Image © Stockyme, Adobe Stock

- GBP/CAD seen as vulnerable to weakness

- Knocking on range ceiling, forecast to drop

- Brexit news to determine Pound; Canadian Dollar looks to oil data

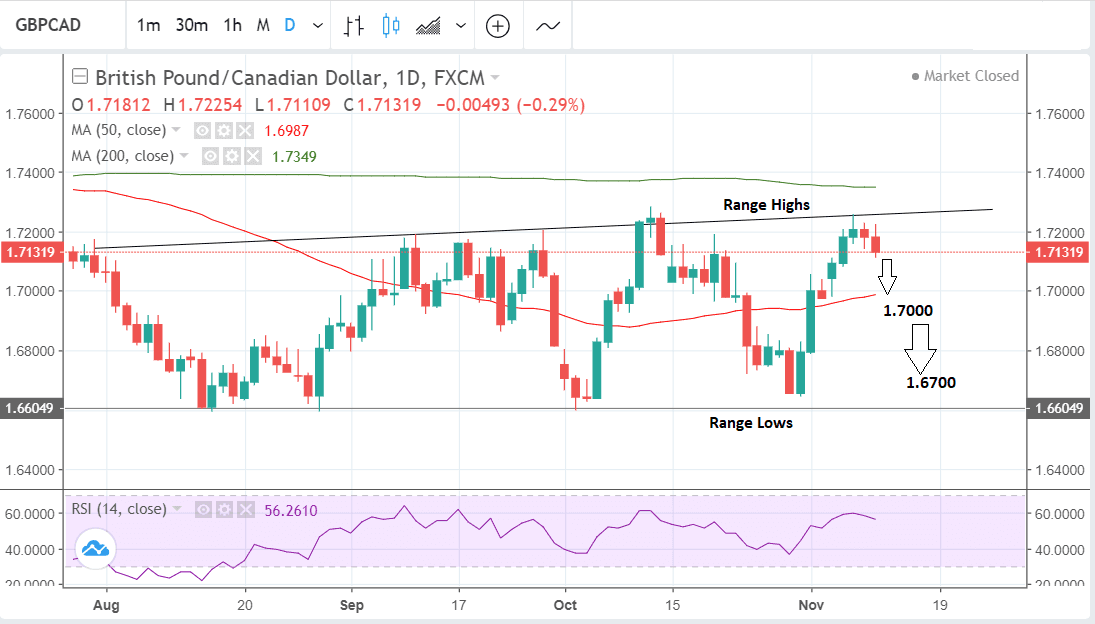

The Pound-to-Canadian Dollar exchange rate is trading within a relatively narrow range between a 1.6600 floor and 1.7250 ceiling.

The GBP/CAD pair has just reached the upper boundary of that range and it will either breakout higher or fall back down within the range, we think it is more likely that it will fall back down.

Since the trend is effectively sideways our base case scenario is to expect it to continue in the week ahead, and a fall back down within the range is now probable, with the next downside target at the 1.7000 level just above the 50-day moving average MA. A move below Friday's 1.7110 lows would provide the necessary confirmation - but we expect that to occur pretty rapidly after the open.

A further break below 1.6900 would probably confirm an extension down to a target at around the 1.66-67 range lows.

Although the last two days of trading activity were bearish there is still not enough concrete evidence from price action alone to indicate the short-term trend has rotated lower.

A third down day in a row, however, will provide a much stronger bearish signal, and this is more likely to materialise than not, given the fundamental headwinds faced by Sterling at the start of the week ahead.

The news that the EU has rejected Theresa May's latest backstop proposal is likely to propel further losses for the Pound. If the high hopes of a Brexit deal which propelled the currency higher are unwound, Sterling will probably crash in all its pairs including GBP/CAD.

There is a lot of oil-related data in next week's calendar and this will also probably influence the pair since the Canadian Dollar is sensitive to fluctuations in the price of crude. The oil price is currently in a downtrend which is negative for the Canadian Dollar (and therefore positive for GBP/CAD).

Advertisement

Bank-beating GBP/CAD exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

The Canadian Dollar: What to Watch this Week

It is a quiet week for the Canadian Dollar from a domestic data perspective, but, as already mentioned, it is a busy week for crude oil data, and this will probably impact on CAD, assuming it impacts on the price of oil.

Canada is a major oil exporter and therefore the price of crude - particularly Western Canada Select crude - impacts on the country's foreign exchange earnings. While brent and WTI crude have enjoyed elevated prices, Canadian crude has struggled, hence we continue to look for a pick-up in prices right across the crude sector that might drag CAD higher in sympathy.

The OPEC monthly oil report is out on Tuesday, November 13 at 11.15 GMT, and is likely to contain key insights into the oil market's supply and demand balance which could impact the price of oil.

