File image of Sanae Takaichi. Source: UN DDR. Licensing CC 2.0.

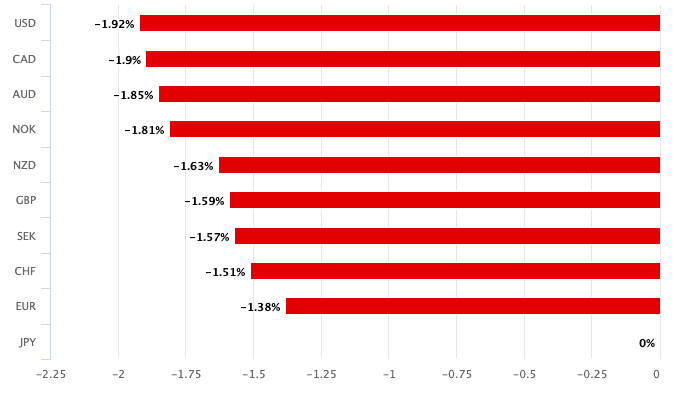

The Japanese yen is down sharply as political developments potentially rule out further interest rate cuts at the Bank of Japan.

The yen fell out of bed Monday after Japan's LDP unexpectedly picked Sanae Takaichi as its leader, someone who is known for her support of higher government spending and lower borrowing costs.

"The yen has weakened sharply during the Asian trading session following the victory for Sanae Takaichi in the LDP leadership election held over the weekend," says Lee Hardman, Senior Currency Analyst EMEA at MUFG Bank Ltd.

Losses for the yen were widespread, with dollar-yen breaching 150, pound-yen gapping through 200 to go to 202 and euro-yen rising to 175, up from Friday's close at 173.19.

A previous spell of yen weakness in April that took it to current levels proved short-lived and was soon faded by traders.

However, Hardman notes the victory for Sanae Takaichi potentially provides stronger justification for a more sustained yen sell-off on this occasion.

"Her election victory has also triggered outsized moves in the Japanese equity and bond markets. The Nikkei 225 equity index has risen by almost 5.0% while the 30-year JGB yield has risen by around 13bps from Friday’s close lifting it a fresh year to date high. The initial market reaction reflects expectations that Sanae Takaichi will actively pursue looser fiscal and monetary policies to support economic growth in Japan," says Hardman.

He explains she is well known as an 'Abenomics' torchbearer.

Abenomics - named after Japanese Prime Minister Shinzo Abe's policies of aggressive monetary policy to increase the money supply and lower interest rates, flexible fiscal policy involving increased government spending on infrastructure and incentives, and structural reforms to boost competitiveness.

Clearly, markets are responding to the money supply and interest rate element of Abenomics, which faces a revival under the new prime minister. "The Japanese rate market has responded accordingly to pare back expectations for further BoJ rate hikes at the short-end of the curve," says Hardman.

We do wonder, however, if Takaichi can pursue an 'Abenomics' monetary policy path as it will surely be scrutinised by the U.S. Administration, which is pursuing a weaker dollar policy.

Scott Bessent, the U.S. Treasury Secretary, in August criticised Japan's interest rate settings, stating the Bank of Japan (BOJ) was "behind the curve" in addressing inflation and expected a rate hike.

The U.S. Treasury Department's June 2025 exchange-rate report also called for the BOJ to continue tightening policy, aiming for a "normalisation of the yen's weakness".

✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.

"The weaker yen may also start to attract more attention/criticism from the Trump administration keeping pressure on Japan to continue normalising monetary policy," says Hardman.

Nevertheless, the market doesn't see this as an immediate risk and price action indicates a belief the Bank of Japan will struggle to get interest rates much higher.

"Even initial discussions between the BoJ and government may delay plans for a hike as early as this month until there is more clarity from both sides of what is required," says Hardman.

She has also advocated for "responsible aggressive fiscal policies" and economists think this will result in a deterioration of Japan's budget position.

Hardman points out that during the Upper House election, Takaichi was the only leadership candidate who considered increasing the issuance of deficit bonds as unavoidable.

"The combination of heightened fiscal risks in Japan and risk of delayed or even derailed BoJ rate hike plans will continue to encourage a weaker yen in the near-term unless evidence emerges that those initial policy expectations will not be realised," says Hardman.