- ZAR rally stalls as USD finds its feet at U.S. open

- But holds gains over all major DM, EM currencies

- Unfazed by SARB’s patient approach to rate rises

- Tame inflation averts rate rises until final quarter

- Economic forecasts upgraded on quicker recovery

Image © SARB

- GBP/ZAR reference rates at publication:

- Spot: 20.11

- Bank transfer rates (indicative guide): 19.41-19.55

- Transfer specialist rates (indicative): 19.93-20.01

- Get a specialist rate quote, here

- Set up an exchange rate alert, here

The Rand appeared unfazed when the South African Reserve Bank (SARB) reiterated that it intends to be patient before raising South African interest rates.

South Africa’s Rand retained intraday gains over all major developed and emerging market currencies on Thursday when a steadying U.S. Dollar appeared to stall a global rally in risky currencies, although USD/ZAR and GBP/ZAR remained close to the week’s lows.

There was little if any sign of the Rand being fazed when the South African Reserve Bank’s quarterly projection model reiterated its prescription from July, which suggests a 0.25% increase to the cash rate from 3.5% to 3.75% could be necessary in the final quarter.

Then as now the bank’s model suggested that a sole 2021 rate rise be followed by a further 0.25% increase to the cash rate in each of the next eight quarters out until 2024 in order to ensure South African inflation rates remain within the 3%-to-6% target band.

“We expect the economy to grow by an upwardly revised 5.3% this year (from 4.2%), despite the much larger negative effect on output than was previously estimated from the July unrest,” the SARB said in its September statement.

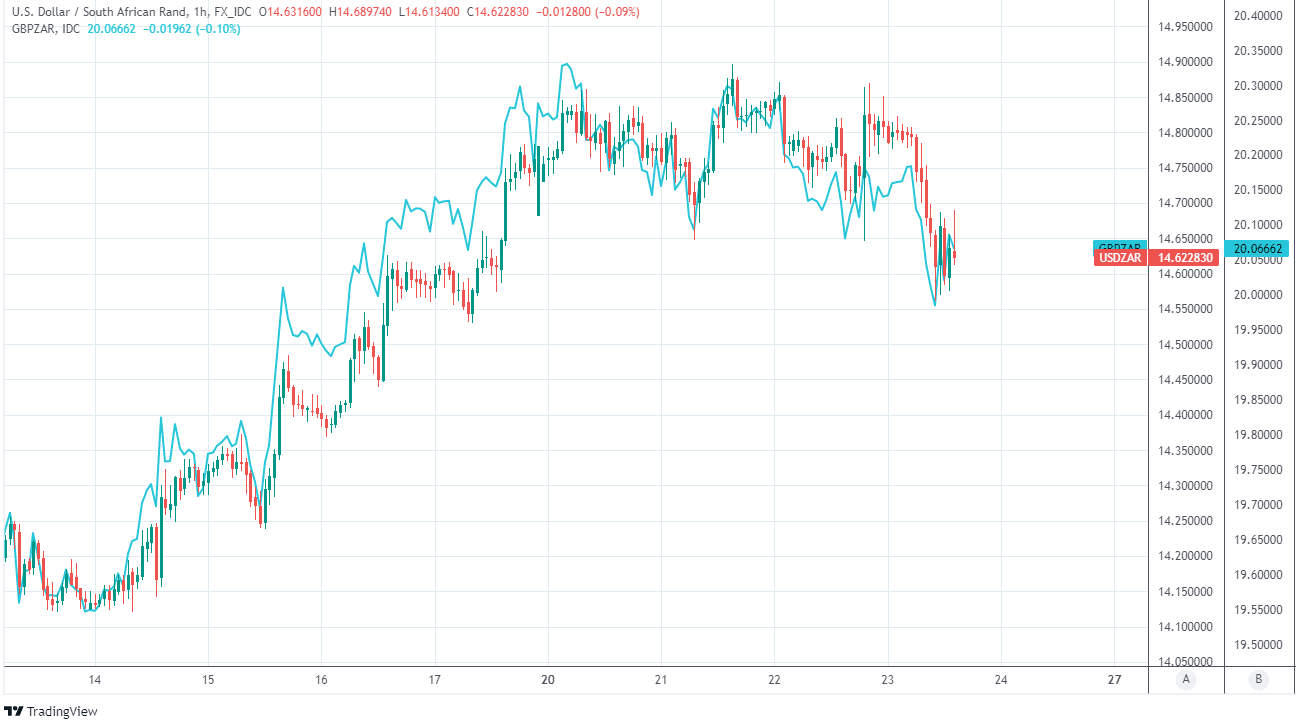

Above: USD/ZAR and GBP/ZAR shown at hourly intervals.

“The faster vaccine rollout presents upside risks to the growth outlook. The current account surplus remains large, at 5.6% of GDP, reflecting high prices for mining and agricultural exports, still gradually rising oil prices, and slowly reviving demand for imported consumer and investment goods. The surplus is expected to shrink to about 0.7% of GDP for next year (2022), as exports slow and imports accelerate,” the statement later said.

