Image © Bank of Canada, Reproduced Under CC Licensing

- GBP/CAD spot at time of writing: 1.7613

- Bank transfer rates (indicative): 1.6997-7120

- FX specialist rates (indicative): 1.7349-1.7454 >> Get your quote now

The Pound-Canadian Dollar rate was eyeing the top of a multi-month range Wednesday after the Bank of Canada (BoC) expanded its maiden quantitative easing programme and set out plans to buy up to 40% of treasury bills sold at auction in what could amount to partial 'monetisation' of the budget deficit.

Governor Stephen Poloz said in his final scheduled annoucement that the coronavirus-driven economic contraction is so unprecedented the Bank of Canada is not providing updated economic forecasts this quarter.

Poloz said BoC analysis indicates a 1-3 percent fall in the first quarter GDP but did not release the regular quarterly forecast pack, although Statistics Canada had said beforehand the economy likely shrank by -9% in March and that this indicates a -2.6% contraction in GDP for the first quarter.

"The sudden halt in global activity will be followed by regional recoveries at different times, depending on the duration and severity of the outbreak in each region. This means that the global economic recovery, when it comes, could be protracted and uneven. The Canadian economy was in a solid position ahead of the COVID-19 outbreak, but has since been hit by widespread shutdowns and lower oil prices," Poloz says. "All the Bank’s actions are aimed at helping to bridge the current period of containment and create the conditions for a sustainable recovery and achievement of the inflation target over time."

This was after leaving the cash rate unchanged at its new record low of 0.25%, which is down from 1.75% in January, and expanding the quantitative easing programme that was only launched just more than a fortnight ago.

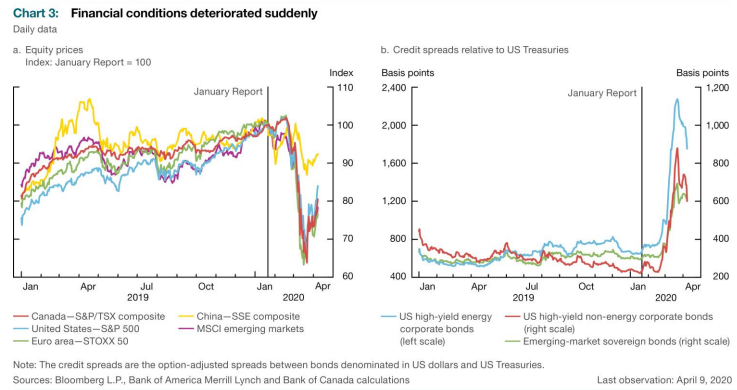

Above: BoC slide showing falls in major stock markets (left) and increase in corporate financing costs (right).

The BoC is now launching a "Provincial Bond Purchase Program of up to $50 billion" and a new "a new Corporate Bond Purchase Program" in which it will buy C$10bn of 'investment grade' corporate bonds.

"The Bank of Canada is justifiably reaching deeper into its tool kit to keep the economy’s pieces in place so that they can be reassembled when the worst of the viral hit has past," says Avery Shenfeld, chief economist at CIBC Capital Markets. "These actions will help narrow spreads for issuers other than the federal government, and thereby transmit more of the impact of low sovereign rates across the economy."

New programs will subject medium and long-term provincial bond yields as well as some corporate yields to the same treatment meted out to money market notes of provincial governments as well as to federal government yields from across the 'curve' or maturity spectrum. But the most notable was a declaration the BoC will now buy up to 40% of the Bills sold at government auctions.

"These programs are meant to help absorb some of the increase in bond supply that will stem from significant government and corporate borrowing, and to ensure these markets continue to function well. Once again, Governor Poloz distinguished that market functioning goal from the more traditional QE aim of pushing longer-term interest rates lower," says Josh Nye, a senior economist at RBC Capital Markets. "Today's rate announcement was the last before Governor Poloz's term ends on June 2, though with unscheduled announcements having been the norm in recent weeks, this might not be the last we see of him."

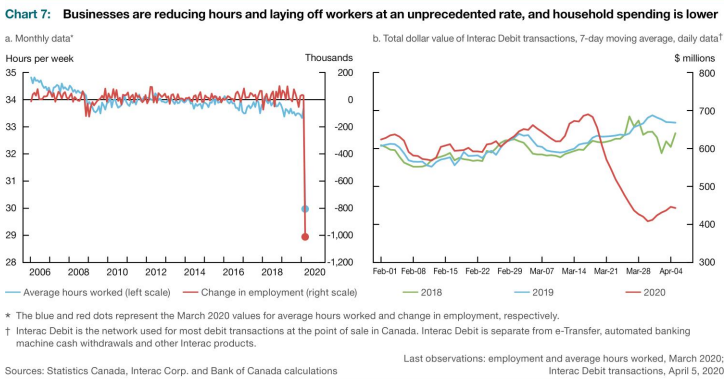

Above: BoC slide showing change in hours worked by sampled employees (left) and credit card transactions (right).

The bill program is the BoC offering to give the government close to half of the short-term finance it might need at any point as it seeks to shepherd the country and economy through the coronavirus shutdown.

It could be described as the partial 'monetisation' or financing of the government budget deficit, a controversial thing in some parts of the market but one arguably made necessary by the extraordinary coronavirus-induced financial needs of all governments, not to mention recent bond market price action.

Canadian 10-year yields rose from 0.30% to 1.05% between March 09 and March 18 despite the BoC cutting the cash rate from 1.25% to 0.75% in that time, denoting capital flight from a supposedly safe-haven market and indicating a preference for hard cash or cash equivalents among investors.

Above: USD/CAD rate shown at daily intervals alongside 2 and 10-year (black line) Canadian government bond yields.

Flighty money and bond markets are why HM Treasury asked the Bank of England for an unlimited overdraft just last week and could explain the BoC buying more Canadian Treasury Bills. "This will provide a short-term source of additional liquidity to the government if needed to smooth its cashflows and support the orderly functioning of markets," the BoE said at the time.

"The monetary policy report illustrates two divergent scenarios, both quite weak in the near term, but showing a difference of about a year in terms of getting back to the prerecession trend level of output," CIBC's Shenfeld says. "Fresh action today, after only starting QE a couple of weeks ago, suggests that it is following Governor Poloz’s earlier analogy, that nobody would criticize a firefighter for throwing two much water on the flames. We agree."

10 and 2-year yields extended earlier sharp falls in response to the announcement and took the Loonie down with them, enabling the Pound-Canadian Dollar rate to swing into the black for the session after having trodden water through much of it beforehand.

Above: Pound-Canadian Dollar rate shown at daily intervals.

Sterling was testing the 1.76 level against the Loonie in Wednesday trade although the exchange rate has previously met tough resistance at the nearby 1.78 handle and stronger pushback from 1.80.

USD/CAD retreated from session highs in response to the BoC's announcement, which came alongside a series of U.S. economic numbers and at the tailend of a European session where the greenback had been bid sharply higher across the board amid renewed risk aversion among investors.

"We are not certain that the GBP can break out of the range at this point but we think the technical stars are aligning to suggest that the GBP could retest strong resistance around 1.78 again—the range ceiling in effect. We continue to think the GBP is a buy on dips," says Juan Manuel Herrera, a strategist at Scotiabank. "USDCAD retains a soft undertone and shorter term trend signals are aligned bearishly, if weakly, for USDCAD. The run lower in funds may be running near to its full course for now, however."