- Record rise in composite PMI

- Employment bouncing back

- But inflationary pressures at 13 year high

Image © Adobe Stock

The UK economic rebound is well underway according to a survey of UK businesses during March which showed employment was on the rise but so too were inflationary pressures.

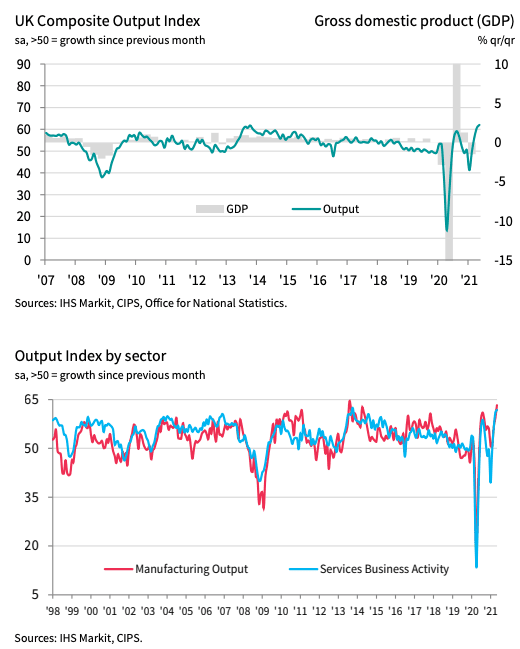

IHS Markit says the rate of expansion was the fastest since the UK Composite Output Index began in January 1998, reflecting strong contributions from both manufacturing and services activity.

The easing of restrictions across the nations of the UK in May meant high levels of pent up demand resulted in a swift turnaround in labour market conditions continued in May with private sector employment rising at the quickest pace since June 2014.

The outcome pointed to a strong rebound in growth but it was ultimately not enough to encourage a more sustained bid in the Pound given it came in largely as the market expected, although the key services sector element of the release disappointed against lofty expectations.

The Services PMI reading for May stood at 61.8 which is slightly less than the 62.2 forecast but above the 61.0 reported in April.

It is important to caution that the survey data will have only covered a few days of the major May 17 Phase 3 reopening in England.

Manufacturing PMI however easily beat expectations at 66.1 (vs 60.8 expected) and was higher than the previous month's 60.9.

Analysts at Capital Economics say there are signs that the manufacturing sector will continue to go from strength to strength as the new orders balance picked up from 54.5 to 61.1 (another record high) and the employment balance increased from 54.5 to 61.1.

Balancing the two readings out to account for their share of the overall economy gives us the Composite PMI which read at 62.0, which is ahead of the 61.9 the market was looking for and the 60.7 reported in April.

Although the headline figures were positive, there were warnings that inflationary pressures were starting to mount.

The PMI survey showed cost pressures were the strongest for nearly thirteen years.

"The CPI measure is likely to increase further later this year, boosted by the temporary cut in VAT for hospitality being partially reversed in September and some pass through from higher commodity prices and the impact of supply bottlenecks," says Martin Beck, Lead UK Economist at Oxford Economics.

Firms reported that efforts to protect margins resulted in the sharpest increase in average prices charged by UK private sector firms since this index began in November 1999.

Looking at the inflationary aspect of the report reveals something interesting that the Bank of England might want to note:

"Manufacturers mostly commented on price pressures due to shortages of raw materials and high shipping costs, while service providers often noted increased staff salaries."

The Bank of England is of the opinion inflation will ultimately prove transitory as global factors - such as fuel costs and supply shortages - will ultimately come to end.

But that staff salaries are increasing is not necessarily in their predictions for inflation.

Rising staff salaries imply a more sustained impact on inflation and this could be something the Bank of England might have to acknowledge if reflected in official data over coming months.

If it is then the market will likely price in a sooner-than-currently-expected Bank of England interest rate rise, which would be bullish for the Pound if the Federal Reserve and European Central Bank sit on their hands.

Analysts at Capital Economics say the PMI data points to the economic recovery shifting through the gears and picking up speed and by their calculations the pace of the rises in GDP should accelerate further from the 2.1% m/m rise in March.

"The lofty levels of the composite PMI in recent months probably has a little further to run as some of the boost from the reopening of indoor hospitality will flow into June. This is encouraging for our view that GDP will return to its February 2020 level by September and suggests there is a chance that it happens sooner," says Kieran Tompkins, Assistant Economist at Capital Economics.