Image © Adobe Images

The yen is expected to weaken further against the dollar despite repeated intervention efforts by Japanese authorities, according to new analysis from RBC Capital Markets.

A new analysis from the investment bank says deteriorating fundamentals will continue to outweigh official attempts to stabilise the currency.

RBC has revised its dollar-yen forecasts sharply higher on growing concern that Japan’s macro backdrop has become increasingly hostile for the currency.

"High energy costs continue to weigh on the yen," RBC strategist Abbas Keshvani wrote, adding that Bank of Japan quantitative tightening and fiscal concerns have also “injected volatility into the JGB market, scaring asset managers."

Japan is a net energy importer and the elevated cost of oil and gas stemming from the Middle East war will hurt its current account dynamics.

RBC estimates Japan's net energy import cost could widen to $15BN per month, assuming Brent crude rises to $110 per barrel, up from roughly $11BN before the latest conflict escalation.

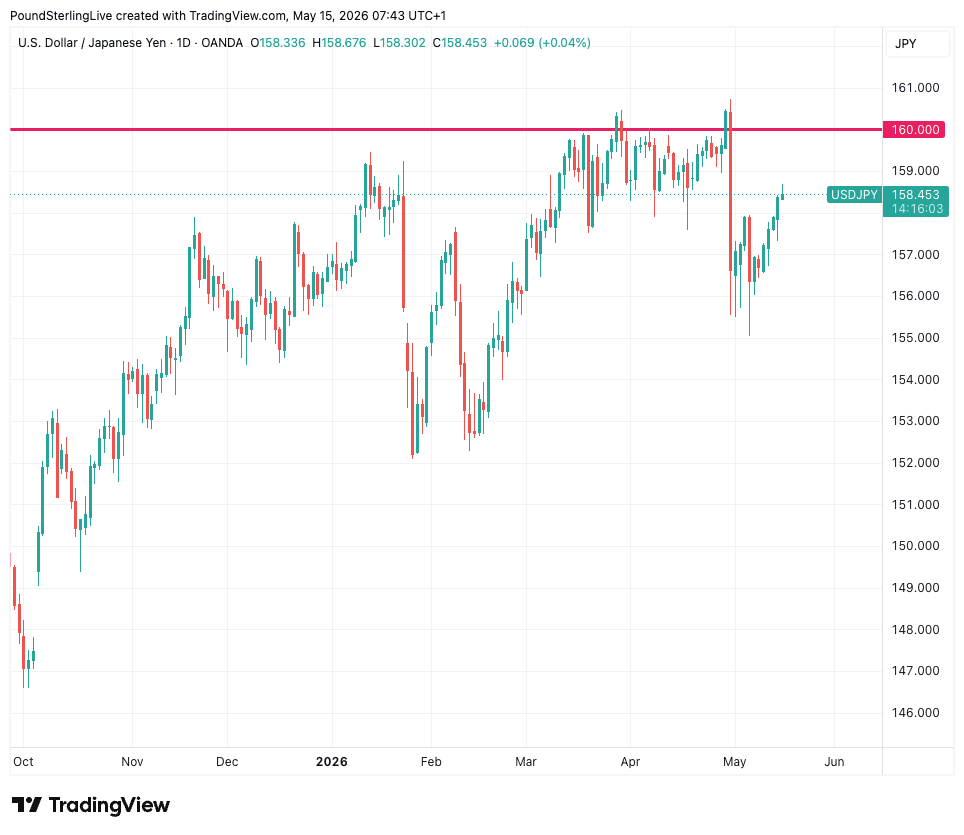

Defending the line: USDJPY will continue to pressure 160, thereby testing the Bank of Japan's resolve.

Japanese refiners source around 90% of their crude imports from the Middle East, leaving the country especially vulnerable to supply disruptions and higher transport premiums.

RBC also says domestic investor behaviour is undermining the yen: despite higher Japanese government bond yields, local asset managers have continued buying foreign debt rather than repatriating capital back into domestic fixed income markets.

Japanese investors purchased a net $50BN of foreign bonds over the past year, reflecting concerns about instability in the domestic bond market caused by the Bank of Japan’s gradual balance sheet reduction and a worsening fiscal outlook under Prime Minister Sanae Takaichi’s government.

RBC says the BoJ’s quantitative tightening programme is removing an important source of demand for Japanese government bonds at a time when issuance risks are increasing.

Markets are also concerned that the Takaichi government's proposed tax cuts and expansionary fiscal policies will contribute to the yen’s valuation.

Against this backdrop, RBC says foreign exchange intervention at the Bank of Japan can only slow, rather than reverse, yen weakness.

RBC says the BoJ appears to have intervened multiple times around the 160 level during the Golden Week holiday period and expects authorities to continue defending that area.

However, it argues intervention will likely only place a temporary “lid” on USD/JPY unless underlying fundamentals improve.

“We suspect any intervention will merely act as a lid on USD/JPY, not a catalyst for protracted yen strength,” says Keshvani.

RBC forecasts USD/JPY to rise to 156 by June, 158 by September and 160 by year-end, compared with previous forecasts of 153, 150 and 147, respectively.