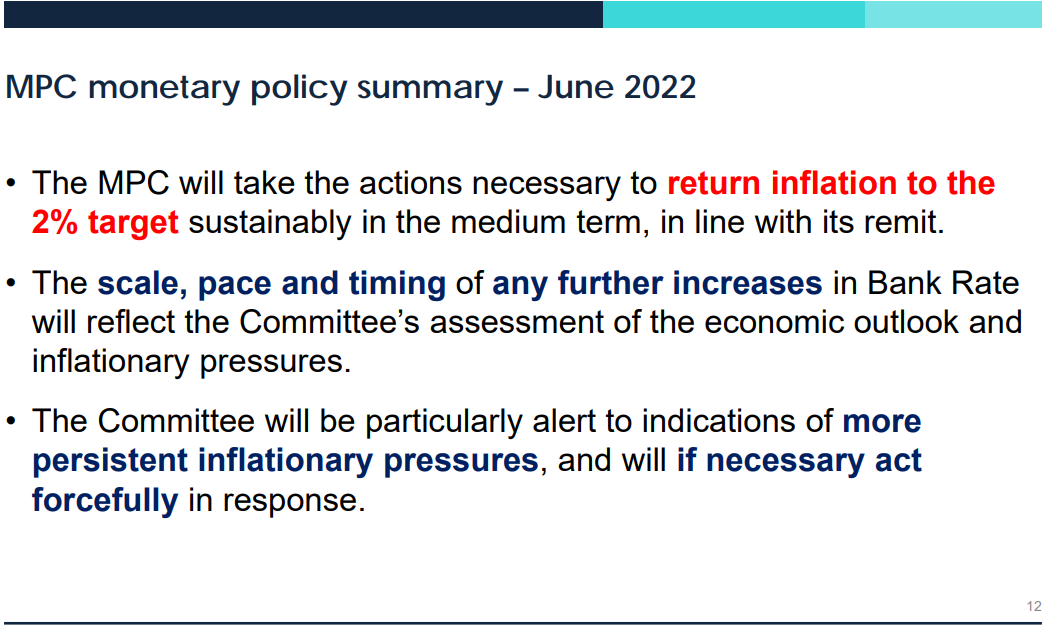

“We use the word forcefully in the last statement deliberately because, clearly, if we see evidence of that persistence we will act forcefully. No question about that. We wanted people to understand that, therefore, there are more options on the table than just 25 basis points and those options can go both ways,” the governor also said in elaboration of his answer on Tuesday this week.

The above remarks were made during a guest lecture about the UK economic landscape following the pandemic and its interaction with the global interest rate environment, which can influence the trend level of real terms interest rates in the UK and other open economies.

Governor Bailey reiterated and staunchly endorsed the stance taken by the BoE last month when telling an audience this week that if domestic prices and wage levels were to be seen rising further in response to a series of imported inflation shocks, then the BoE would have to act more forcefully.

“If we don’t get inflation back to target then things get worse so we’ve got to get inflation back to target and we will do it,” he also said.

His other remarks indicated that wage growth excluding one-off bonuses (more of that data released in July) will be an important influence on the thinking of the BoE in August and likewise with the core measure of inflation for June, which ignores imported energy and food prices.

Source: Bank of England.

Source: Bank of England.

“That’s important because obviously that is distinguishing what I would call the immediate effects of the Russia Ukraine situation, in particular the effect on energy prices,” he said during the Tuesday discussion.

