- GBP/AUD downtrend intact and to endure despite waning momentum.

- As AUD- CNH correlation gone into reverse so can't save GBP/AUD.

- Technical and other considerations may lift GBP/AUD in coming days.

- But macro tables are turning on GBP/AUD and risking -14% downside.

Image © Adobe Images

- GBP/AUD spot at time of writing: 1.8543

- Bank transfer rates (indicative): 1.7894-1.8024

- FX specialist rates (indicative): 1.8265-1.8376 >> Get your quote now

The Pound-to-Australian Dollar rate downtrend has waned this week but remains intact while the underperforming British currency is unlikely to be spared from further losses by Chinese aggression toward Australia and a rise in USD/CNH due to the now-broken relationship between these currencies.

Sterling was lower against many rivals during the final session of the week as "month-end flows" helped paint a mixed picture in the major currency sphere. Australia's Dollar was higher against half the major bucket including the U.S. Dollar and Sterling, but flagging ahead of an eagerly-awaited press conference from President Donald Trump where details of a pending response to China's actions in Hong Kong are expected.

Meanwhile, the U.S. Dollar was down against all major rivals in what some have previously described as a "buy the rumour and sell the fact" response to the absence of meaningful action from President Donald Trump on Hong Kong. However, stock markets were mostly lower and some commodity prices higher, producing very much a mixed bag and murky illustration of the mood in global financial markets that might speak more to a lack of consensus.

But crucially for the Pound-to-Australian Dollar rate, the antipodean has bitten its thumb at Beijing and Sterling has underperformed.

"The Chinese Communist Party might not be saying so much following their conference in Beijing. But higher iron ore prices and falling Shanghai metals inventories indicate a degree of business confidence that comes with stimulus spending," says John Meyer, head of research at SP Angel, an independent investment bank with a specialism in resources. "Prices are set for a record monthly advance driven by supply worries form Brazil and robust demand from China. Most-active futures have jumped 22% in May as the world's second largest producer Brazil has been hit badly by the Covid-19 pandemic which has led to Vale cutting its annual shipment guidance."

Above: GBP/AUD eyes 78.6% Fibonacci retracement of Aug 2019 trend as momentum wanedes and RSI plateaus.

Sterling's fall against the Aussie has paused this week and with it the relative-strength-index measure of momentum has flattened out, confirming last week's warning from quantitative strategists at BofA Global Research who said the trend is waning and that there's now a medium risk of reversal based upon studies of pricing in the options market and other factors. Relative price action in AUD/USD and GBP/USD is what drives the GBP/AUD exchange rate so the market's appetite for Aussie Dollars and the general mood among investors, which is important for the U.S. Dollar, are important influences on the outlook.

