- AUD trade surplus surprises on upside for February and March.

- Exports to China and Japan return to record levels during March.

- May 15 wage price index is key to the AUD outlook from here.

© Taras Vyshnya, Adobe Stock

The Australian Dollar rose during the Thursday session on data which showed a surprise increase in the Australian trade surplus during the month of March and a substantial upgrade to February's number.

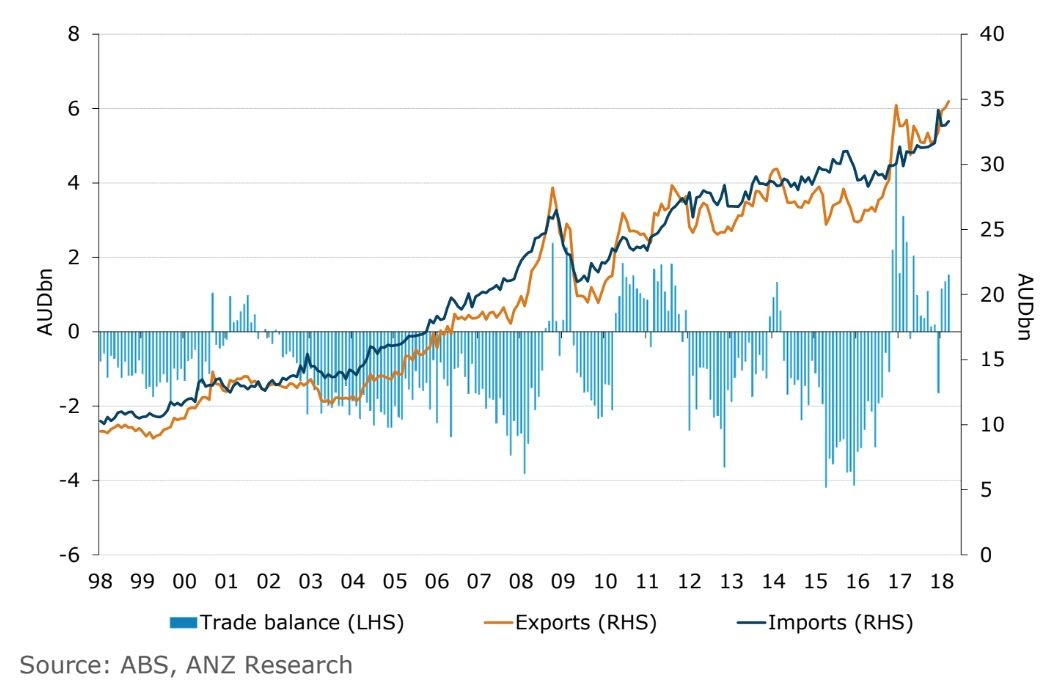

Australia's trade surplus rose to $1.53 billion in March, up from $1.35 billion in February, when markets had expected it to decline to $0.68 billion. This was after February's $865 million surplus was revised higher to $1.35 billion at the same time.

The balance of trade is key as a currency tends to enjoy fundamental support when exports exceed imports, all else being equal.

The increase in the surplus came as Australian exports rose at a faster pace than imports, suggesting global demand for Aussie goods remains robust.

"Australia's trade surplus with China (annualised) is on par with the 2013 record of $A40b, followed by Japan at nearly $A30b. For perspective, in the absence of trade with China and Japan, Australia's current account deficit would be closer to -5.5% of GDP," says Annette Beacher, chief Asia Pacific macro strategist at TD Securities.

As it stands, the Australian current account deficit was just -2.2% of GDP during the first quarter, thanks to a surge in Chinese and Japanese demand for Aussie goods.

As can be seen in the below, it is rare by historic standards for Australia to deliver a trade surplus:

"With a full quarter of trade data now published, net exports look set to provide a solid contribution to Q1 GDP, after being a significant drag in the second half of 2017," says Jack Chamers, Economist with ANZ Bank.

Separately, the Australian Bureau of Statistics also said that building approvals rose by 2.6% during March, partially reversing a -4.2% slump from back in February, which also surprised the market. Economists had been looking for growth of just 1.1% in the number of new construction projects approved during the month.

Both of these sets of statistics are relevant to the Aussie Dollar as they are leading indicators of demand within the economy, which is itself important for the inflation outlook. And it is inflation that matters most for the Reserve Bank of Australia and its interest rate policy in that, without a pick up in consumer price pressures, Aussie interest rates will not be going anywhere fast.

Above: AUD/USD rate shown at hourly intervals.

The AUD/USD rate was 0.50% higher at 0.7523 during the morning session in London as a result, while the Pound-to-Australian-Dollar rate was 0.46% lower at 1.8042. The Aussie unit was also quoted higher against all other developed world currencies.

Above: Pound-to-Australian-Dollar rate shown at hourly intervals.

Where Next for the AUD?

The Australian Dollar was crushed beneath the weight of unfavourable interest rate differentials during the April month as markets refocused on relative returns at a time when US and other global bond yields were rising, just as the Reserve Bank of Australia signalled it is comfortable sitting on its hands for the foreseeable future.

Australian interest rates have been held at a record low of 1.5% for approaching two year now and, at the time of writing, markets do not expect a change in RBA policy until well into the 2019 year. However, the Federal Reserve has raised interest rates six times in the last three years and American bond yields now sit above those of their Aussie counterparts.

"The AUD has proved vulnerable to the rise in short term US rates – which the RBA acknowledge have risen for reasons other than a rise in Fed Funds. We acknowledge that AUD will face a tough week from upside risks to US rates, but the local AUD story doesn’t look that bleak. 0.7500 remains key AUD/$ support," writes Chris Turner, global head of FX strategy at ING Group, in a note this week.

What's more, the direction of travel for other central banks and bond yields is also opposite to that seen down-under, with the Bank of Canada firmly entrenched in an interest rate hiking cycle while the Bank of England and European Central Bank are also in the process of withdrawing stimulus from their respective economies.

This means that, in a world where currency markets are focused on relative interest rates, the Aussie Dollar is at risk of being shunned by investors in favour alternatives where either rates are already higher, or where the direction of travel is more positive. The only thing that will prevent this from happening is signs of a change in the RBA policy stance.

The Reserve Bank will release its latest statement on monetary policy at 02:30 am Friday, which will provide more detailed insight into the most recent deliberations over the economic and interest rate outlook down-under.

There is also scope for markets to become more optimistic about Australian interest rates later this month, on May 15, when the first quarter wage price index is released. Wage growth can have a significant influence over demand in an economy and so it is also important for inflation and interest rate expectations.

However, the last set of figures were a disappointment as they showed pay growth driven entirely by one-off changes in public sector pay and the minimum wage. It remains to be seen whether 2018 will bring the long-awaited turn for the better in Australian household finances.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.