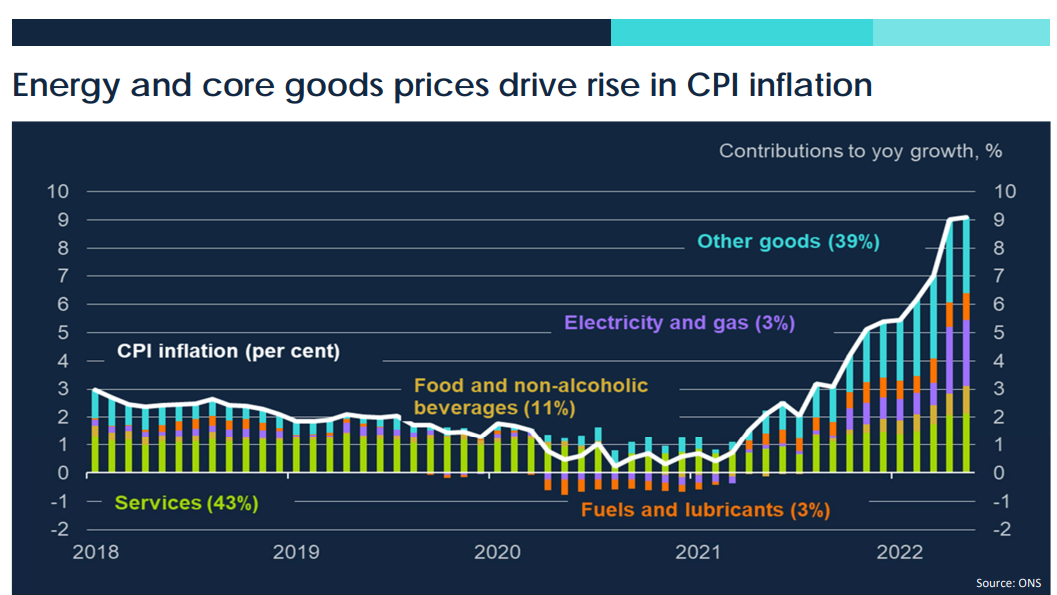

UK inflation edged higher from 9% to 9.1% during May and is forecast by the Bank of England to exceed 11% before the year is out while the rate of core inflation actually edged down from 6.2% to 5.9%.

But exactly that kind of outcome was recently seen over in the U.S. only for Bureau of Labor Statistics figures to then reveal just this Wednesday that the main rate of inflation leapt to a new high of 9.1% in June and that the core rate of inflation accelerated notably in month-on-month terms.

This is especially notable following the remarks from Governor Bailey’and also Huw Pill at the Managing Director’s Club at the University of Sheffield and at the Qatar Centre for Global Banking and Finance Conference last week.

“Recent communication has emphasised the Committee’s preparedness to act forcefully, if necessary, to indications of more persistent inflationary pressures. At least on my part, this statement reflects a willingness – should circumstances require – to adopt a faster pace of tightening than we have seen implemented in this interest rate cycle,” Pill said in part while at the University of Sheffield.

Source: Bank of England.

Source: Bank of England.

“And it flags that the focus of attention will be on indications of more persistent inflationary pressures, which, in my view, places emphasis on potential second-round effects in price and wage setting behaviour. Much remains to be resolved before we vote on our August policy decision. How I vote on that occasion will be determined by the evolution of the data and my interpretation,” he added.

Chief economist Huw Pill argued before the Managing Director’s Club that firms’ and workers’ ongoing attempts to avoid declines in their incomes connected with imported commodity and tradable goods price pressures are at risk of creating a self-sustaining inflation dynamic in the UK that would compel the BoE to act more forcefully with its interest rate. This is his key concern.

“UK price setters and wage bargainers will try to offset the impact of higher headline inflation on their real spending power by seeking higher profit margins or higher wages in order to preserve their real income. Crucially, this threatens to create more persistent inflation dynamics in the UK, which continue even after the original impetus from external sources has dissipated or even reversed,” he said previously at the Qatar Centre.

“It is via such second-round effects that higher current inflation can become embedded in the inflation process and achieve a self-sustaining momentum all of its own. Such behaviour would threaten a more sustained deviation of inflation from target, going beyond the realisation of the shorter-term volatility that I have already mentioned,” he also said in that same address.

Source: Bank of England.

Source: Bank of England.