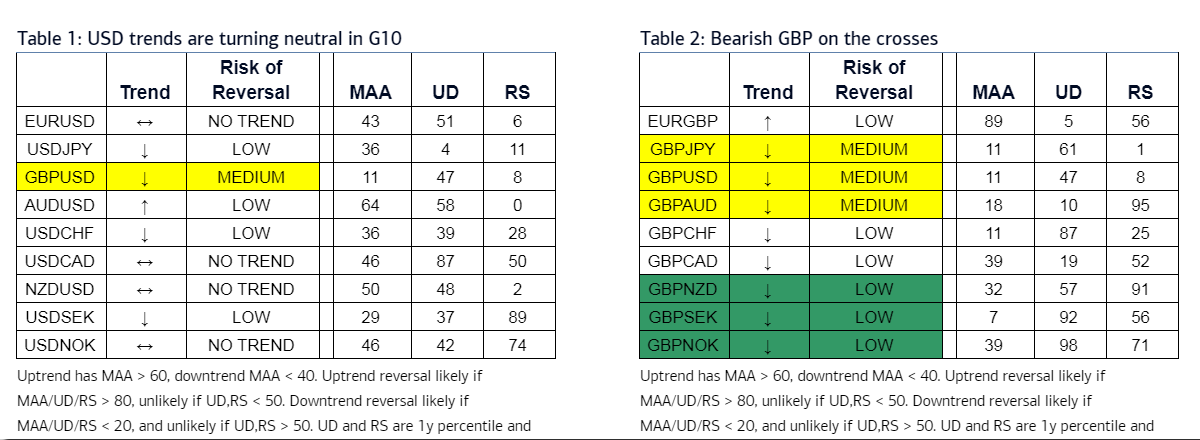

"Our quant models are overall bearish GBP on the crosses. While USD trends have started to moderate and slow down, GBP is sliding lower against all pairs in G10. GBP/NZD, GBP/SEK and GBP/NOK downtrends are robust, according to bearish Up/Down vol and Residual Skew for puts," says Vadim Iarolov, a quantitative strategist at BofA Global Research.

Australia's Dollar has been one of the better performers in the major currency space this month while the greenback sits in the middle of the rankings and Pound Sterling firmly at the bottom. These trends were also confirmed by Iaralov and the BofA team. But the AUD/USD rate was knocking on the door of its 200-day moving average Friday as well as the 100% Fibonacci retracement of its March downtrend, which means it might not go much further in the short-term. Meanwhile, GBP/USD has become more resistant to the downside this week and if such behaviour continues alongside an AUD/USD stall the Pound-to-Aussie rate would bounce from Friday's levels.

Above: BofA Global Research graph detailing quantitative studies of exchange rates and trend scores. Click to enlarge.

"Geopolitical risks up, but global equities were mixed-to-higher (Stoxx-50 +0.4%, Hang Seng -0.7%). XAU rallied 0.8%... The BBDXY traded flat. On most axes, we would not look to add to USD longs until the Index closes back above 1,240.00," says Stephen Gallo, European head of FX strategy at BMO Capital Markets. "Michael Saunders was quoted as saying it would be better to ease "too much" rather than "too little". This is another flagrantly dovish BoE remark in what was already a long list of dovishness. Fiscal policy won't begin to prop up the GBP and offset the BoE story for some time."

The Pound-to-Australian Dollar rate may well bounce in the days and weeks ahead but the market view on Sterling has become decidedly bearish, which suggests that any gains might be limited, more so given the Aussie's relative appeal to investors. Sterling has fallen more than 4% against the Aussie this month as the Bank of England (BoE) sat on Sterling and Brexit headwinds returned to haunt the British currency. This was on days when it wasn't in retreat from a rapidly recovering Aussie, which has been lifted by a sharp rebound in commodity prices and stock markets as well as a swift end from the Reserve Bank of Australia (RBA) to its interventions in the local bond market.

Australia's Dollar is a commodity currency while Sterling is on the letterhead of a jolly big banking sector, which could partly explain GBP/AUD's performance in May because the month marked the beginning of a still-tentative global economic recovery. This is the point where equity market strategists would normally say something like "commodity stocks tend to outperform early in the cycle while banking stocks only really begin to come alive late cycle."

