The Pound to Canadian Dollar exchange rate has been consolidating within a fairly narrow range between 1.62 and 1.65 for several weeks now, but now it is starting to show signs of directional activity.

The pair has broken above the consolidation range and is looking bullish.

A move above the 1.6600 level would help confirm a continuation higher, to a target at 1.6800, just beneath the 200-day moving average.

My studies suggest the current move should go to 1.6800 at the very least, as this is the equal to the height of the range extrapolated from the break to the upside, which is the method of forecasting the extent of moves following breakouts.

While we are a little more optimistic on Sterling's prospects against the Canadian Dollar near-term, the bigger picture continues to point to the pair being stuck in a quagmire.

"GBPCAD is stuck," says strategist Shaun Osborne at Scotiabank. "The market has hugged the 1.64 level for the past four weeks and looks poised to continue range trading for a little longer."

Osborne says the drop in volatility is reflected in the sharp contraction in the daily Bollinger bands.

"Often, after a protracted period of low volatility price action, a more dynamic burst of movement follows. Price accelerations can be brutal. We still think 1.6250/1.6550 covers the range for now. And we still think that the GBP needs to break above 1.6620, the early 2017 high, to rally," says the analyst.

Data, Events to Watch for the Canadian Dollar

The week starts with Retail Sales in January on Tuesday, March 21 at 12.30 GMT, which are forecast to show a 1.2% rise year-on-year from -0.5% previously, and a 1.0% increase for Core Retail Sales from -0.3% previously.

Inflation data is out on Friday, March 24 at 12.30, and is forecast to come out at 2.1% year-on-year and 0.9% month-on-month in February.

The Federal Budget on Wednesday, March 22 could cause some volatility depending on the information contained within about the government’s planned infrastructure spending programme. This previously supported the Canadian Dollar after it took the pressure off the Bank of Canada to use monetary easing to stimulate the economy.

Sterling's Rally Built on Sand?

The Pound rallied following the Bank of England’s (BOE) last meeting because the market had not expected such widespread optimism amongst officials.

Kirsten Forbes, for example, voted for a rate hike and other officials voiced similar thought’s judging from the minutes.

“Other members noted that it would take relatively little further upside news on the prospects for activity or inflation for them to consider that a more immediate reduction in policy support might be warranted,” said the meeting minutes.

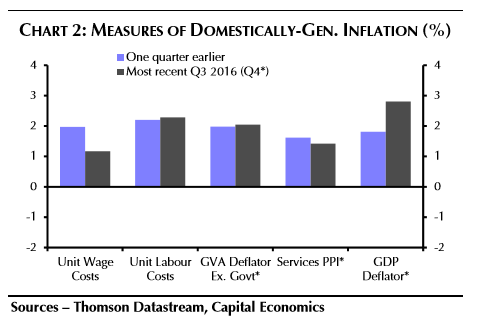

But the BOE’s optimism does not reflect recent data, which has actually shown a slight deterioration over the preceding quarter warns to advisory service Capital Economics.

They note how the Purchasing Manager survey data, for example, is showing a GDP growth of only around 0.4% in Q1 against BOE forecasts of 0.6%.

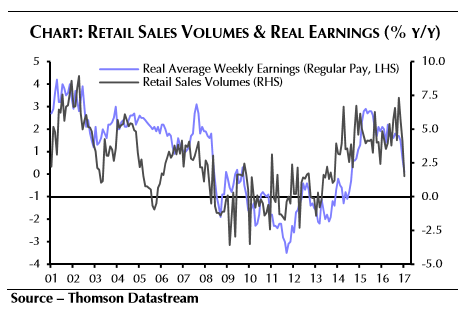

Retail sales have also slowed.

“Early hard evidence such as the surprise dip in retail sales volumes in January, adds to the view that the near-term risks to the MPC’s activity forecasts may be skewed to the downside,” says economist Paul Hollingsworth at Capital Economics.

The imminent triggering of article 50 will officially kick-start the UK's exit of the European Union and usher in a period of uncertainty which is likely to impact on economic growth.

Sterling’s current rally may therefore be built on sand.

The Week Ahead for the Pound: Inflation Data will be Key

As far as upcoming data releases go, the main release for the Pound is the February CPI due for release on Tuesday, March 21 at 9.30 GMT.

Market expectations for a rise to 1.8% are a little low according to both Capital Economics and TD Securities, who estimate a higher 2.1% and 2.2% rise year-on-year in Feb.

The main contributory factors are likely to be rising food inflation due to the weak Pound and the lagged effect of the rebound in oil prices.

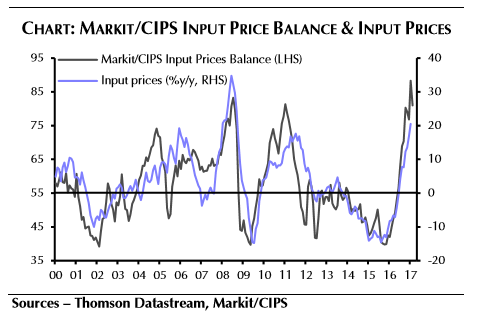

Producer Prices in the UK, out at the same time are expected to show continued extremely high yearly gains in ‘Input prices’ due to the rise in imported component prices because of the weak Pound.

Capital expect Input prices to rise by 21.7% year-on-year.

Manufacturers are not passing the higher costs on, however, as output prices are only rising at a fraction of the level, of 3.5% currently, rising to 3.8% according to Capital.

“Meanwhile, the survey evidence suggests firms have been taking a hit to their margins. Indeed, the output prices balance of the Markit/CIPS survey has not risen by nearly as much as the input price balance. As such, we expect output prices to have increased only a little further, from 3.5% to 3.8%.,” said Holingsworth.

On Tuesday, March 21 at 9.30 Public Borrowing data is released and should show a small 1.0bn rise in February.

Nevertheless, borrowing remains below previous forecasts – down 22% on the previous year allowing the public finances some breathing room.

Given the government’s U-turn on increasing National Insurance contributions from the self-employed and lower-than-expected borrowing, the government does now have a buffer it can use to stimulate the economy in case of a Brexit-related slowdown, factors Sterling’s current rebound may be based on.

The final big news release for the Pound is Retail Sales at 9.30 on Thursday, March 23.

“February’s retail sales figures are likely to suggest that consumer spending is on track for a disappointing first quarter,” said Capital’s Hollingsworth.

He further notes this appears to be as a result of a correlated fall in real earnings growth.

The consensus market estimate is for sales to have risen by 0.4% month-on-month and 2.6% year-on-year, whilst Capital are slightly more optimistic seeing 0.5% and 2.7% rises respectively.

Notwithstanding this slightly brighter forecast the remain pessimistic about the outlook for Retail Sales in Q1.