SARB policymakers upgraded their forecast for 2021 GDP growth sharply on Thursday following a stronger-than-anticipated performance in the second quarter, although they crimped modestly their earlier projections for 2022 and 2023, leaving them at 1.7% and 1.8% respectively.

Meanwhile, the 2021 inflation forecast was lifted from 4.3% to 4.4%, although projections for 2022 and 2023 were left unchanged at 4.2% and 4.5% respectively.

The outlook for core inflation - which overlooks volatile energy and food prices - was similarly little changed with projections for 2021, 2022 and 2023 coming in at 3%, 3.8% and 4.3% respectively.

“In our view, the prospects of a full economic recovery in South Africa remain bleak, and there is a long list of reasons why the SARB should hold rates. In line with this, we continue to expect no rate hikes this year,” says Cristian Maggio, head of emerging market strategy at TD Securities.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

The SARB’s updated inflation forecasts are one reason why the bank is unlikely to raise interest rates before the final quarter, and could even see the South African cash rate left unchanged until some time in the New Year.

It’s inflation that central banks are seeking to manage, within the context of a predefined target, when they tinker with interest rates and the SARB’s projections suggest that South African price pressures will remain tamed around the midpoint of the three-to-six percent target over the coming years.

Statistics South Africa data for August provided little if any argument against the SARB’s outlook this Wednesday when it showed the main inflation rate edging higher to 4.9% last month while the more important core inflation rate crept up from 3% to 3.1%.

Low core inflation suggests, if anything, that price pressures were simply not very prominent within the collection of risks still faced by the South African economy this summer, and could yet give the bank’s quarterly projection model cause to further delay its prescribed date of lift-off for interest rates.

“Risks to inflation do seem to be more to the upside, but when considering the details of inflation, it is clear that consumer demand remains constrained, leaving space for the SARB to keep its monetary policy settings at current levels,” says Siobhan Redford, an economist at Rand Merchant Bank, in a note ahead of Thursday’s release.

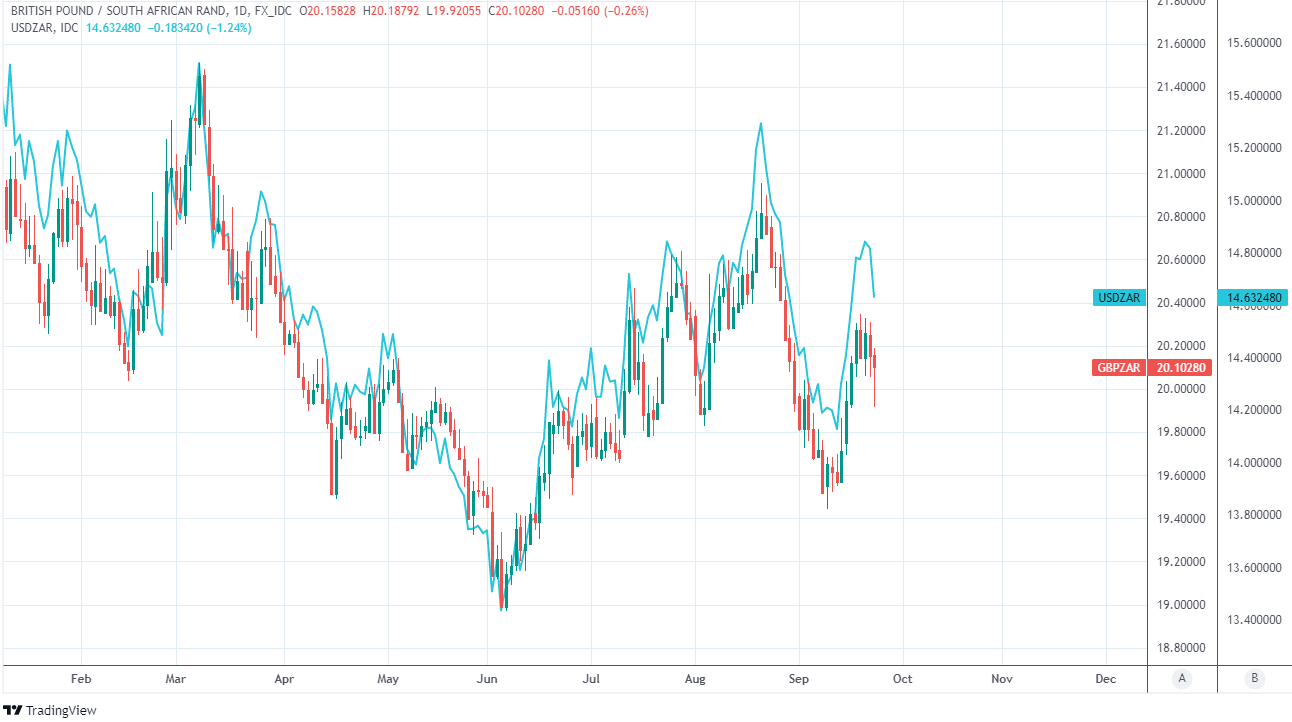

Above: GBP/ZAR and USD/ZAR shown at daily intervals.