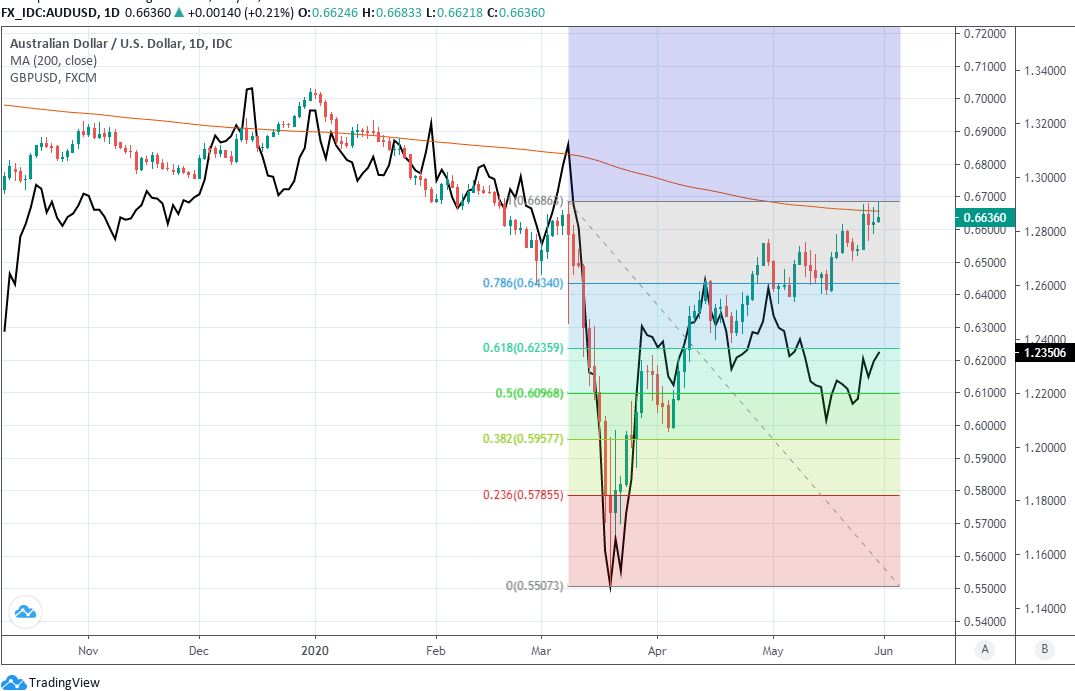

Above: AUD/USD with Fibonacci retracements of March downtrend, 200-day average and GBP/USD (black line).

There are other factors that also explain the performance of the Pound-to-Aussie rate including relative stability in Australian bond yields, which the RBA has managed to anchor mostly between 0.25% and 0.30% in the two-to-three year sector of the yield curve. Meanwhile, two-year British bond yields fell more than -50% Friday, pushing deeper below the zero level as the market feels the full weight of the BoE bearing down on its shoulders.

That widening and Aussie-favourable yield differential very much reflects the contrast between the financial positions of the UK and Australian governments that would feature prominently in the considerations of investors up ahead. Nonetheless, and irrespective of the cause, readers who have Australian Dollar liabilities may not be able to count on Chinese aggression toward Australia or the slump in the currency of the world's second largest economy to save the Pound-to-Australian Dollar rate.

The relationship between AUD/USD and USD/CNH has broken down this year and with it, the GBP/AUD and USD/CNH correlation has also gone into reverse. This coincided closely with the end-March and early April period in which the Federal Reserve (Fed) fired an unprecedented number of U.S. Dollars into the financial system, and the breakdown has endured since the coronavirus went into retreat in the major economies.

Above: AUD/USD alongside USD/CNH. Both have a positive correlation post-coronavirus rather than negative.

China has attacked Australia repeatedly over its calls for an investigation into the origins of the coronavirus but the Aussie has so-far bitten its thumb at Beijing whereas before the virus, the antipodean currency might've been left reeling. That correlation shift and the early cycle economic recovery are supportive factors for the Australian Dollar, while BoE monetary policy and a looming Brexit showdown between the UK and EU are net-negatives for Sterling.

Put differently, the macroeconomic tables are turning against the Pound-to-Australian Dollar rate and at a point when its still above the midpoint of its post-referendum range and a downtrend is in play. This is an exchange rate that traded near 1.60 after the Brexit referendum - darker days for the Aussie too - and not long after the last occasion that the weekly relative-strength-index broke beneath its Friday level. Sterling was at 1.86 against the Aussie Friday, with a -14% difference between there and 1.60.

One important reality for Aussie Dollar buyers is the above rates would only be available at interbank level if realised, with those quoted to retail and SME participants likely much lower. Some high street banks were already quoting below 1.80 on Friday. Specialist payments firms can help squash the spread between interbank and retail rates as well as lock-in the rates prevailing at any one time up to two years in advance of the relevant transaction.

Friday's rates and any improvements seen in the days ahead really might be as good as they get for those who've got Sterling-Aussie-Dollar liabilities, and for a while to come too. A Brexit and BoE pile-on that comes as investors are beginning to chase a global economic recovery narrative would imply very, very steep downside for the Pound-to-Australian Dollar rate that does its greatest damage at the intersection of Sterling weakness and Australian Dollar strength.

Above: GBP/AUD nearing mid-point of post-referendum range.