Image © Adobe Stock

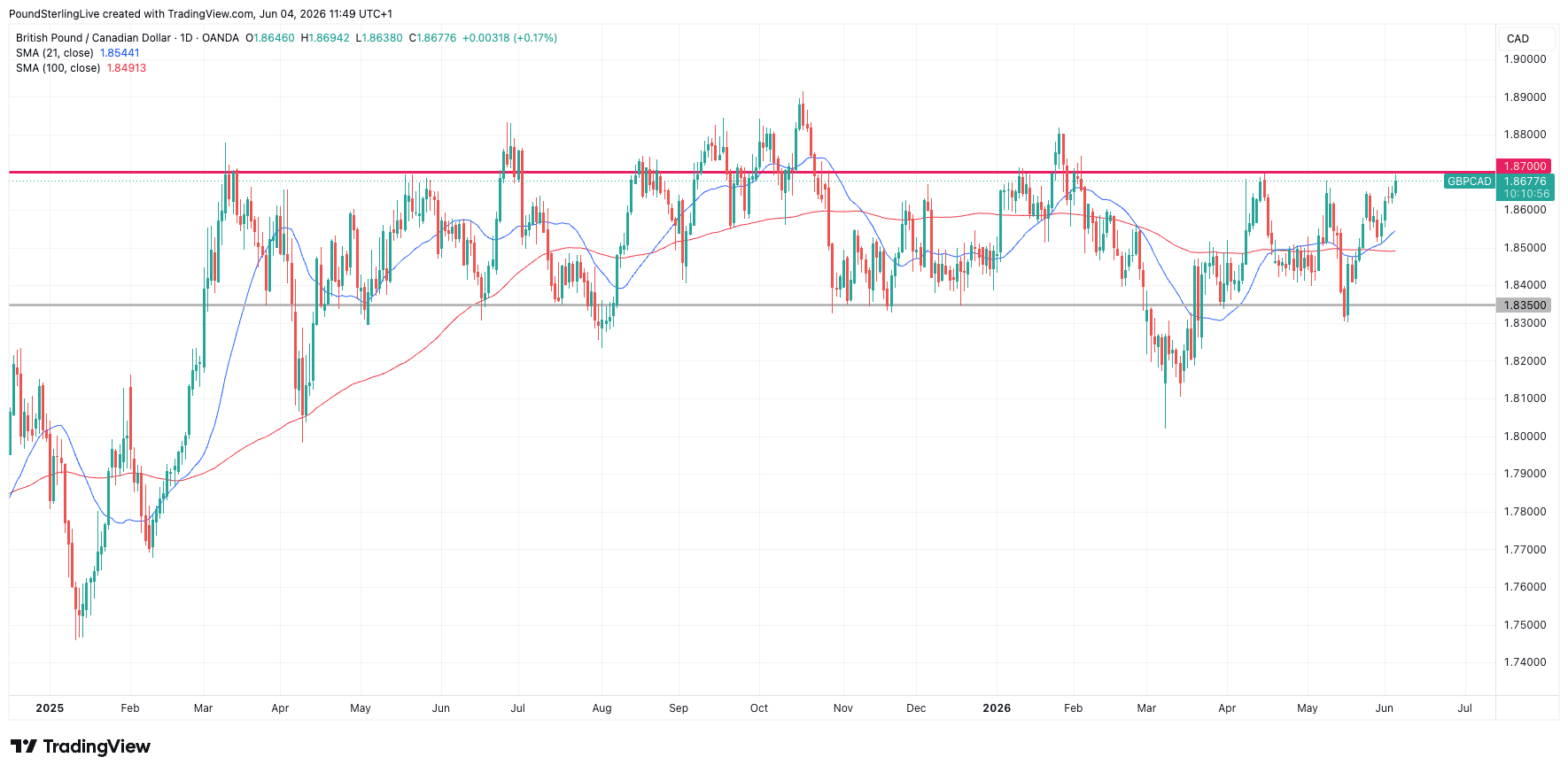

GBP/CAD likely to fall back to 1.8490.

The Canadian dollar is outperforming G10 peers ahead of the weekend after the economy added far more jobs than was expected in May.

87,800 new positions were filled in May said Statistics Canada, dropping the unemployment rate to 6.6%. Consensus estimates had pointed to 10K, marking a sizeable beat that would inevitably alter Canadian bond yields and the currency.

The headline figure is supportive of the view that the Bank of Canada can consider raising interest rates again should future inflation prints reveal upside persistence.

However, pushing back against that notion that the Bank needs to act was another set of data showing the average hourly wage for permanent employees fell sharply to 3.2% from a year earlier, down from 4.8% in the prior month.

That might signal to the Bank of Canada that there's still some slack in the economy that must be filled before wages start rising and pressuring inflation.

It's an observation that could help the CAD's post-jobs advance.

It is also important to consider that even after this stonking report, the six-month average for employment is still slightly negative (-2K). This means the Canadian economy is coming out of a noticeably soft patch, and raising rates could seem premature.

Nevertheless, on the day, the Loonie holds the advantage: the pound to Canadian dollar exchange rate had risen to 1.87 earlier in the day but has fallen back post-jobs.

This is technically significant as 1.87 forms the top of a range that stretches all the way back into early 2025 and marks a limit that traders dare not pursue, confirming a major technical rejection has occurred.

The inevitable consequence of the failure is a retreat back into the range, with the flat 100-day moving average, now at 1.8490, likely to attract sellers.

Above: 1.87 has been the start of a mighty barrier that has contained GBP/CAD upside since March last year.