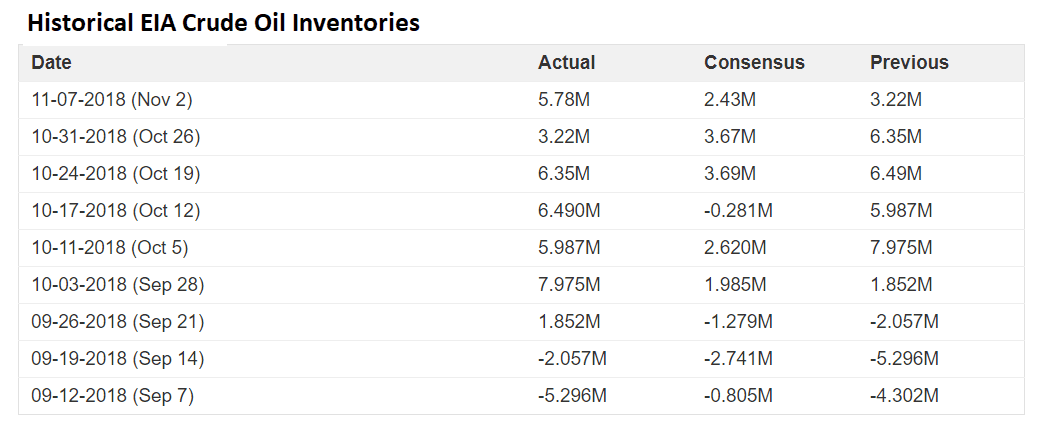

Crude Oil inventories in the U.S. are published by the Energy Information Agency (EIA) on Wednesday at 15.30 and if they show a rise then it is generally taken as negative for the oil price as it is indicative of increased supply; if inventories fall it suggests demand is outstripping supply which is positive for the price of oil - and also CAD.

Image courtesy of fxstreet.com.

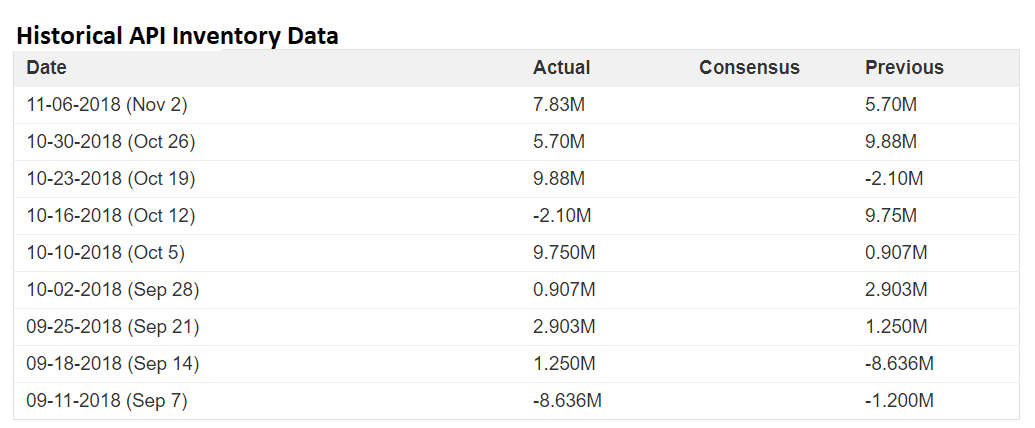

The American Petroleum Institute's (API) inventories are released on Wednesday at 21.30. This is different to EIA data as it records refined - not crude - fuel stocks. API is negatively correlated to oil prices and the Canadian Dollar, as is the case with the EIA data.

Image courtesy of fxstreet.com.

The Pound: What to Watch this Week

The main driver of the Pound in the week ahead is likely to be Brexit news.

If it looks like a withdrawal deal is on the table the Pound will rise, and vice-versa if the opposite.

The headlines from the Sunday Times are indeed worrying: if true then it might be the case that Theresa May will have to walk away from negotiations as she simply won't be able to muster parliamentary support for a wildly unpopular deal that risks the U.K. being subjugated to E.U. law indefinitely.

Yet, we always knew these negotiations would go down to the wire and with December being the final deadline we are not surprised by these negative headlines.

Markets could be accused of becoming far too optimistic on the state of Brexit negotiations of late. The E.U. always negotiates until the very end; and we are seeing just this.

That is also possible gains on any deal may be short-lived as even if the government announces a deal it will still have to get approval from Parliament, and this could be an arduous process, presenting a risk to Sterling.

The conservative government only has a small majority and is reliant on support from the DUP and every single one of it MPs, so there is a risk that if either the DUP or Brexit rebels vote against the deal Theresa May may find she does not have the majority to push it through, and this could weigh on the Pound.

On the hard data front, one of the most significant releases in the week ahead is likely to be inflation data for October, which, according to the market consensus, is forecast to show a 0.2% rise on a month-on-month (mom) basis and 2.5% rise on a year-on-year (yoy) basis (for headline inflation) when it is released on Wednesday at 9.30 GMT.

A result in line with expectations would probably be bullish for Sterling as higher inflation puts pressure on the central bank to raise interest rates which appreciates the currency.

This is because higher interest rates tend to attract more inflows of foreign capital drawn by the promise of higher returns.

There is a chance, however, that inflation will disappoint because of the waning influence of the cheap Pound which has appreciated on Brexit hopes. Headline CPI has already fallen from a peak of 3.0% in January due to the bounce in the Pound, so more losses are possible - although if comments from the Bank of England (BOE) are anything to go by unlikely.

"In its most recent meeting, the Bank of England (BoE) noted that it does not expect inflation to fall much further, with price growth instead holding fairly steady near the 2% target," say Wells Fargo in a note to clients.

Another major release for the Pound is labour market data out on Tuesday at 9.30. Probably of most significance to Sterling is the average earnings component because of its influence on inflation. The current expectation is for a rise of 3.0% in Earnings (including bonuses) and for a rise of 3.1% in earnings excluding bonuses. A result in line with expectations could be positive for the Pound as it will reflect an even stronger rise in real earnings since the fall in inflation from its January peak.

Other results of note within the labour report are unemployment, which is forecast to remain at 3.0% and employment change which is forecast to rise by 34k.

The final major release for the Pound is retail sales on Thursday, which is forecast to show a 0.2% rebound in October, from a rather weak -0.8% previously, and a 2.8% rise yoy from 3.0% previously, when it released at 9.30 GMT.

Advertisement

Bank-beating GBP/CAD exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here